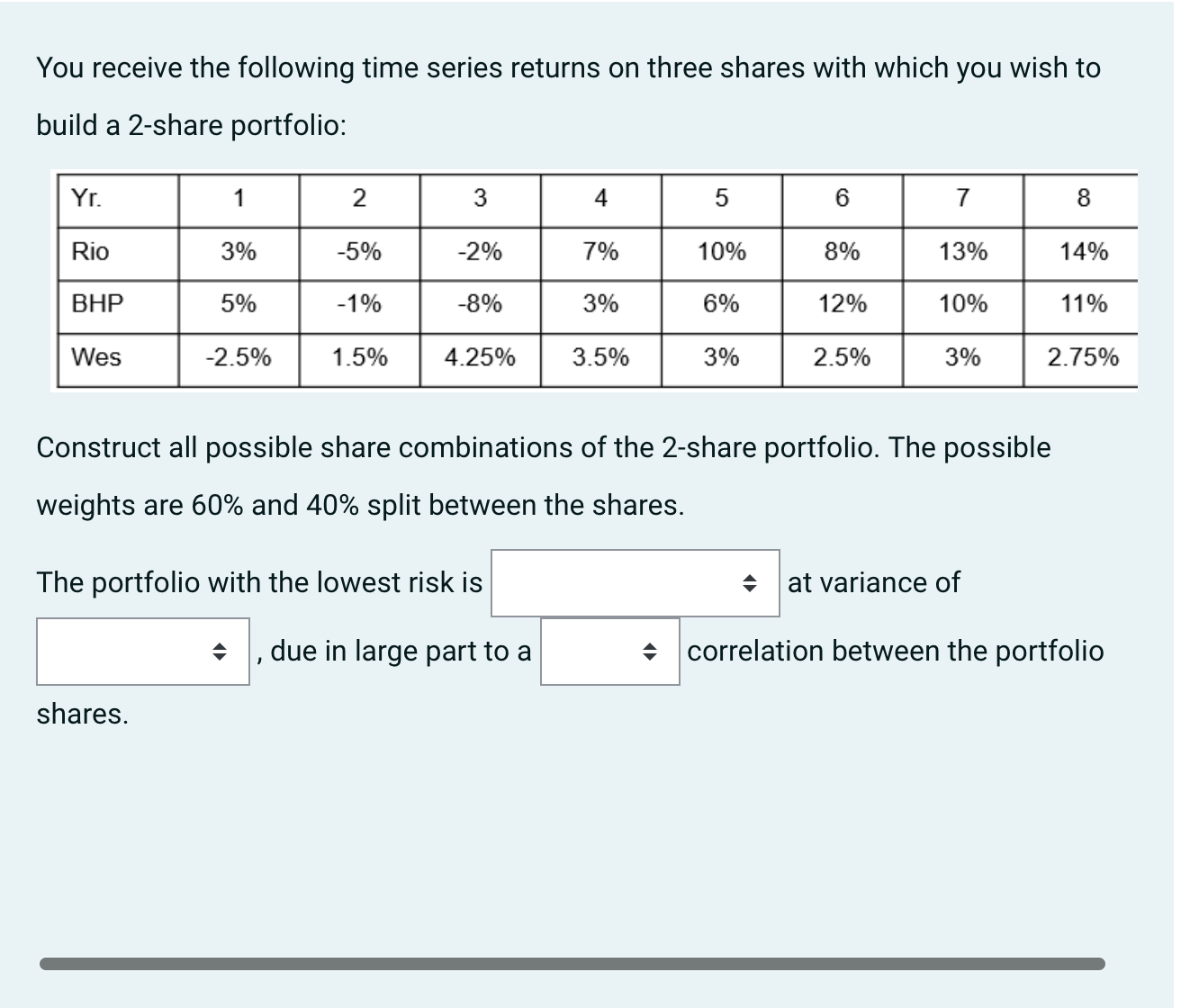

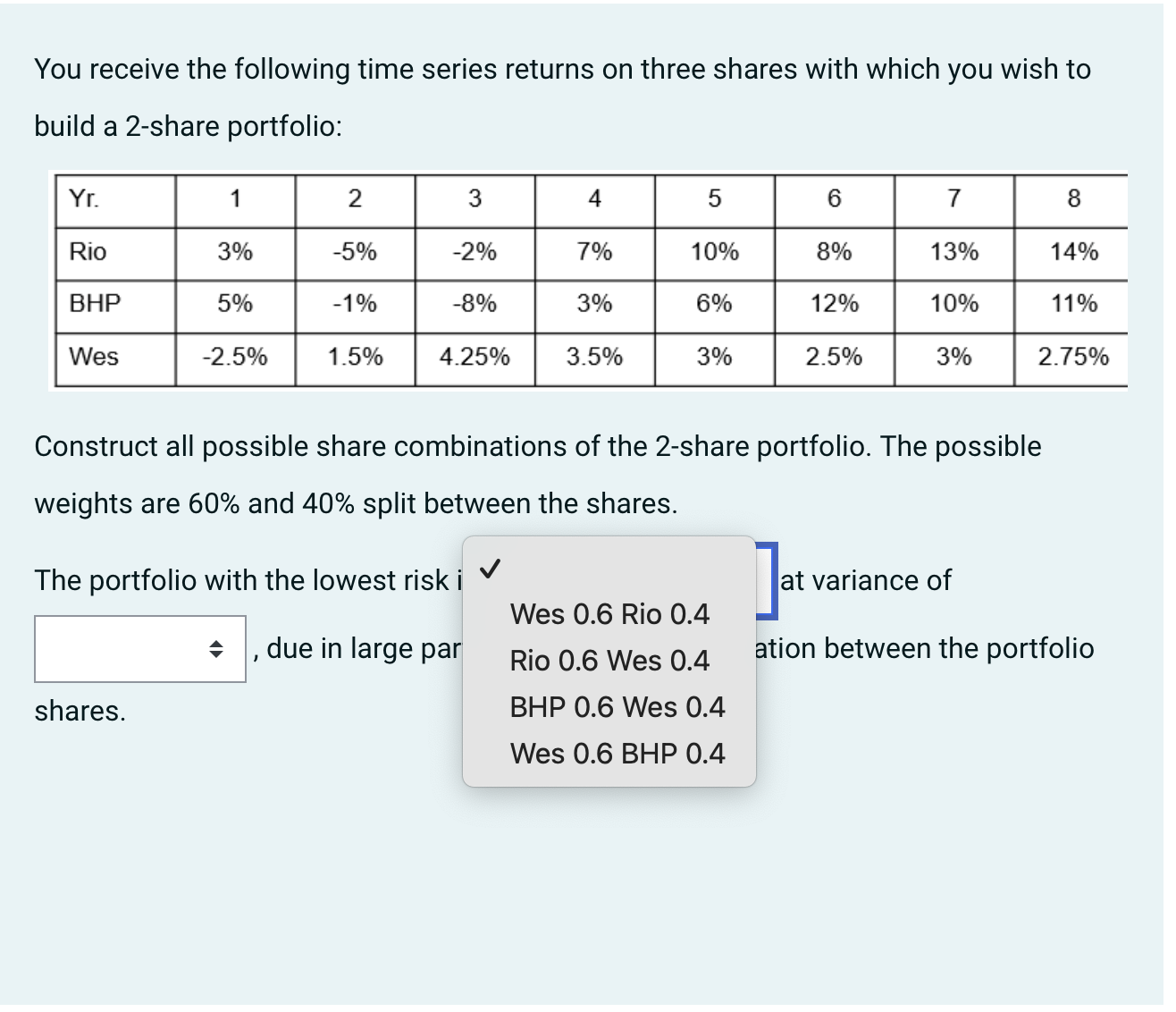

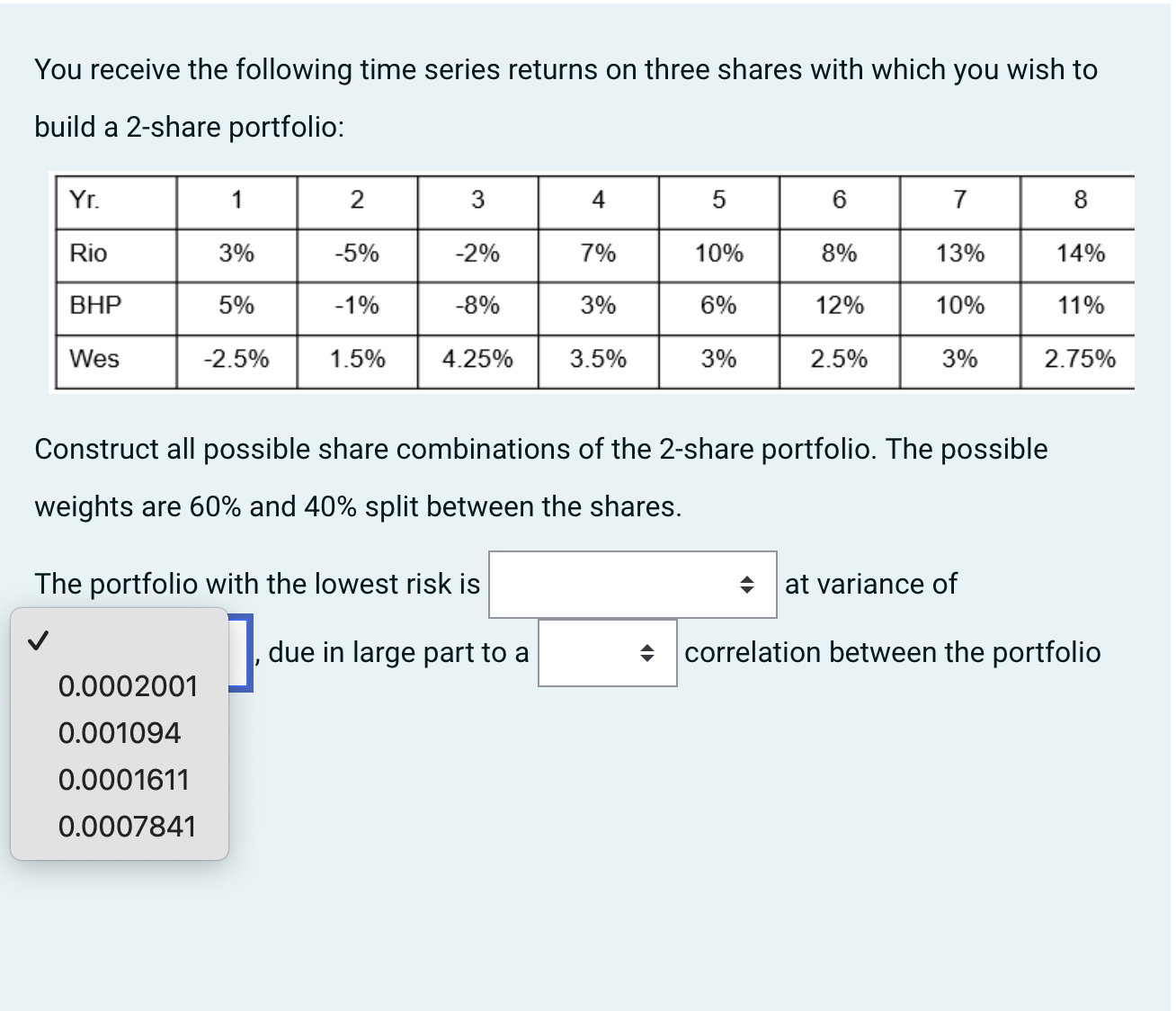

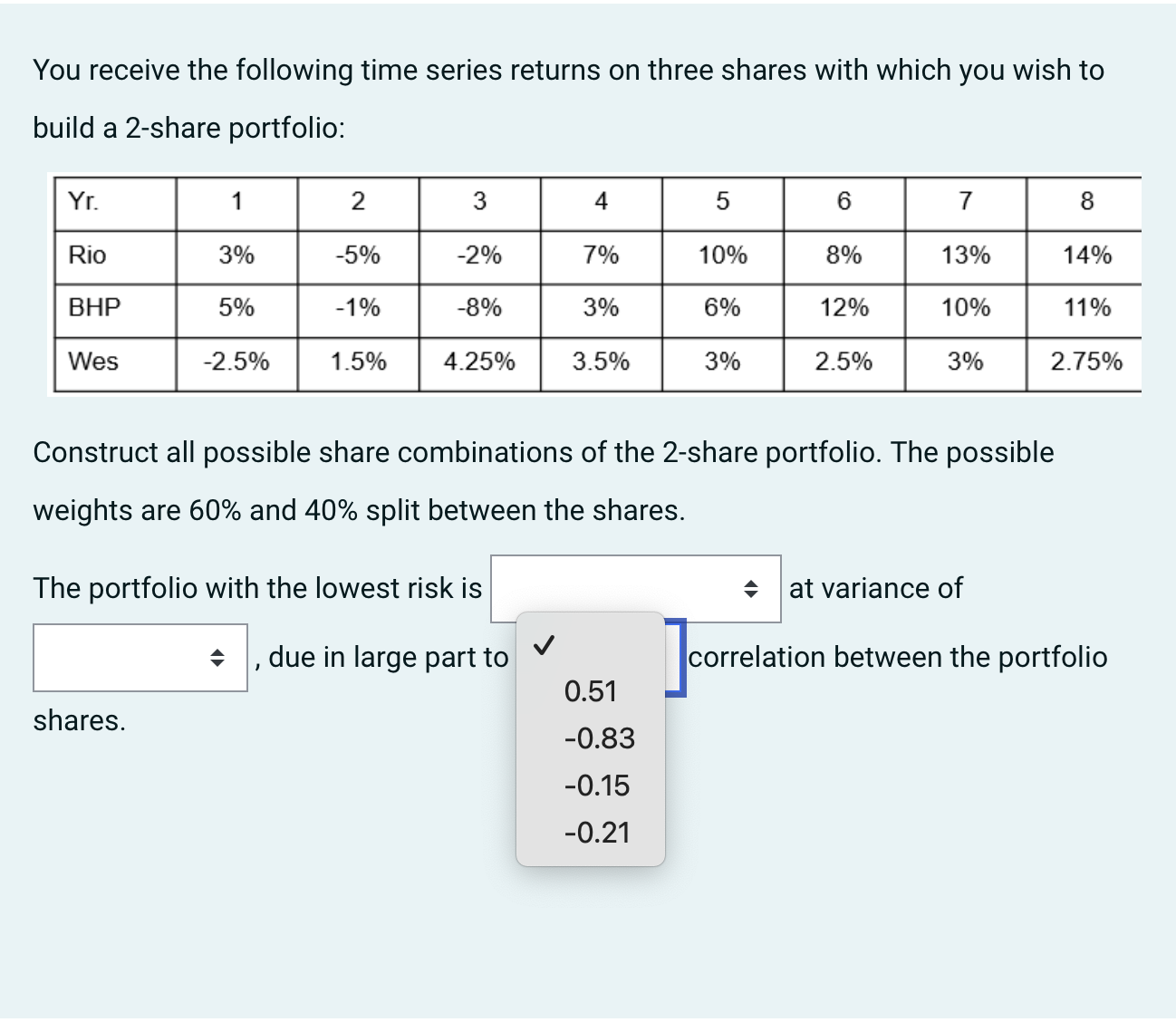

You receive the following time series returns on three shares with which you wish to build a 2-share portfolio: - - mummmmm Construct all possible

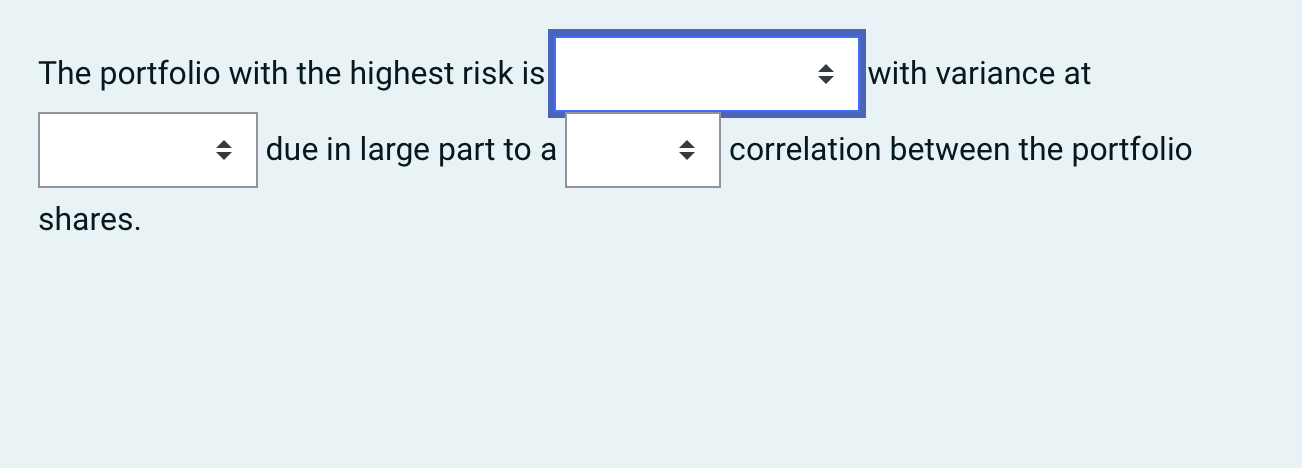

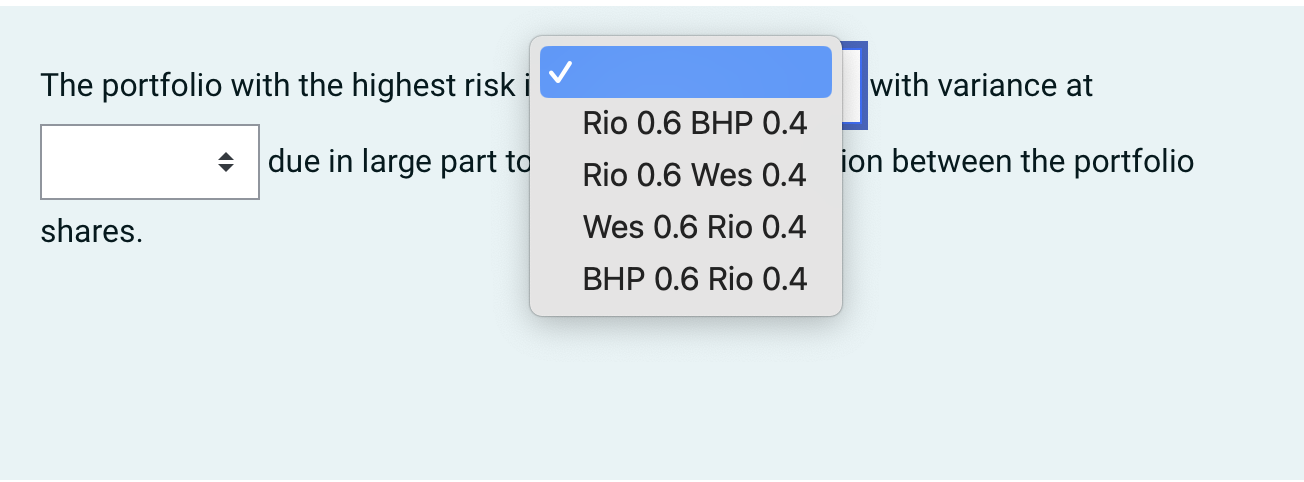

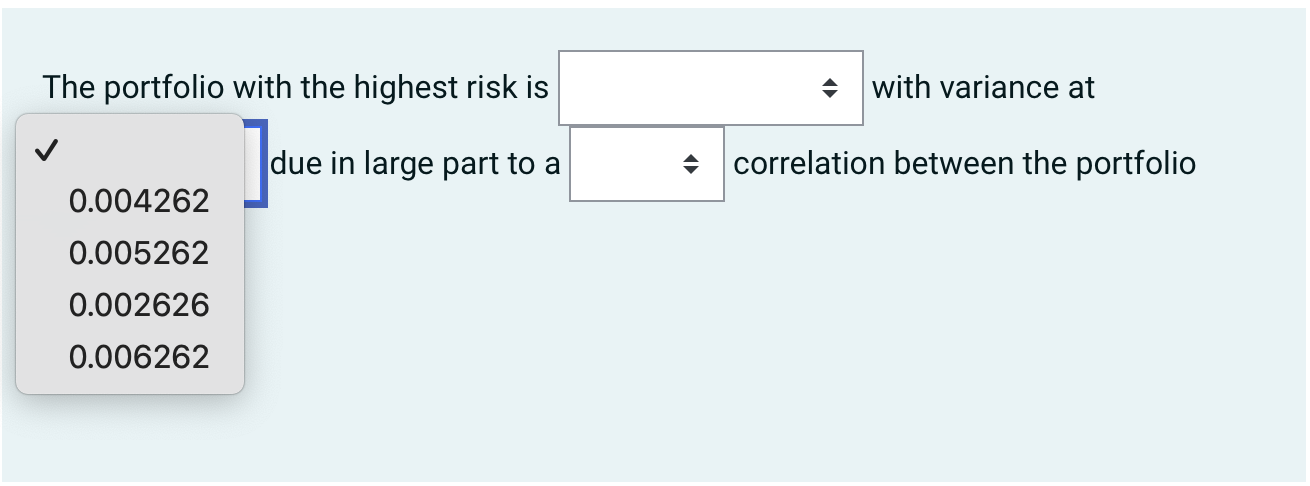

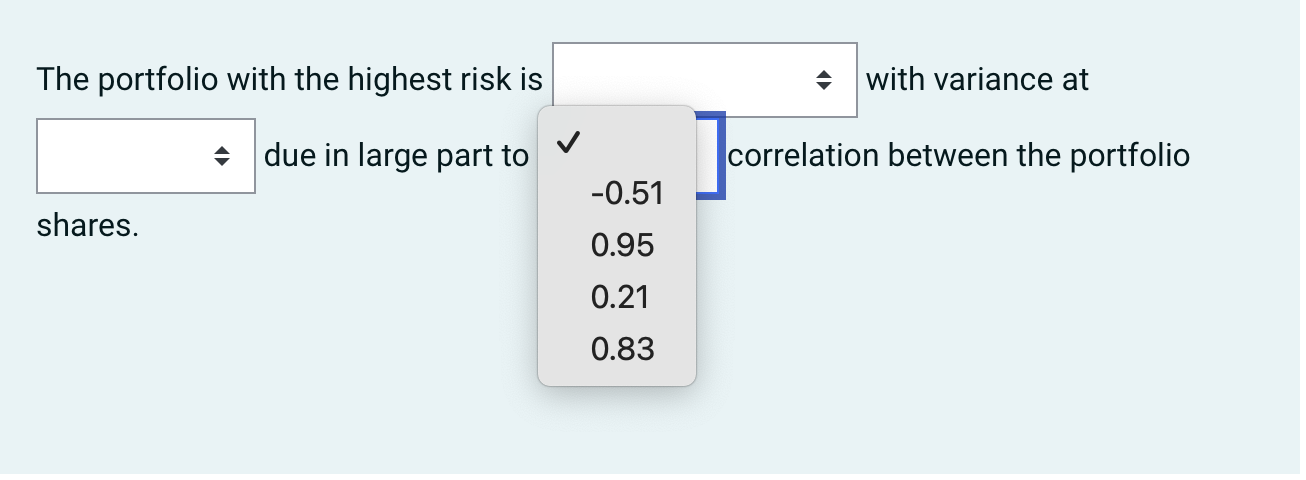

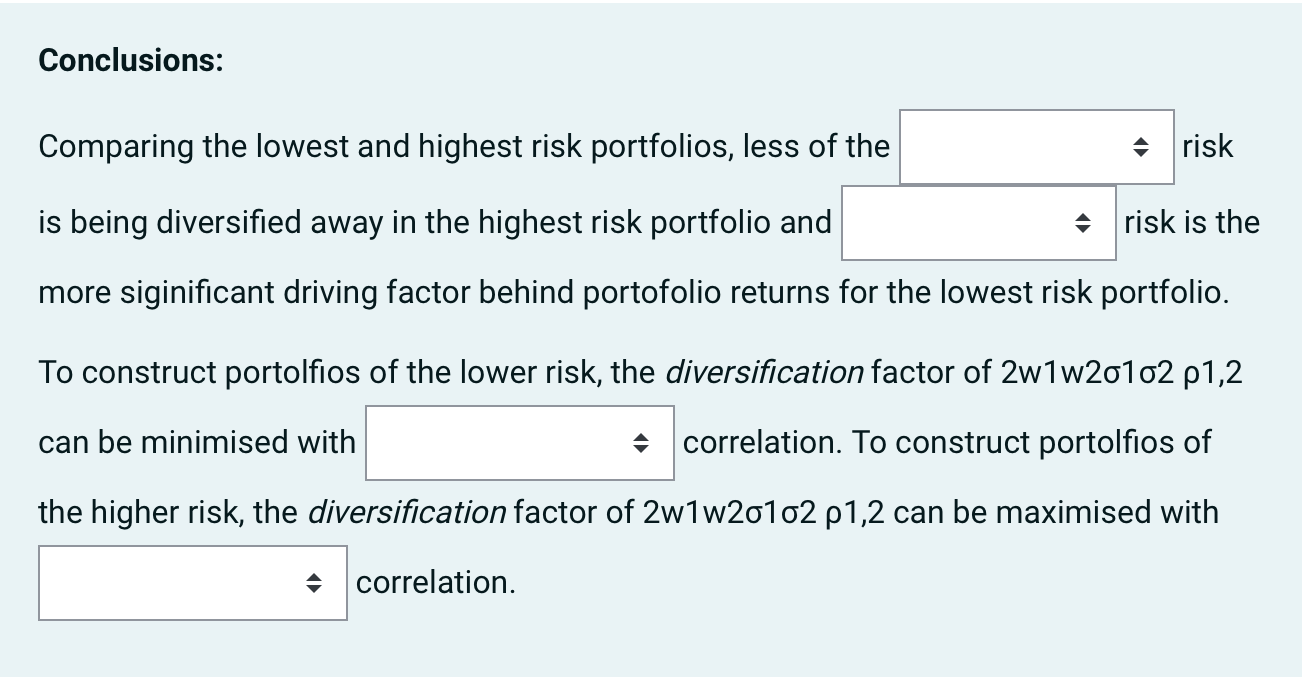

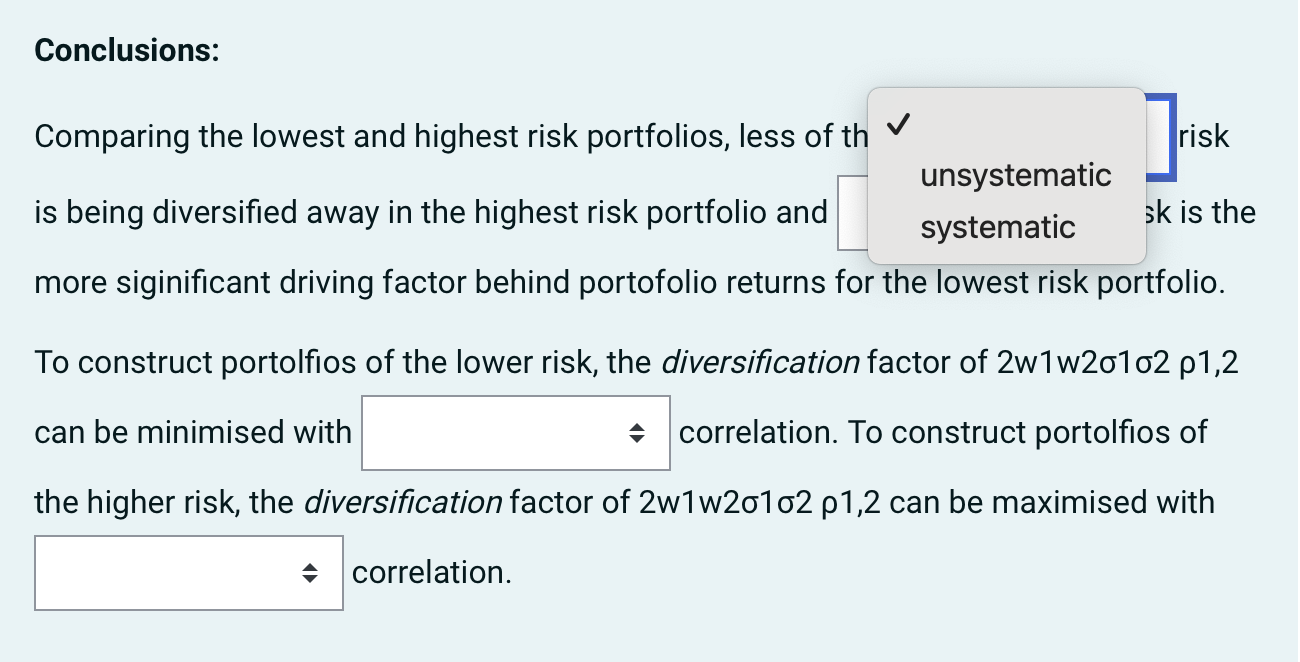

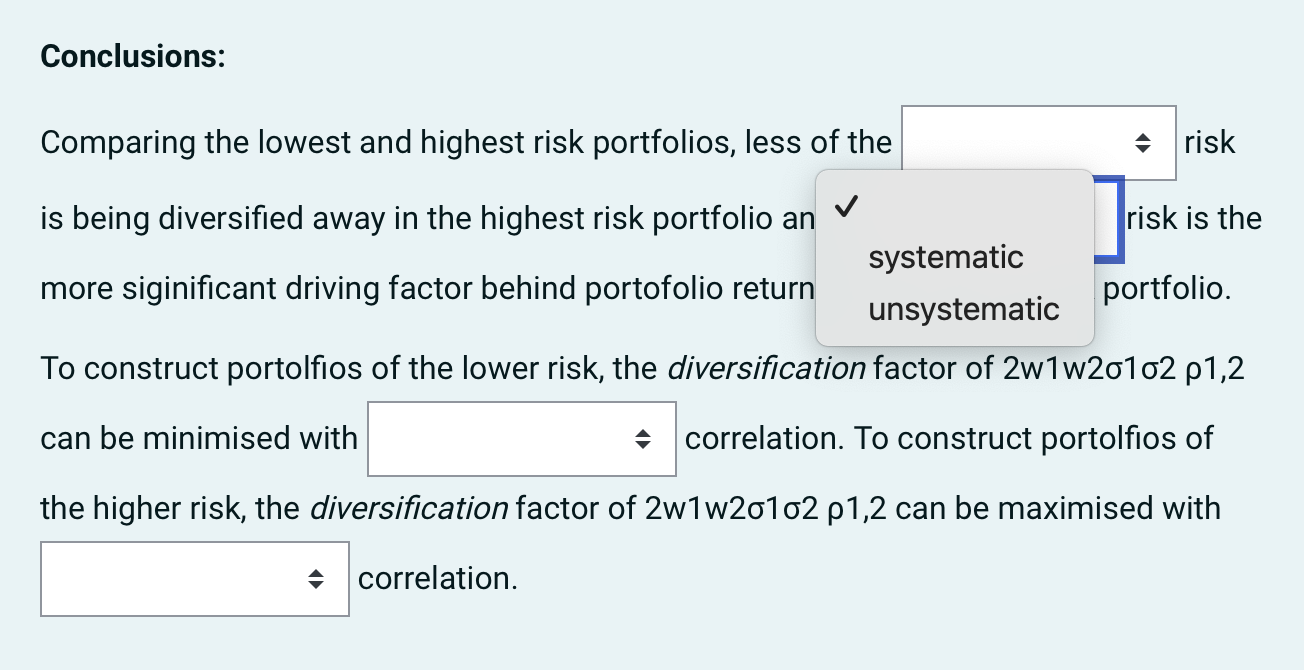

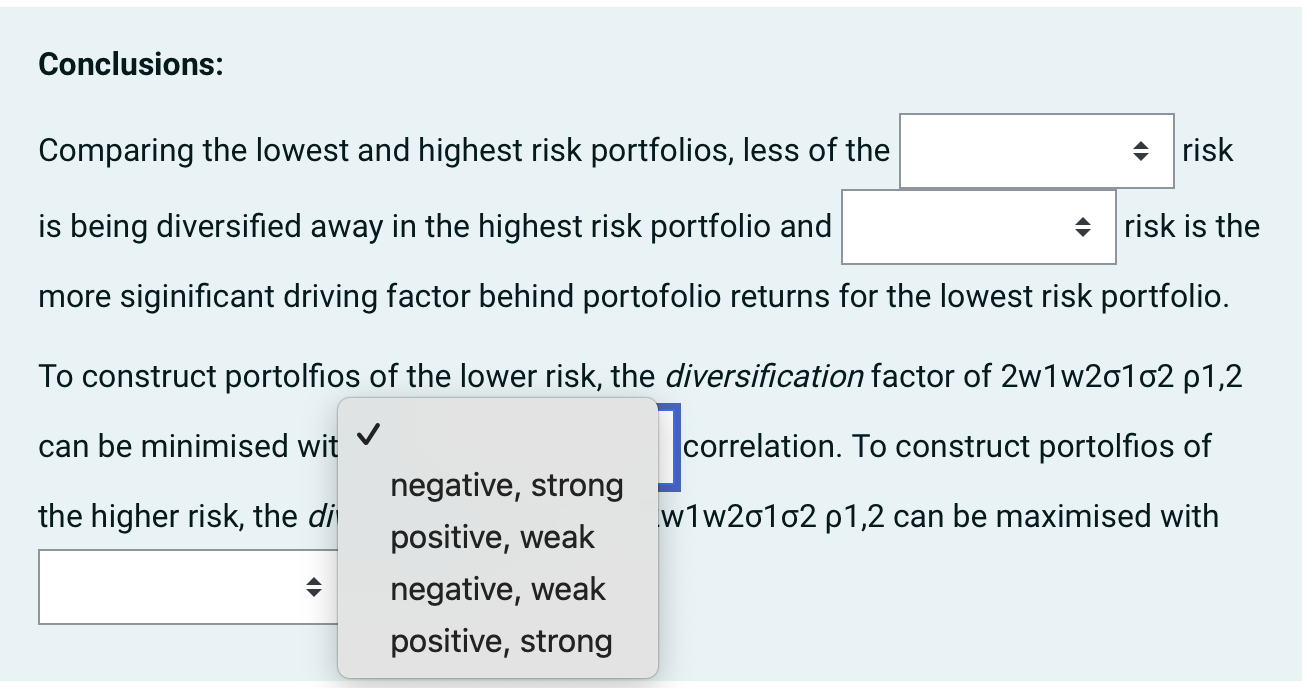

You receive the following time series returns on three shares with which you wish to build a 2-share portfolio: - "- mummmmm Construct all possible share combinations of the 2-share portfolio. The possible weights are 60% and 40% split between the shares. The portfolio with the lowest risk is _ at variance of - due in large part to a - correlation between the portfolio shares. You receive the following time series returns on three shares with which you wish to build a 2-share portfolio: Yr. 2 3 4 5 6 7 8 Rio 3% -5% -2% 7% 10% 8% 13% 14% BHP 5% -1% -8% 3% 6% 12% 10% 11% Wes -2.5% 1.5% 4.25% 3.5% 3% 2.5% 3% 2.75% Construct all possible share combinations of the 2-share portfolio. The possible weights are 60% and 40% split between the shares. The portfolio with the lowest risk i V at variance of Wes 0.6 Rio 0.4 + , due in large par Rio 0.6 Wes 0.4 ation between the portfolio shares. BHP 0.6 Wes 0.4 Wes 0.6 BHP 0.4You receive the following time series returns on three shares with which you wish to build a 2-share portfolio: m- Construct all possible share combinations of the 2-share portfolio. The possible weights are 60% and 40% split between the shares. The portfolio with the lowest risk is _ at variance of J ] due in large part to a - correlation between the portfolio 0.0002001 0.001094 0.0001611 0.0007841 You receive the following time series returns on three shares with which you wish to build a 2-share portfolio: ------ Construct all possible share combinations of the 2-share portfolio. The possible weights are 60% and 40% split between the shares. The portfolio with the lowest risk is at variance of - due in large part to "" correlation between the portfolio 0.51 shares. 0.83 -0.15 -0.21 The portfolio with the highest risk is with variance at due in large part to a shares. correlation between the portfolio The portfolio with the highest risk i V with variance at Rio 0.6 BHP 0.4 due in large part to Rio 0.6 Wes 0.4 ion between the portfolio shares. Wes 0.6 Rio 0.4 BHP 0.6 Rio 0.4The portfolio with the highest risk is _ with variance at '/ ]due in large part to a - correlation between the portfolio 0.004262 0.005262 0.002626 0.006262 The portfolio with the highest risk is with variance at due in large part to J -0.51 shares. 0.95 0.21 0.83 correlation between the portfolio Conclusions: Comparing the lowest and highest risk portfolios, less of the risk is being diversified away in the highest risk portfolio and risk is the more siginificant driving factor behind portofolio returns for the lowest risk portfolio. To construct portolfios of the lower risk, the diversification factor of 2w1w20102 p1,2 can be minimised with correlation. To construct portolfios of the higher risk, the diversification factor of 2w1w20102 p1,2 can be maximised with correlation.Conclusions: Comparing the lowest and highest risk portfolios, less of th V risk unsystematic is being diversified away in the highest risk portfolio and systematic sk is the more siginificant driving factor behind portofolio returns for the lowest risk portfolio. To construct portolfios of the lower risk, the diversification factor of 2w1w20102 p1,2 can be minimised with correlation. To construct portolfios of the higher risk, the diversification factor of 2w1w20102 p1,2 can be maximised with correlation.Conclusions: Comparing the lowest and highest risk portfolios, less of the risk J is being diversified away in the highest risk portfolio an risk is the systematic more siginicant driving factor behind portofolio return . portfolio. unsystematic To construct portolos of the lower risk, the diversication factor of 2w1w20102 p12 can be minimised with :l correlation. To construct portolflos of the higher risk, the diversification factor of 2W1 w201 02 p12 can be maximised with Conclusions: Comparing the lowest and highest risk portfolios, less of the risk is being diversified away in the highest risk portfolio and risk is the more siginificant driving factor behind portofolio returns for the lowest risk portfolio. To construct portolfios of the lower risk, the diversification factor of 2w1w20102 p1,2 can be minimised wit V correlation. To construct portolfios of negative, strong the higher risk, the di positive, weak w1w20102 p1,2 can be maximised with negative, weak positive, strongConclusions: Comparing the lowest and highest risk portfolios, less of the risk is being diversified away in the highest risk portfolio and risk is the more siginificant driving factor behind portofolio returns for the lowest risk portfolio. To construct portolfios of the lower risk, the diversification factor of 2w1w20102 p1,2 can be minimised with correlation. To construct portolfios of the higher risk, the diversification factor of 2w1w20102 p1,2 can be maximised with correlation. positive, strong positive, weak negative, weak negative, strong

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance