Question

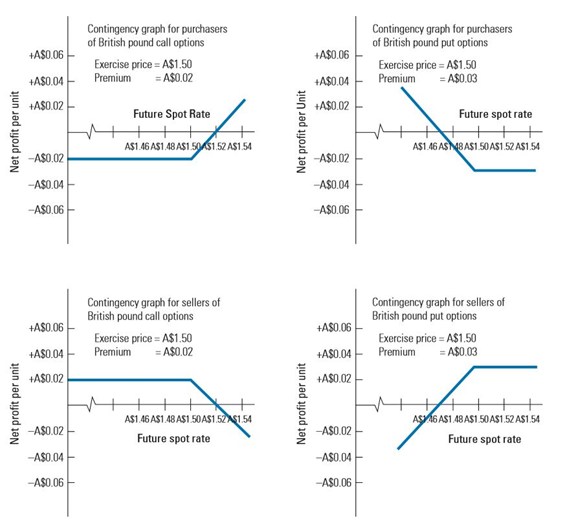

You want you to buy 1.91 million British pounds (GBP) using call options and foreign exchange market. The following four figures provide the market information

You want you to buy 1.91 million British pounds (GBP) using call options and foreign exchange market. The following four figures provide the market information on the GBP options, which expires in 5-month. How much can you make a net profit or a net loss for GBP1.91 million if the spot rate is A$1.6732 at the maturity (i.e., after 5 months)? (enter the whole number)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Oxford Handbook Of Hedge Funds

Authors: Douglas Cumming, Sofia Johan, Geoffrey Wood

1st Edition

0198840950, 978-0198840954