Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You have been given two different investments: Stock X and Stock Y. The Economist for your firm has given you the following expected returns given

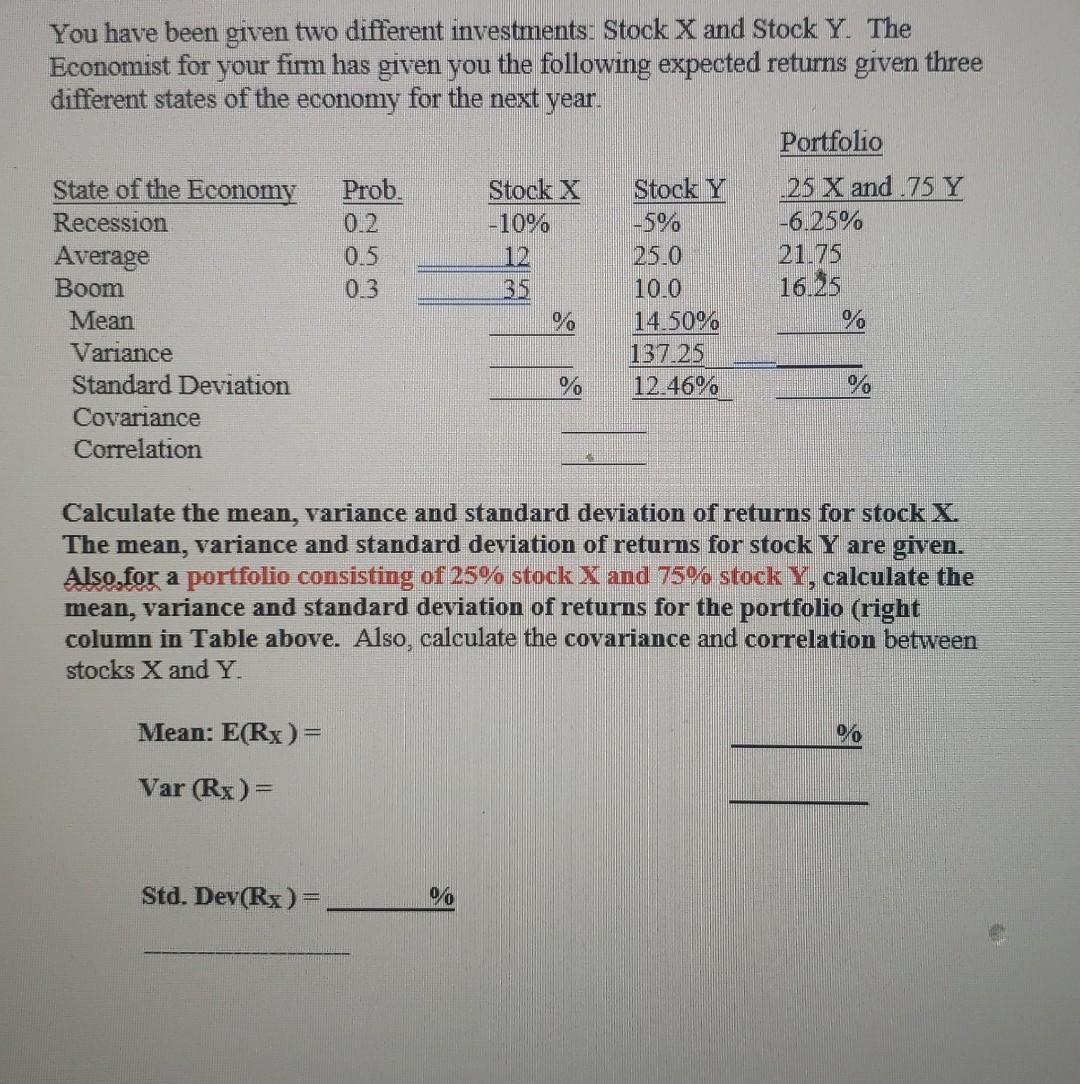

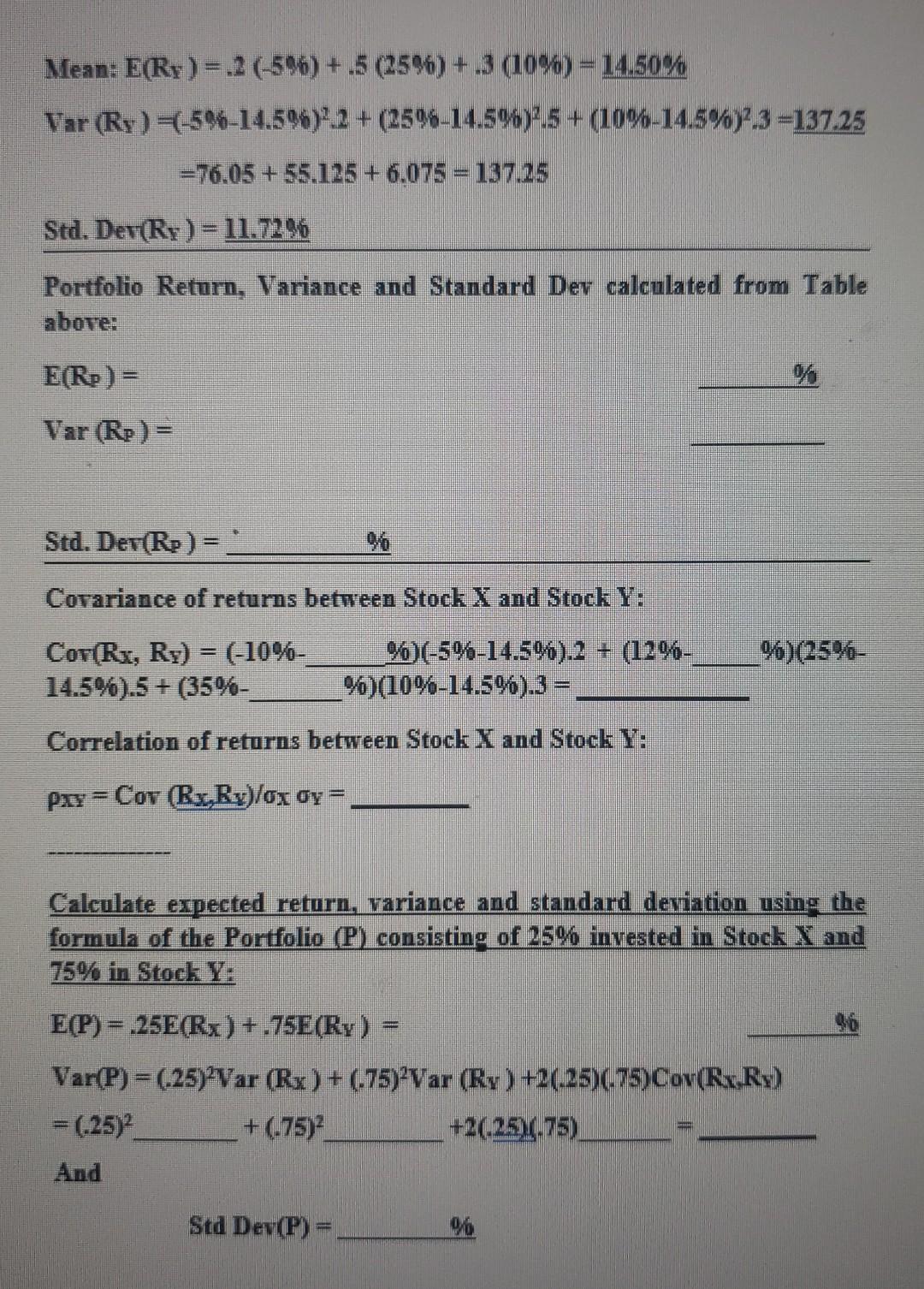

You have been given two different investments: Stock X and Stock Y. The Economist for your firm has given you the following expected returns given three different states of the economy for the next year. Portfolio State of the Economy Prob. Stock X Stock Y -25 X and 75 Y Recession 0.2 -10% -5% -6.25% Average 0.5 25.0 21.75 Boom 0.3 35 10.0 16.35 Mean % 14.50% % Variance 137.25 Standard Deviation % 12.46% Covariance Correlation Calculate the mean, variance and standard deviation of returns for stock X. The mean, variance and standard deviation of returns for stock Y are given. Also.for a portfolio consisting of 25% stock X and 75% stock Y, calculate the mean, variance and standard deviation of returns for the portfolio (right column in Table above. Also, calculate the covariance and correlation between stocks X and Y. Mean: E(Rx) = 00 Var (Rx)= Std. Dev(Rx ) = 0% Mean: E(Ry) =.2 (-5%6) +.5 (2596) +.3 (10%) = 14.50% Var (Ry)=(-5%-14.596).2 + (2596-14.5%)',5 + (10%-14.5%y3-137.25 =76.05 + 55.125 +6.075 = 137,25 Std. Der(Ry)=11.7296 Portfolio Retum, Variance and Standard Dev calculated from Table above: E(Re) = Var (Rp)= Std. Dev(R)= " Covariance of returns between Stock X and Stock Y: 96)(2596- Cov(Rx, Ry) = (-10%- 14.5%).5+ (35%- %)(-5%-14.5%).2 + (1296- %)(10%-14.5%).3 = Correlation of returns between Stock X and Stock Y: PXY = Cor (Ry, Ry)/ox Oy Calculate expected return, variance and standard deviation using the formula of the Portfolio (P) consisting of 25% invested in Stock X and 75% in Stock Y: E(P)= .25E(Rx) +.75E(Ry) Var(P) = (-25) Var (Rx) + (.75){Var (Ry) +20.25)(-75)Cov(Rr.Ry) = (-25) + (175) +2.25.75) And Std Dev(P) =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started