Answered step by step

Verified Expert Solution

Question

1 Approved Answer

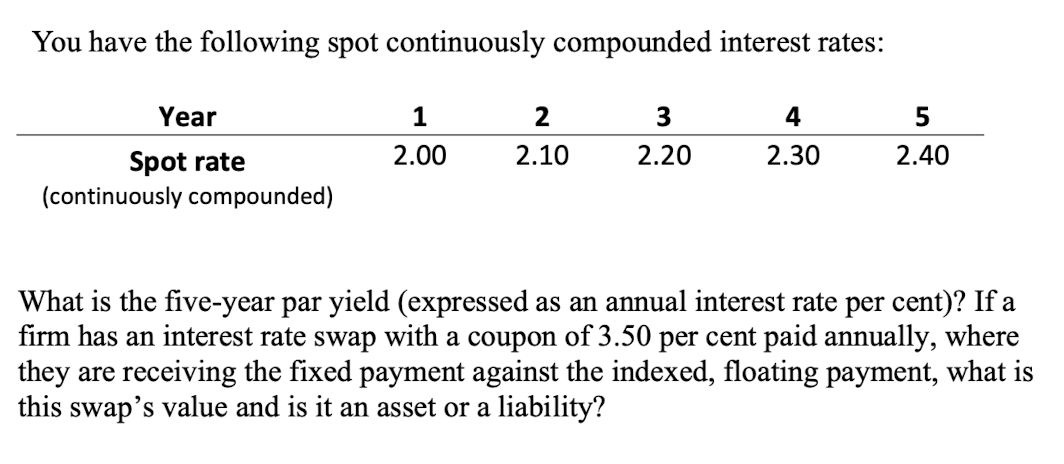

You have the following spot continuously compounded interest rates: Year Spot rate (continuously compounded) 1 2.00 2 2.10 3 2.20 4 2.30 5 2.40

You have the following spot continuously compounded interest rates: Year Spot rate (continuously compounded) 1 2.00 2 2.10 3 2.20 4 2.30 5 2.40 What is the five-year par yield (expressed as an annual interest rate per cent)? If a firm has an interest rate swap with a coupon of 3.50 per cent paid annually, where they are receiving the fixed payment against the indexed, floating payment, what is this swap's value and is it an asset or a liability?

Step by Step Solution

★★★★★

3.38 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

To find the fiveyear par yield we need to calculate the continuously compounded rate that makes the ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Eugene F. Brigham, Phillip R. Daves

11th edition

978-1111530266