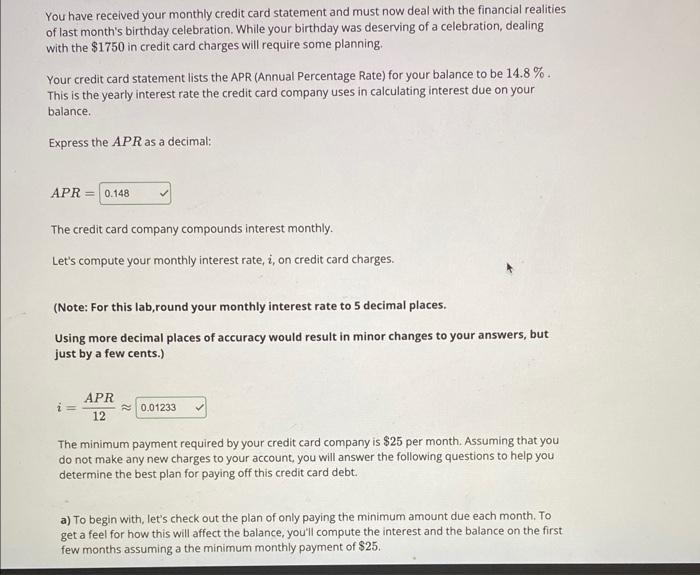

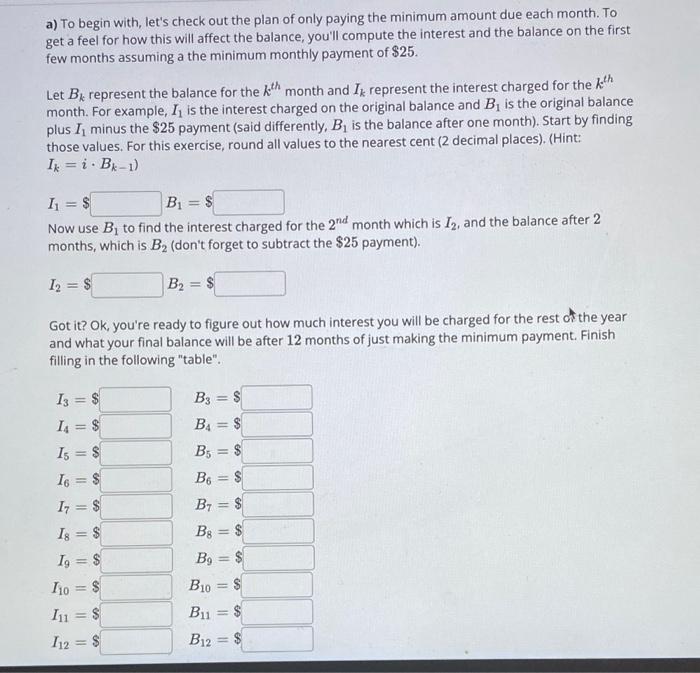

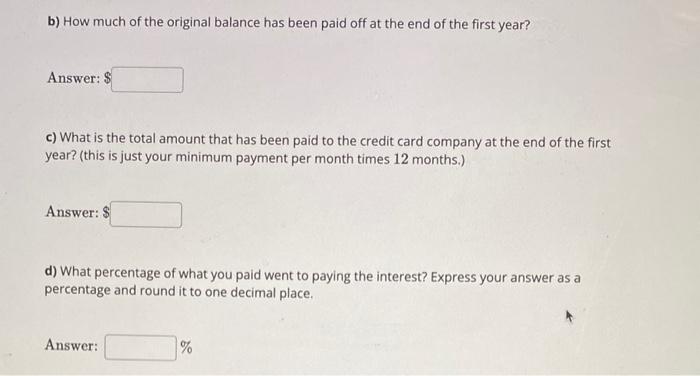

You have received your monthly credit card statement and must now deal with the financial realities of last month's birthday celebration. While your birthday was deserving of a celebration, dealing with the $1750 in credit card charges will require some planning. Your credit card statement lists the APR (Annual Percentage Rate) for your balance to be 14.8%. This is the yearly interest rate the credit card company uses in calculating interest due on your balance. Express the APR as a decimal: APR= The credit card company compounds interest monthly. Let's compute your monthly interest rate, i, on credit card charges. (Note: For this lab,round your monthly interest rate to 5 decimal places. Using more decimal places of accuracy would result in minor changes to your answers, but just by a few cents.) i=12APR The minimum payment required by your credit card company is $25 per month. Assuming that you do not make any new charges to your account, you will answer the following questions to help you determine the best plan for paying off this credit card debt. a) To begin with, let's check out the plan of only paying the minimum amount due each month. To get a feel for how this will affect the balance, you'll compute the interest and the balance on the first few months assuming a the minimum monthly payment of $25. a) To begin with, let's check out the plan of only paying the minimum amount due each month. To get a feel for how this will affect the balance, you'll compute the interest and the balance on the first few months assuming a the minimum monthly payment of $25. Let Bk represent the balance for the kth month and Ik represent the interest charged for the kth month. For example, I1 is the interest charged on the original balance and B1 is the original balance plus I1 minus the $25 payment (said differently, B1 is the balance after one month). Start by finding those values. For this exercise, round all values to the nearest cent ( 2 decimal places). (Hint: Ik=iBk1) I1=$B1=$ Now use B1 to find the interest charged for the 2nd month which is I2, and the balance after 2 months, which is B2 (don't forget to subtract the $25 payment). I2=$B2=$ Got it? Ok, you're ready to figure out how much interest you will be charged for the rest of the year and what your final balance will be after 12 months of just making the minimum payment. Finish filling in the following "table". b) How much of the original balance has been paid off at the end of the first year? Answer: $ c) What is the total amount that has been paid to the credit card company at the end of the first year? (this is just your minimum payment per month times 12 months.) Answer: $ d) What percentage of what you paid went to paying the interest? Express your answer as a percentage and round it to one decimal place. Answer: % You have received your monthly credit card statement and must now deal with the financial realities of last month's birthday celebration. While your birthday was deserving of a celebration, dealing with the $1750 in credit card charges will require some planning. Your credit card statement lists the APR (Annual Percentage Rate) for your balance to be 14.8%. This is the yearly interest rate the credit card company uses in calculating interest due on your balance. Express the APR as a decimal: APR= The credit card company compounds interest monthly. Let's compute your monthly interest rate, i, on credit card charges. (Note: For this lab,round your monthly interest rate to 5 decimal places. Using more decimal places of accuracy would result in minor changes to your answers, but just by a few cents.) i=12APR The minimum payment required by your credit card company is $25 per month. Assuming that you do not make any new charges to your account, you will answer the following questions to help you determine the best plan for paying off this credit card debt. a) To begin with, let's check out the plan of only paying the minimum amount due each month. To get a feel for how this will affect the balance, you'll compute the interest and the balance on the first few months assuming a the minimum monthly payment of $25. a) To begin with, let's check out the plan of only paying the minimum amount due each month. To get a feel for how this will affect the balance, you'll compute the interest and the balance on the first few months assuming a the minimum monthly payment of $25. Let Bk represent the balance for the kth month and Ik represent the interest charged for the kth month. For example, I1 is the interest charged on the original balance and B1 is the original balance plus I1 minus the $25 payment (said differently, B1 is the balance after one month). Start by finding those values. For this exercise, round all values to the nearest cent ( 2 decimal places). (Hint: Ik=iBk1) I1=$B1=$ Now use B1 to find the interest charged for the 2nd month which is I2, and the balance after 2 months, which is B2 (don't forget to subtract the $25 payment). I2=$B2=$ Got it? Ok, you're ready to figure out how much interest you will be charged for the rest of the year and what your final balance will be after 12 months of just making the minimum payment. Finish filling in the following "table". b) How much of the original balance has been paid off at the end of the first year? Answer: $ c) What is the total amount that has been paid to the credit card company at the end of the first year? (this is just your minimum payment per month times 12 months.) Answer: $ d) What percentage of what you paid went to paying the interest? Express your answer as a percentage and round it to one decimal place. Answer: %