Answered step by step

Verified Expert Solution

Question

1 Approved Answer

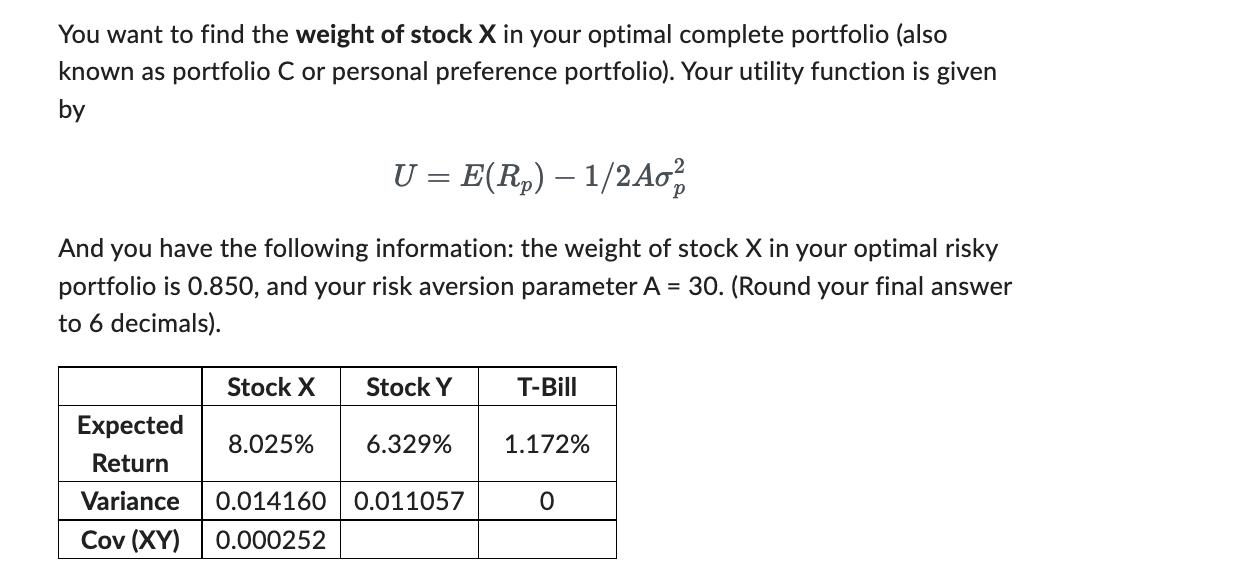

You want to find the weight of stock X in your optimal complete portfolio (also known as portfolio C or personal preference portfolio). Your

You want to find the weight of stock X in your optimal complete portfolio (also known as portfolio C or personal preference portfolio). Your utility function is given by U = E(R) - 1/2 Ao And you have the following information: the weight of stock X in your optimal risky portfolio is 0.850, and your risk aversion parameter A = 30. (Round your final answer to 6 decimals). Stock X Stock Y Expected Return Variance 0.014160 0.011057 Cov (XY) 0.000252 8.025% 6.329% T-Bill 1.172% 0

Step by Step Solution

There are 3 Steps involved in it

Step: 1

To find the weight of stock X in your optimal complete portfolio you can use the formula for the opt...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microeconomics

Authors: Austan Goolsbee, Steven Levitt, Chad Syverson

1st Edition

978-1464146978, 1464146977