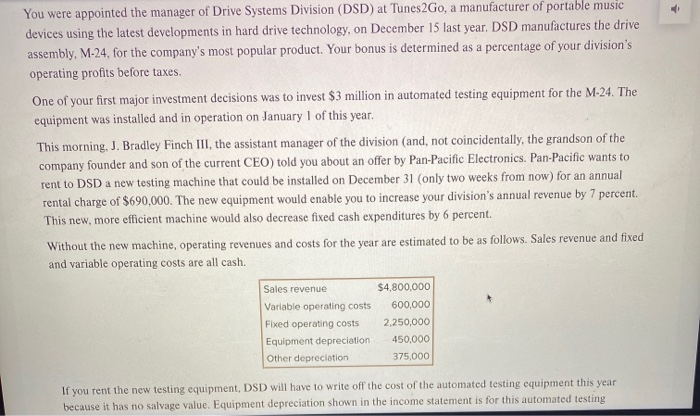

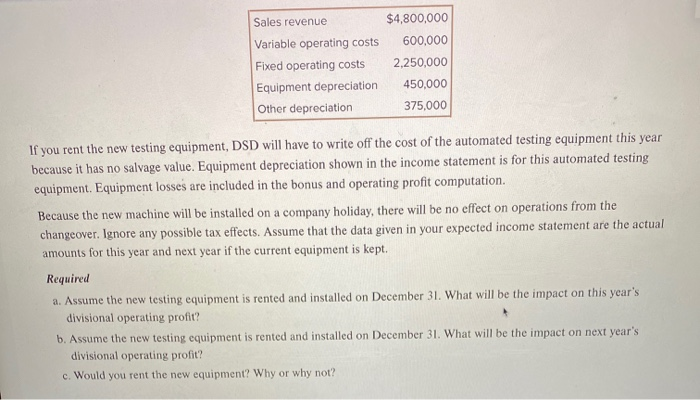

You were appointed the manager of Drive Systems Division (DSD) at Tunes2Go, a manufacturer of portable music devices using the latest developments in hard drive technology, on December 15 last year. DSD manufactures the drive assembly, M-24, for the company's most popular product. Your bonus is determined as a percentage of your division's operating profits before taxes. One of your first major investment decisions was to invest $3 million in automated testing equipment for the M-24. The equipment was installed and in operation on January 1 of this year. This morning. J. Bradley Finch III, the assistant manager of the division (and, not coincidentally, the grandson of the company founder and son of the current CEO) told you about an offer by Pan-Pacific Electronics. Pan-Pacific wants to rent to DSD a new testing machine that could be installed on December 31 (only two weeks from now) for an annual rental charge of $690,000. The new equipment would enable you to increase your division's annual revenue by 7 percent, This new, more efficient machine would also decrease fixed cash expenditures by 6 percent. Without the new machine, operating revenues and costs for the year are estimated to be as follows. Sales revenue and fixed and variable operating costs are all cash. Sales revenue Variable operating costs Fixed operating costs Equipment depreciation Other depreciation $4,800,000 600,000 2,250,000 450,000 375,000 If you rent the new testing equipment, DSD will have to write of the cost of the automated testing equipment this year because it has no salvage value. Equipment depreciation shown in the income statement is for this automated testing Sales revenue Variable operating costs Fixed operating costs Equipment depreciation Other depreciation $4,800,000 600,000 2,250,000 450,000 375,000 If you rent the new testing equipment, DSD will have to write off the cost of the automated testing equipment this year because it has no salvage value. Equipment depreciation shown in the income statement is for this automated testing equipment. Equipment losses are included in the bonus and operating profit computation. Because the new machine will be installed on a company holiday, there will be no effect on operations from the changeover. Ignore any possible tax effects. Assume that the data given in your expected income statement are the actual amounts for this year and next year if the current equipment is kept. Required a. Assume the new testing equipment is rented and installed on December 31. What will be the impact on this year's divisional operating profit? b. Assume the new testing equipment is rented and installed on December 31. What will be the impact on next year's divisional operating profit? c. Would you rent the new equipment? Why or why not