Answered step by step

Verified Expert Solution

Question

1 Approved Answer

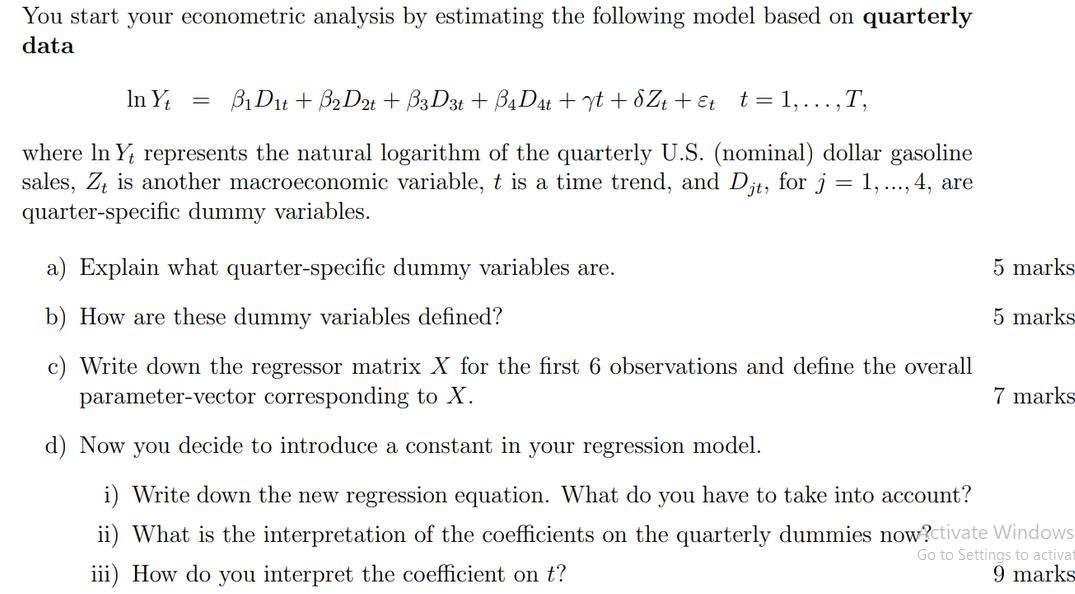

You start your econometric analysis by estimating the following model based on quarterly data In Yt = B1 D1t + B2D2t + B3D3t+ B4D4t

You start your econometric analysis by estimating the following model based on quarterly data In Yt = B1 D1t + B2D2t + B3D3t+ B4D4t + yt + 8Z + & t t = 1,..., T, where In Yt represents the natural logarithm of the quarterly U.S. (nominal) dollar gasoline sales, Z is another macroeconomic variable, t is a time trend, and Djt, for j = 1,...,4, are quarter-specific dummy variables. a) Explain what quarter-specific dummy variables are. b) How are these dummy variables defined? c) Write down the regressor matrix X for the first 6 observations and define the overall parameter-vector corresponding to X. 5 marks 5 marks 7 marks d) Now you decide to introduce a constant in your regression model. i) Write down the new regression equation. What do you have to take into account? ii) What is the interpretation of the coefficients on the quarterly dummies now?ctivate Windows iii) How do you interpret the coefficient on t? Go to Settings to activat 9 marks

Step by Step Solution

★★★★★

3.52 Rating (162 Votes )

There are 3 Steps involved in it

Step: 1

ANSWER a Quarterspecific dummy variables are a type of dummy variable that takes on a value of 1 for ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Business Statistics

Authors: Norean Sharpe, Richard Veaux, Paul Velleman

3rd Edition

978-0321944726, 321925831, 9780321944696, 321944720, 321944690, 978-0321925831