Answered step by step

Verified Expert Solution

Question

1 Approved Answer

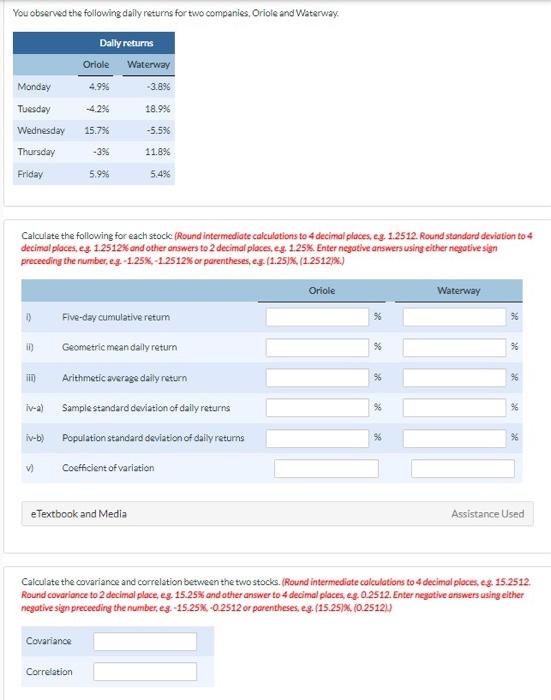

You observed the following daily returns for two companies, Oriole and Waterway Dally returns Oriole Waterway 4.996 -3.896 42% 18.9% Monday Tuesday Wednesday Thursday 15.7%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Cryptocurrencies Decode How To Make Money With Bitcoin And Altcoins

Authors: Lynda Crew

1st Edition

979-8353774839