Answered step by step

Verified Expert Solution

Question

1 Approved Answer

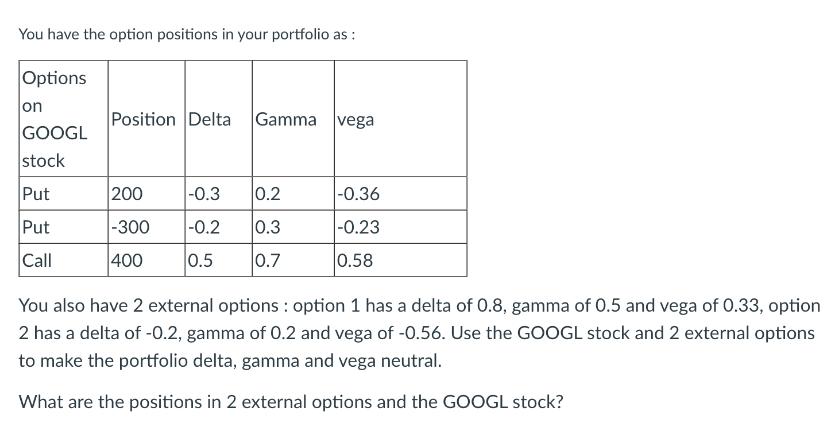

You have the option positions in your portfolio as: Options on GOOGL stock Put Put Call Position Delta Gamma vega 200 -0.3 0.2 -300

You have the option positions in your portfolio as: Options on GOOGL stock Put Put Call Position Delta Gamma vega 200 -0.3 0.2 -300 -0.2 0.3 400 0.5 0.7 -0.36 -0.23 0.58 You also have 2 external options: option 1 has a delta of 0.8, gamma of 0.5 and vega of 0.33, option 2 has a delta of -0.2, gamma of 0.2 and vega of -0.56. Use the GOOGL stock and 2 external options to make the portfolio delta, gamma and vega neutral. What are the positions in 2 external options and the GOOGL stock?

Step by Step Solution

★★★★★

3.49 Rating (159 Votes )

There are 3 Steps involved in it

Step: 1

To make the portfolio delta gamma and vega neutral we need to ensure that the sum of deltas gammas a...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Basic Statistics

Authors: Charles Henry Brase, Corrinne Pellillo Brase

6th Edition

978-1133525097, 1133525091, 1111827028, 978-1133110316, 1133110312, 978-1111827021