Answered step by step

Verified Expert Solution

Question

1 Approved Answer

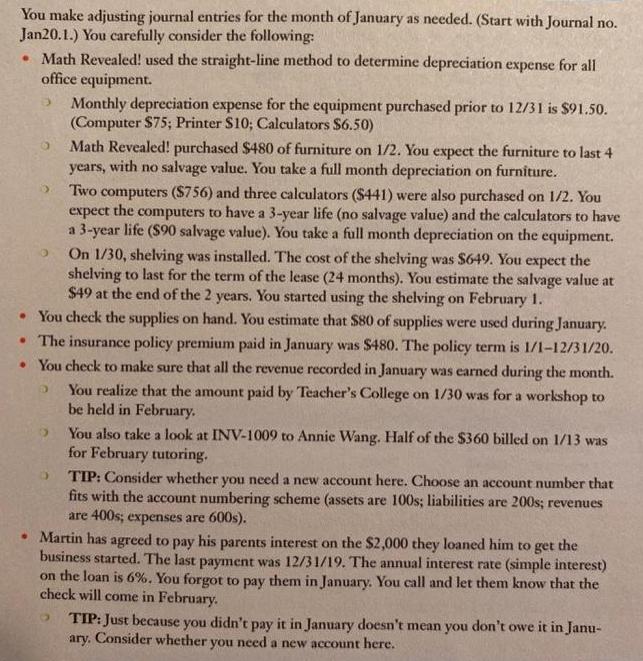

You make adjusting journal entries for the month of January as needed. (Start with Journal no. Jan20.1.) You carefully consider the following: Math Revealed!

You make adjusting journal entries for the month of January as needed. (Start with Journal no. Jan20.1.) You carefully consider the following: Math Revealed! used the straight-line method to determine depreciation expense for all office equipment. Monthly depreciation expense for the equipment purchased prior to 12/31 is $91.50. (Computer $75; Printer S10; Calculators S6.50) Math Revealed! purchased $480 of furniture on 1/2. You expect the furniture to last 4 years, with no salvage value. You take a full month depreciation on furniture. Two computers ($756) and three calculators ($441) were also purchased on 1/2. You expect the computers to have a 3-year life (no salvage value) and the calculators to have a 3-year life ($90 salvage value). You take a full month depreciation on the equipment. On 1/30, shelving was installed. The cost of the shelving was $649. You expect the shelving to last for the term of the lease (24 months). You estimate the salvage value at $49 at the end of the 2 years. You started using the shelving on February 1. You check the supplies on hand. You estimate that S80 of supplies were used during January. The insurance policy premium paid in January was $480. The policy term is 1/1-12/31/20. You check to make sure that all the revenue recorded in January was earned during the month. You realize that the amount paid by Teacher's College on 1/30 was for a workshop to be held in February. You also take a look at INV-1009 Annie Wang. Half of the $360 billed on 1/13 was for February tutoring. TIP: Consider whether you need a new account here. Choose an account number that fits with the account numbering scheme (assets are 100s; liabilities are 200s; revenues are 400s; expenses are 600s). Martin has agreed to pay his parents interest on the $2,000 they loaned him to get the business started. The last payment was 12/31/19. The annual interest rate (simple interest) on the loan is 6%. You forgot to pay them in January. You call and let them know that the check will come in February. TIP: Just because you didn't pay it in January doesn't mean you don't owe it in Janu- ary. Consider whether you need a new account here.

Step by Step Solution

★★★★★

3.54 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Depreciation calculation ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Survey Of Accounting

Authors: Paul D. Kimmel, Jerry J. Weygandt

2nd Edition

1119594537, 978-1119594536