Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You have combined two stocks, ABC and DEF, into an equally weighted portfolio (Stable) and it has a variance of 35%. The covariance between

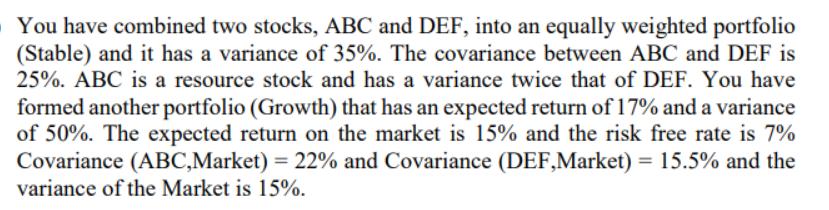

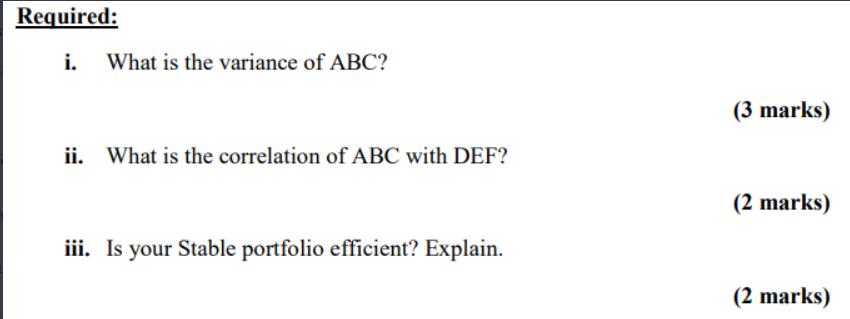

You have combined two stocks, ABC and DEF, into an equally weighted portfolio (Stable) and it has a variance of 35%. The covariance between ABC and DEF is 25%. ABC is a resource stock and has a variance twice that of DEF. You have formed another portfolio (Growth) that has an expected return of 17% and a variance of 50%. The expected return on the market is 15% and the risk free rate is 7% Covariance (ABC,Market) = 22% and Covariance (DEF,Market) = 15.5% and the variance of the Market is 15%. Required: i. What is the variance of ABC? ii. What is the correlation of ABC with DEF? iii. Is your Stable portfolio efficient? Explain. (3 marks) (2 marks) (2 marks)

Step by Step Solution

★★★★★

3.41 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

i Variance of ABC Given Variance of the equally weighted portfolio Stable 35 Covariance between ABC and DEF 25 Variance of ABC is twice that of DEF We can use the formula for the variance of a portfol...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Jarrad Harford

5th Edition

0135811600, 978-0135811603