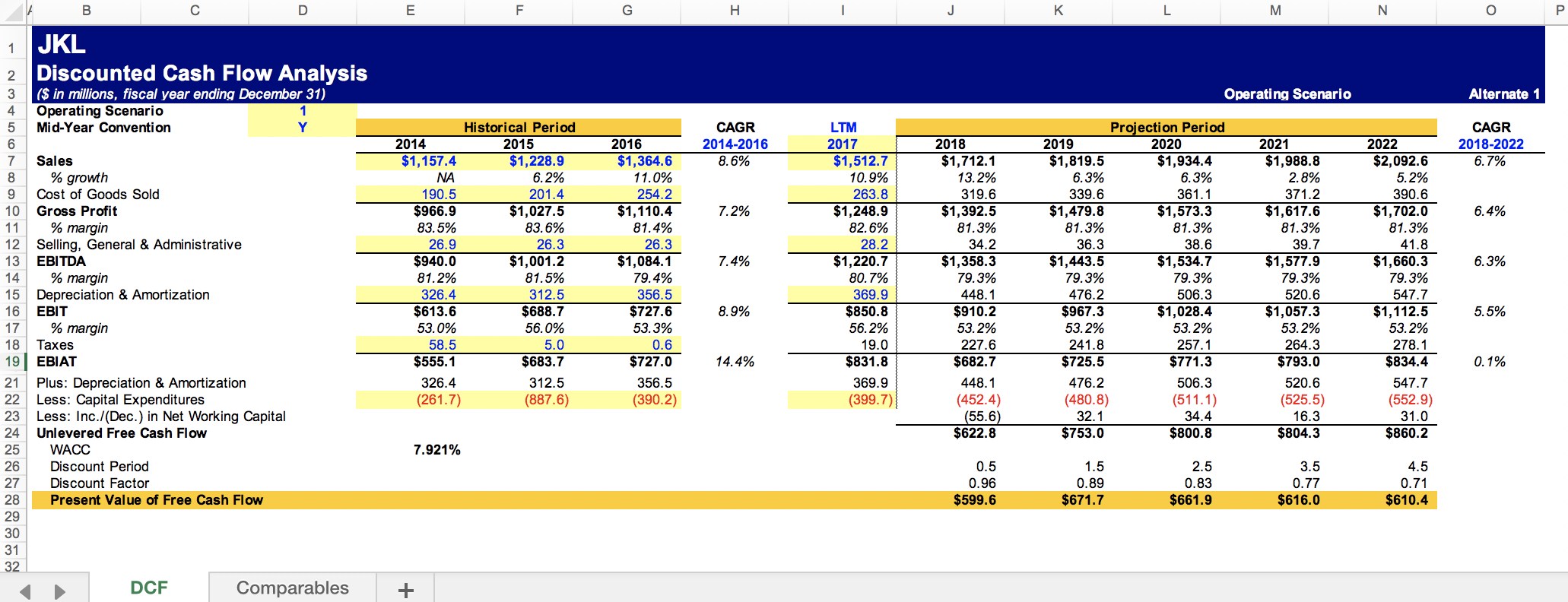

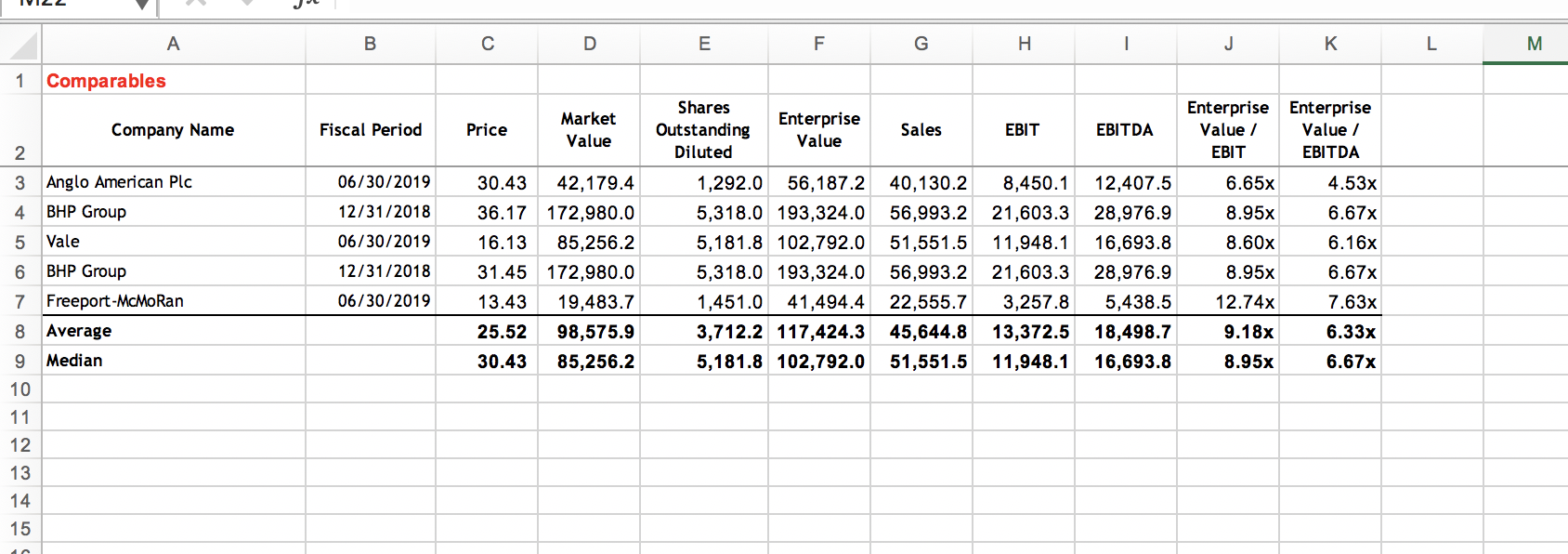

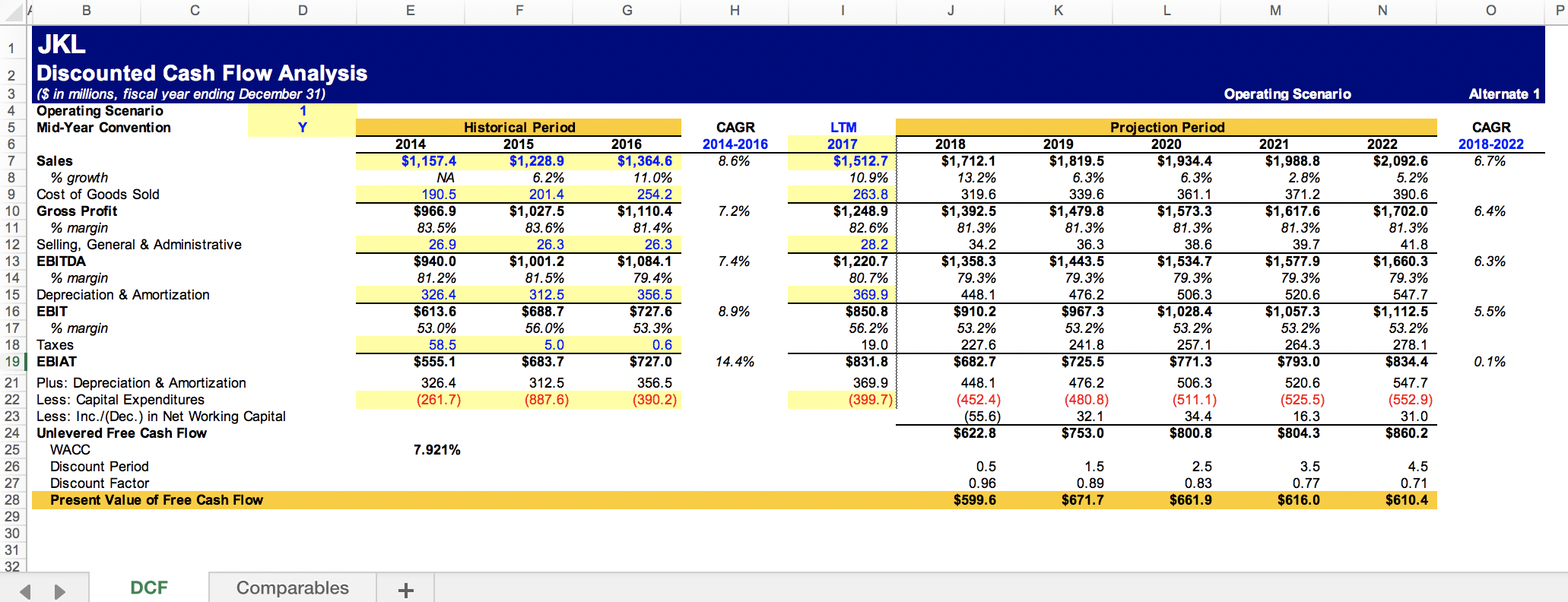

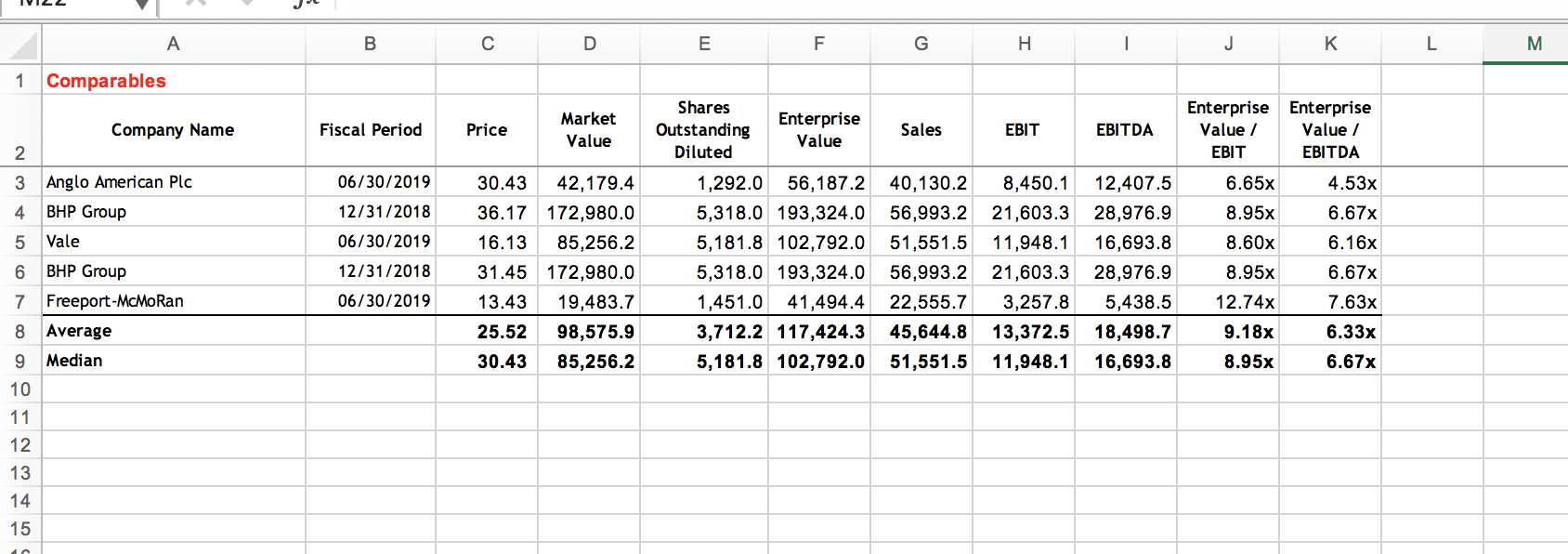

You need to complete a DCF Valuation Analysis for company JKL. The file Question_8.xlsx has the relevant data in the worksheet DCF. You are still missing the Terminal Value component of your valuation. For simplicity you decide to estimate the Terminal Value using the "Exit Multiple" methodology. Calculate the Enterprise Value of the company assuming an Exit multiple equal to the average multiple for the comparables derived from Factset ("Comps") and reported in the worksheet Comparables. Use the average multiple with two decimal digits of precision. Do the calculations in excel linking to the cells directly to avoid loss of precision. Express your answer in millions of dollars with one decimal point and without the dollar sign. So an enterprise value of 21,345.2m$ should be entered as 21345.2

M O B C D E F G H K N JKL Discounted Cash Flow Analysis Alternate 1 ($ in millions, fiscal year ending December 31) Operating Scenario Operating Scenario Historical Period CAGR LTM Projection Period CAGR Mid-Year Convention 2014 2015 2016 2014-2016 2017 2018 2019 2020 2021 2022 2018-2022 $1, 157.4 $1,228.9 $1,364.6 8.6% $1,512.7 $1, 712. 1 $1,819.5 $1,934.4 $1,988.8 $2, 092.6 6.7% Sales % growth NA 6.2% 11.0% 10.9% 13.2% 6.3% 6.3% 2.8% 5.2% Cost of Goods Sold 190.5 201.4 254.2 263.8 319.6 339.6 361.1 371.2 390.6 $1,573.3 $1, 617.6 $1,702.0 6.4% Gross Profit $966.9 $1,027.5 $1, 110.4 7.2% $1,248.9 $1,392.5 $1,479.8 83.5% 83.6% 81.4% 82.6% 81.3% 81.3% 81.3% 81.3% 81.3% % margin Selling, General & Administrative 26.9 26.3 26.3 28.2 34.2 36.3 38.6 39.7 41.8 EBITDA $940.0 $1,001.2 $1,084.1 7.4% $1,220.7 $1,358.3 $1,443.5 $1,534.7 $1,577.9 $1, 660.3 6.3% 79.3% 79.3% 79.3% 79.3% 14 % margin 81.2% 81.5% 79. 4% 80. 7% 79.3% 15 Depreciation & Amortization 326.4 312.5 356.5 369.9 448.1 476.2 506.3 520.6 547.7 16 EBIT $613.6 $688.7 $727.6 8.9% $850.8 $910.2 $967.3 $1,028.4 $1,057.3 $1, 112.5 5.5% 17 % margin 53.0% 56.0% 53.3% 56. 2% 53.2% 53.2% 53.2% 53.2% 53.2% 241.8 257.1 264.3 278.1 18 Taxes 58.5 5.0 0.6 19.0 227.6 0. 1% 19 EBIAT $555.1 $683.7 $727.0 14.4% $831.8 $682.7 $725.5 $771.3 $793.0 $834.4 21 Plus: Depreciation & Amortization 326.4 312.5 356.5 369.9 448.1 476.2 506.3 520.6 547.7 (480.8) (511.1) (525.5) (552.9) 22 Less: Capital Expenditures (261.7) (887.6) (390.2) (399.7) (452.4) (55.6) 32.1 34.4 16.3 31.0 23 Less: Inc./(Dec.) in Net Working Capital 24 $622.8 $753.0 $804.3 Unlevered Free Cash Flow $800.8 $860.2 25 WACC 7.921% 3.5 26 Discount Period 0.5 1.5 2.5 4.5 Discount Factor 0.96 0.89 0.83 0.77 0.71 Present Value of Free Cash Flow $599.6 $671.7 $661.9 $616.0 $610.4 28 29 30 31 32 DCF Comparables +A B C D E F G H J K L M 1 Comparables Company Name Price Market Shares Fiscal Period Outstanding Enterprise Enterprise Enterprise Sales EBIT EBITDA Value / Value / 2 Value Diluted Value EBIT EBITDA 3 Anglo American Plc 06/30/2019 30.43 42, 179.4 1,292.0 56, 187.2 40, 130.2 8,450.1 12,407.5 6.65x 4.53x 4 BHP Group 12/31/2018 36.17 172,980.0 5,318.0 193,324.0 56,993.2 21,603.3 28,976.9 8.95x 6.67x 5 Vale 06/30/2019 16.13 85,256.2 5, 181.8 102,792.0 51,551.5 11,948.1 16,693.8 8.60x 6.16x 6 BHP Group 12/31/2018 31.45 172,980.0 5,318.0 193,324.0 56,993.2 21,603.3 28,976.9 8.95x 6.67x 7 Freeport-McMoRan 06/30/2019 13.43 19,483.7 1,451.0 41,494.4 22,555.7 3,257.8 5,438.5 12.74x 7.63x 8 Average 25.52 98,575.9 3,712.2 117,424.3 45,644.8 13,372.5 18,498.7 9.18x 6.33x 9 Median 30.43 85,256.2 5,181.8 102,792.0 51,551.5 11,948.1 16,693.8 8.95x 6.67x 10 11 12 13 14 15