Question

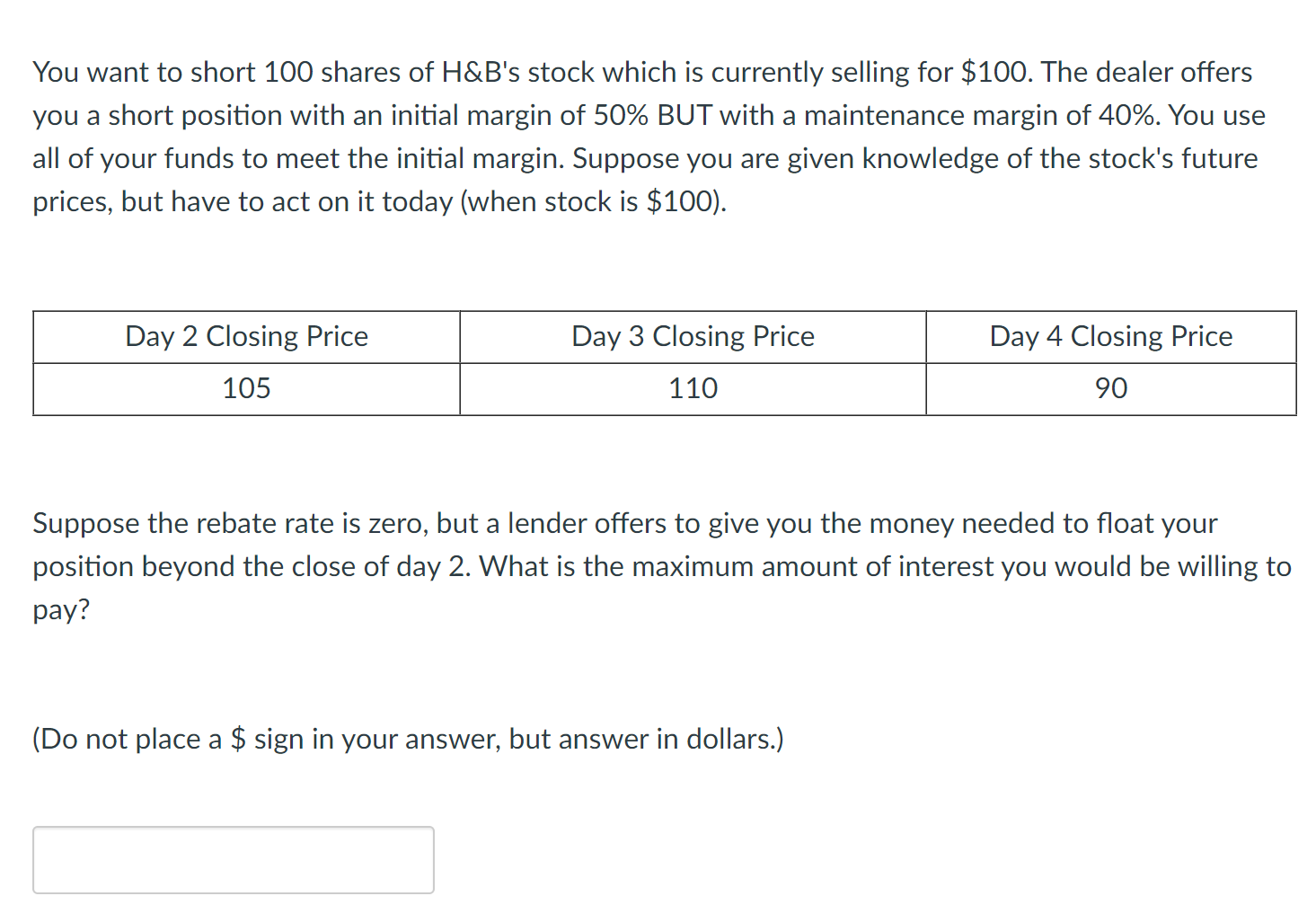

You want to short 100 shares of H&B's stock which is currently selling for $100. The dealer offers you a short position with an initial

You want to short 100 shares of H&B's stock which is currently selling for $100. The dealer offers you a short position with an initial margin of 50% BUT with a maintenance margin of 40%. You use all of your funds to meet the initial margin. Suppose you are given knowledge of the stock's future prices, but have to act on it today (when stock is $100).

Day 2 Closing Price: 105

Day 3 Closing Price: 110

Day 4 Closing Price: 90

Suppose the rebate rate is zero, but a lender offers to give you the money needed to float your position beyond the close of day 2. What is the maximum amount of interest you would be willing to pay? (Do not place a $ sign in your answer, but answer in dollars.)

You want to short 100 shares of H&B's stock which is currently selling for $100. The dealer offers you a short position with an initial margin of 50% BUT with a maintenance margin of 40%. You use all of your funds to meet the initial margin. Suppose you are given knowledge of the stock's future prices, but have to act on it today (when stock is $100). Day 2 Closing Price Day 3 Closing Price Day 4 Closing Price 105 110 90 Suppose the rebate rate is zero, but a lender offers to give you the money needed to float your position beyond the close of day 2. What is the maximum amount of interest you would be willing to pay? (Do not place a $ sign in your answer, but answer in dollars.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Barry Ned Crypto

Authors: Barry D Ned

1st Edition

979-8857241233