Answered step by step

Verified Expert Solution

Question

1 Approved Answer

You want your portfolio beta to be 1.20. Currently, your portfolio consists of $3,000 invested in stock A with a beta of 1.64 and $2,000

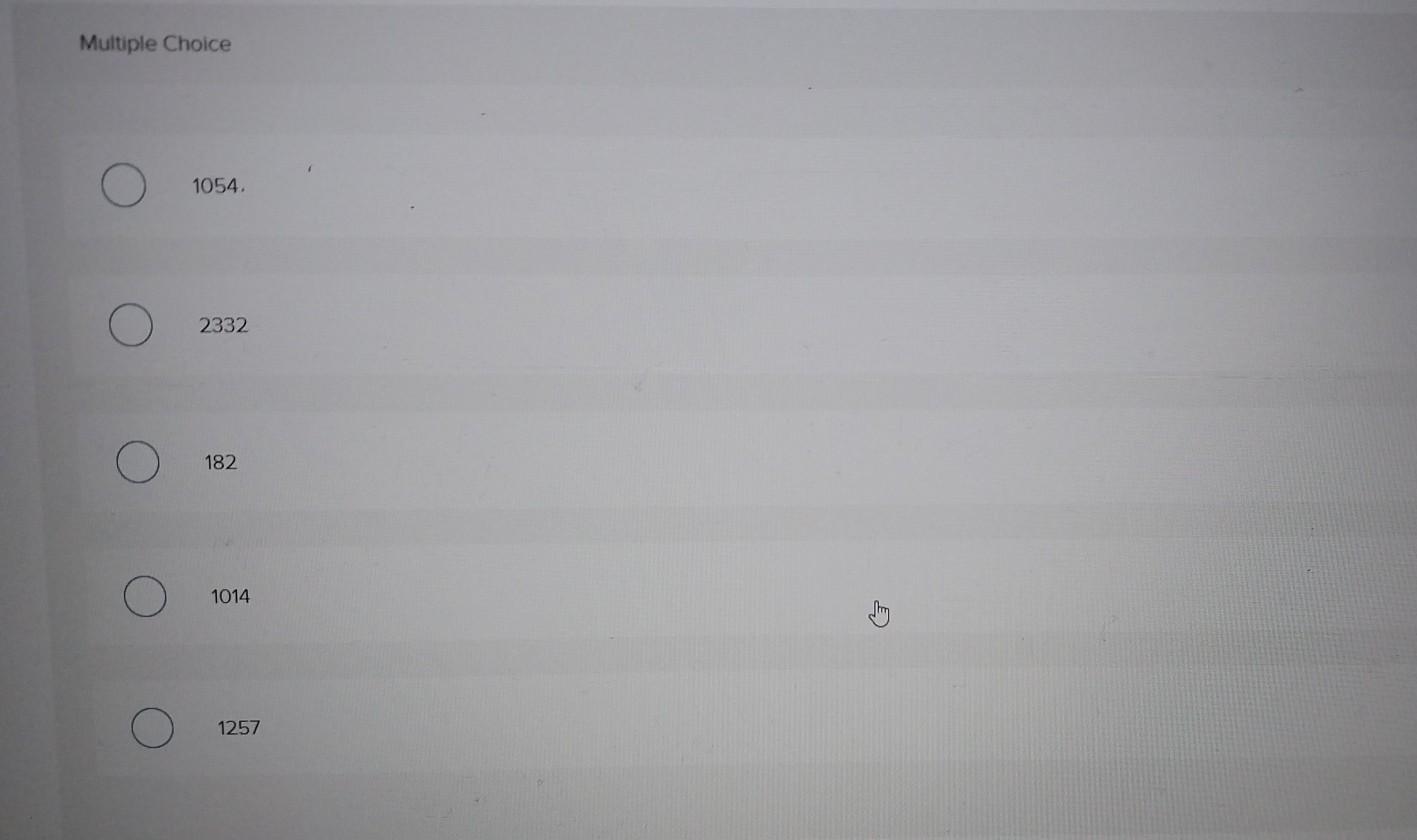

You want your portfolio beta to be 1.20. Currently, your portfolio consists of $3,000 invested in stock A with a beta of 1.64 and $2,000 in stock B with a beta of 0.67 . You have another $5,000 to invest and want to divide it between an asset with a beta of 1.44 and a risk-free asset. How much should you invest in the risk-free asset? Multiple Choice 1054. 2332 182 1014 1257

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asset Allocation And International Investments

Authors: G. Gregoriou

1st Edition

023001917X,0230626513