Answered step by step

Verified Expert Solution

Question

1 Approved Answer

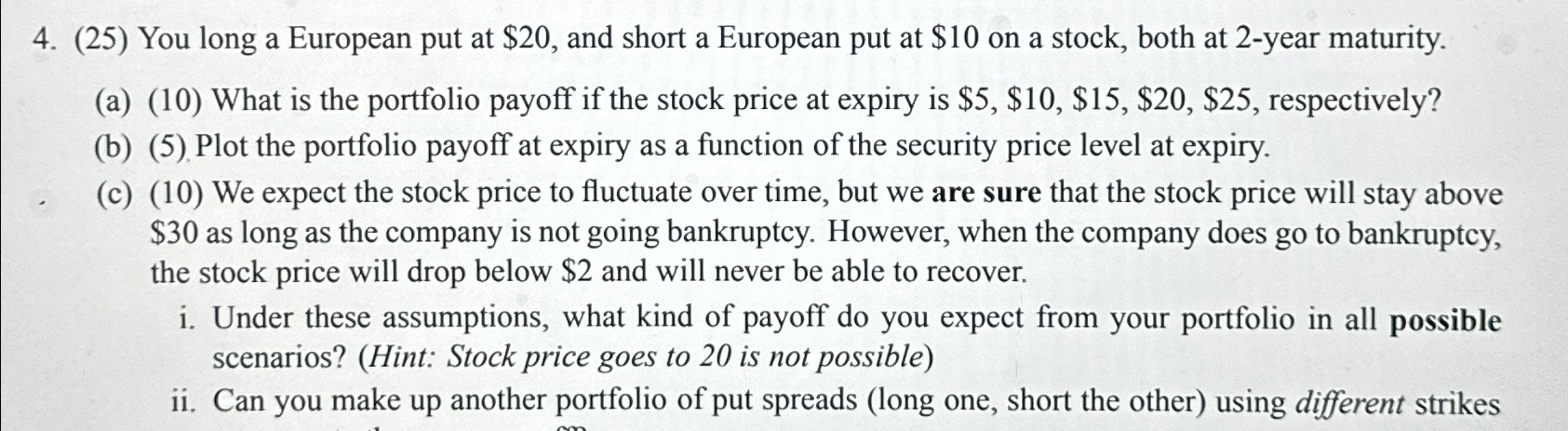

You long a European put at $ 2 0 , and short a European put at $ 1 0 on a stock, both at 2

You long a European put at $ and short a European put at $ on a stock, both at year maturity.

a What is the portfolio payoff if the stock price at expiry is $$$$$ respectively?

b Plot the portfolio payoff at expiry as a function of the security price level at expiry.

c We expect the stock price to fluctuate over time, but we are sure that the stock price will stay above $ as long as the company is not going bankruptcy. However, when the company does go to bankruptcy, the stock price will drop below $ and will never be able to recover.

i Under these assumptions, what kind of payoff do you expect from your portfolio in all possible scenarios? Hint: Stock price goes to is not possible

ii Can you make up another portfolio of put spreads long one, short the other using different strikes

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started