Answered step by step

Verified Expert Solution

Question

1 Approved Answer

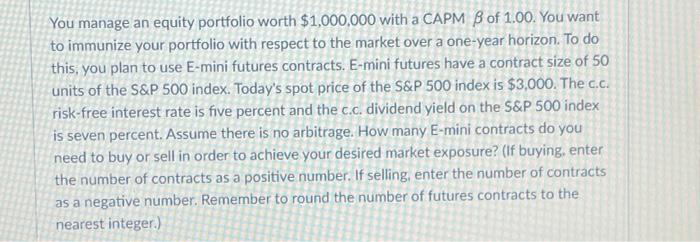

You manage an equity portfolio worth $1,000,000 with a CAPMB of 1.00. You want to immunize your portfolio with respect to the market over a

You manage an equity portfolio worth $1,000,000 with a CAPMB of 1.00. You want to immunize your portfolio with respect to the market over a one-year horizon. To do this, you plan to use E-mini futures contracts. E-mini futures have a contract size of 50 units of the S&P 500 index. Today's spot price of the S&P 500 index is $3,000. The c.c. risk-free interest rate is five percent and the c.c. dividend yield on the S&P 500 index is seven percent. Assume there is no arbitrage. How many E-mini contracts do you need to buy or sell in order to achieve your desired market exposure? (If buying, enter the number of contracts as a positive number. If selling, enter the number of contracts as a negative number. Remember to round the number of futures contracts to the nearest integer.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Broadcasting Finance In Transition

Authors: Jay G. Blumler, T. J. Nossiter

1st Edition

0195050894, 978-0195050899