Answered step by step

Verified Expert Solution

Question

1 Approved Answer

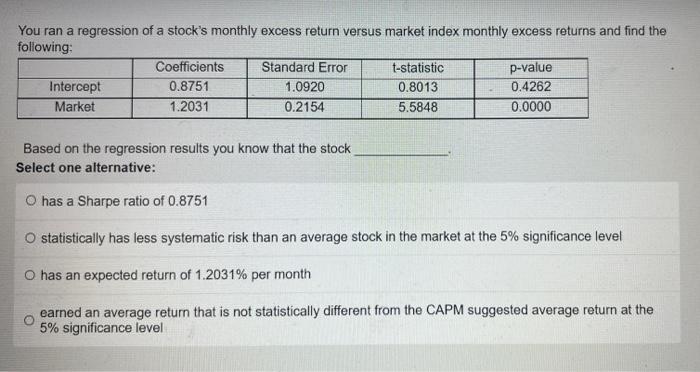

You ran a regression of a stock's monthly excess return versus market index monthly excess returns and find the following: Coefficients Standard Error t-statistic p-value

You ran a regression of a stock's monthly excess return versus market index monthly excess returns and find the following: Coefficients Standard Error t-statistic p-value Intercept 0.8751 1.0920 0.8013 0.4262 Market 1.2031 0.2154 5.5848 0.0000 Based on the regression results you know that the stock Select one alternative: O has a Sharpe ratio of 0.8751 statistically has less systematic risk than an average stock in the market at the 5% significance level O has an expected return of 1.2031% per month earned an average return that is not statistically different from the CAPM suggested average return at the 5% significance level

You ran a regression of a stock's monthly excess return versus market index monthly excess returns and find the following: Coefficients Standard Error t-statistic p-value Intercept 0.8751 1.0920 0.8013 0.4262 Market 1.2031 0.2154 5.5848 0.0000 Based on the regression results you know that the stock Select one alternative: O has a Sharpe ratio of 0.8751 statistically has less systematic risk than an average stock in the market at the 5% significance level O has an expected return of 1.2031% per month earned an average return that is not statistically different from the CAPM suggested average return at the 5% significance level

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Theory Of Constraints Handbook

Authors: James Cox, John Schleier

1st Edition

0071665544, 978-0071665544