Answered step by step

Verified Expert Solution

Question

1 Approved Answer

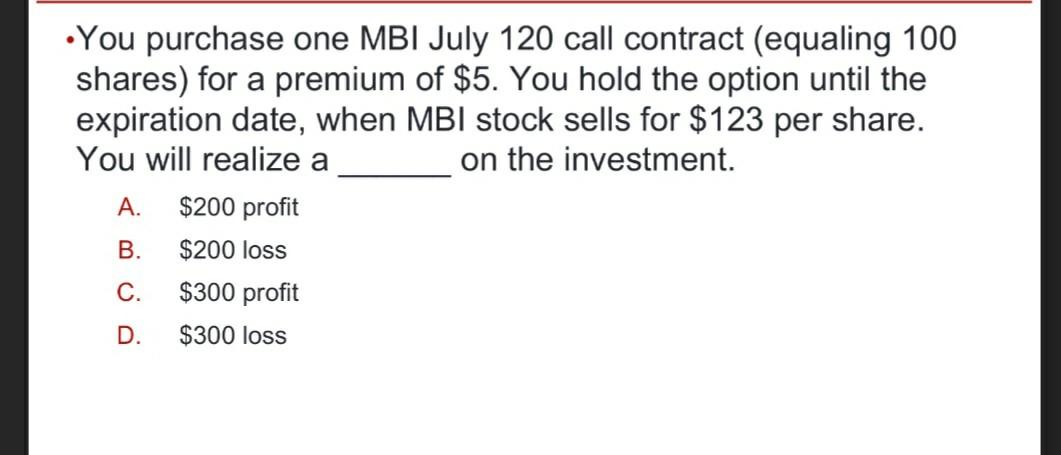

You purchase one MBI July 120 call contract (equaling 100 shares) for a premium of $5. You hold the option until the expiration date, when

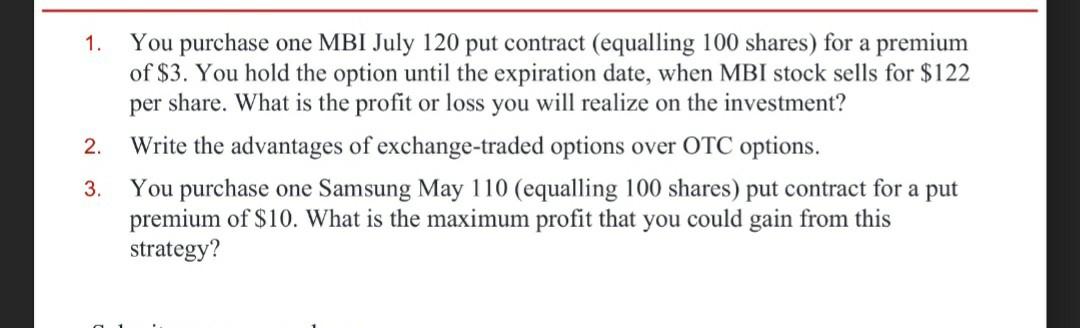

You purchase one MBI July 120 call contract (equaling 100 shares) for a premium of $5. You hold the option until the expiration date, when MBI stock sells for $123 per share. You will realize a on the investment. $200 profit $200 loss $300 profit $300 loss A. B. C. D. 1. 2. You purchase one MBI July 120 put contract (equalling 100 shares) for a premium of $3. You hold the option until the expiration date, when MBI stock sells for $122 per share. What is the profit or loss you will realize on the investment? Write the advantages of exchange-traded options over OTC options. You purchase one Samsung May 110 (equalling 100 shares) put contract for a put premium of $10. What is the maximum profit that you could gain from this strategy? 3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Market Analysis And Behaviour The Adaptive Preference Hypothesis

Authors: Emil Dinga, Camelia Oprean Stan, Cristina Roxana Tinisescu, Vasile Brctian, Gabriela Mariana Ionescu

1st Edition

1032255161, 1000609731, 9781032255163, 9781000609738