Your assignment should be submitted with report format. The written report with single-spaced, double between paragraphs about your finds and

analysis. it should not be more than 600 words.

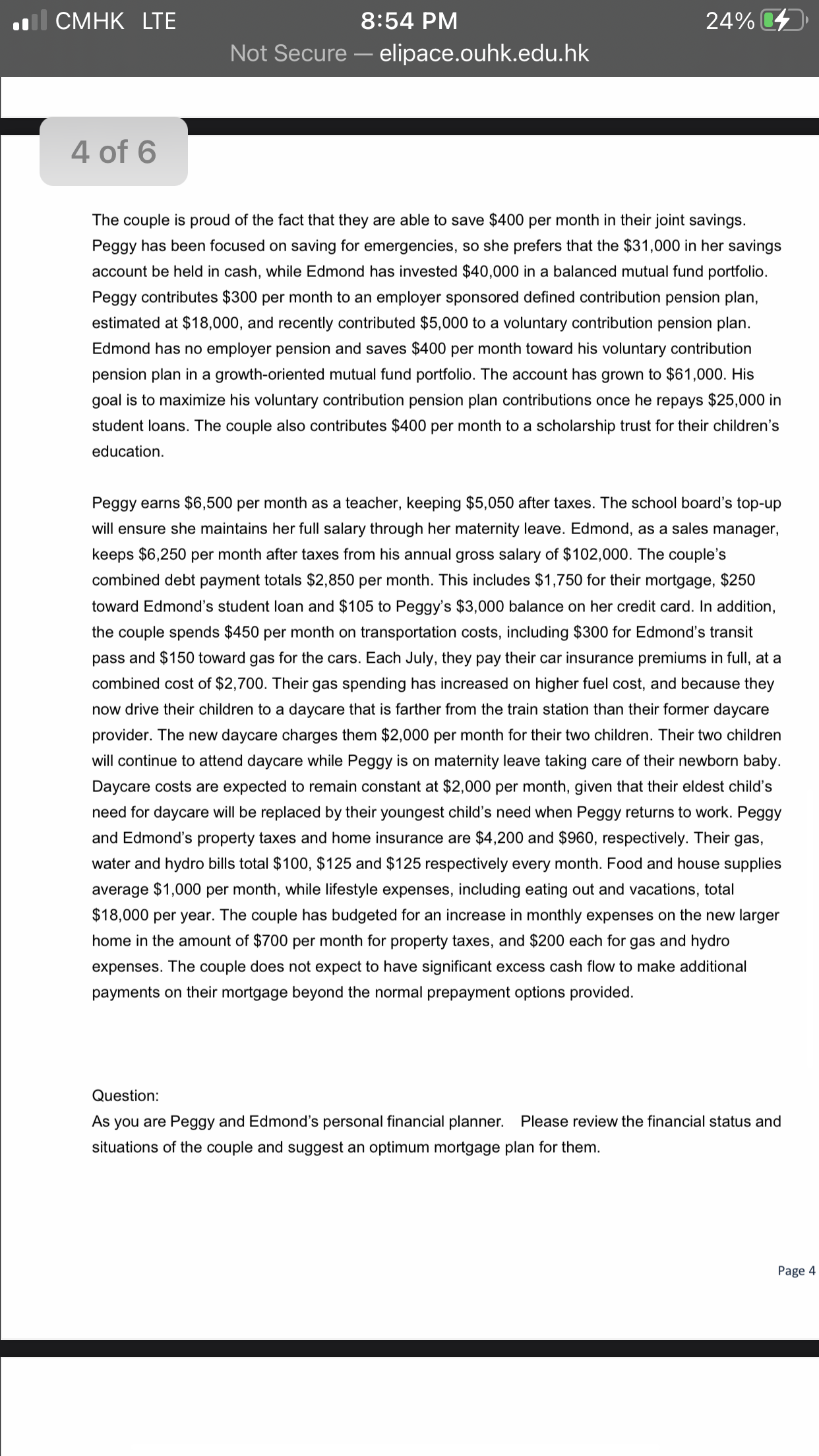

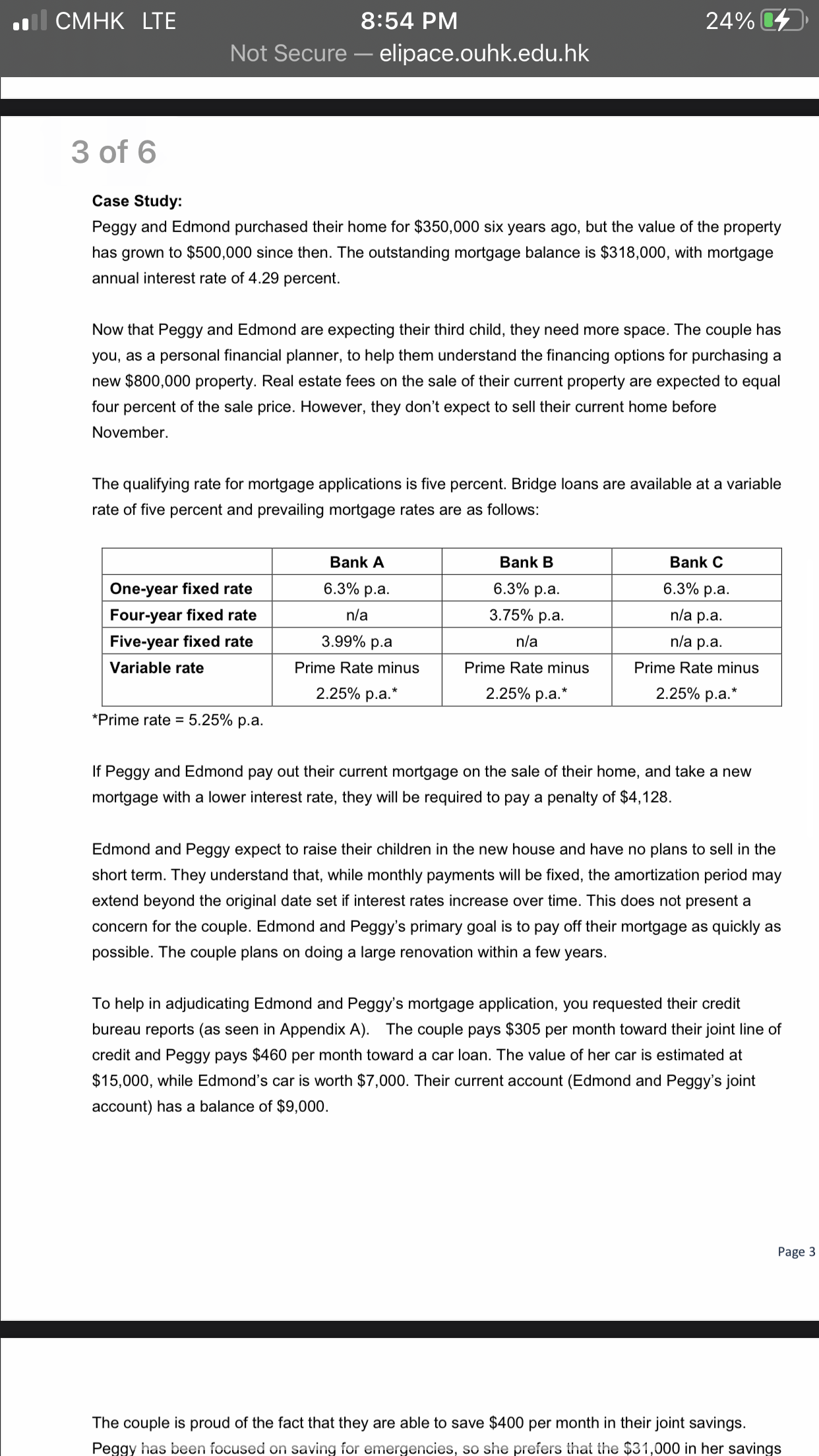

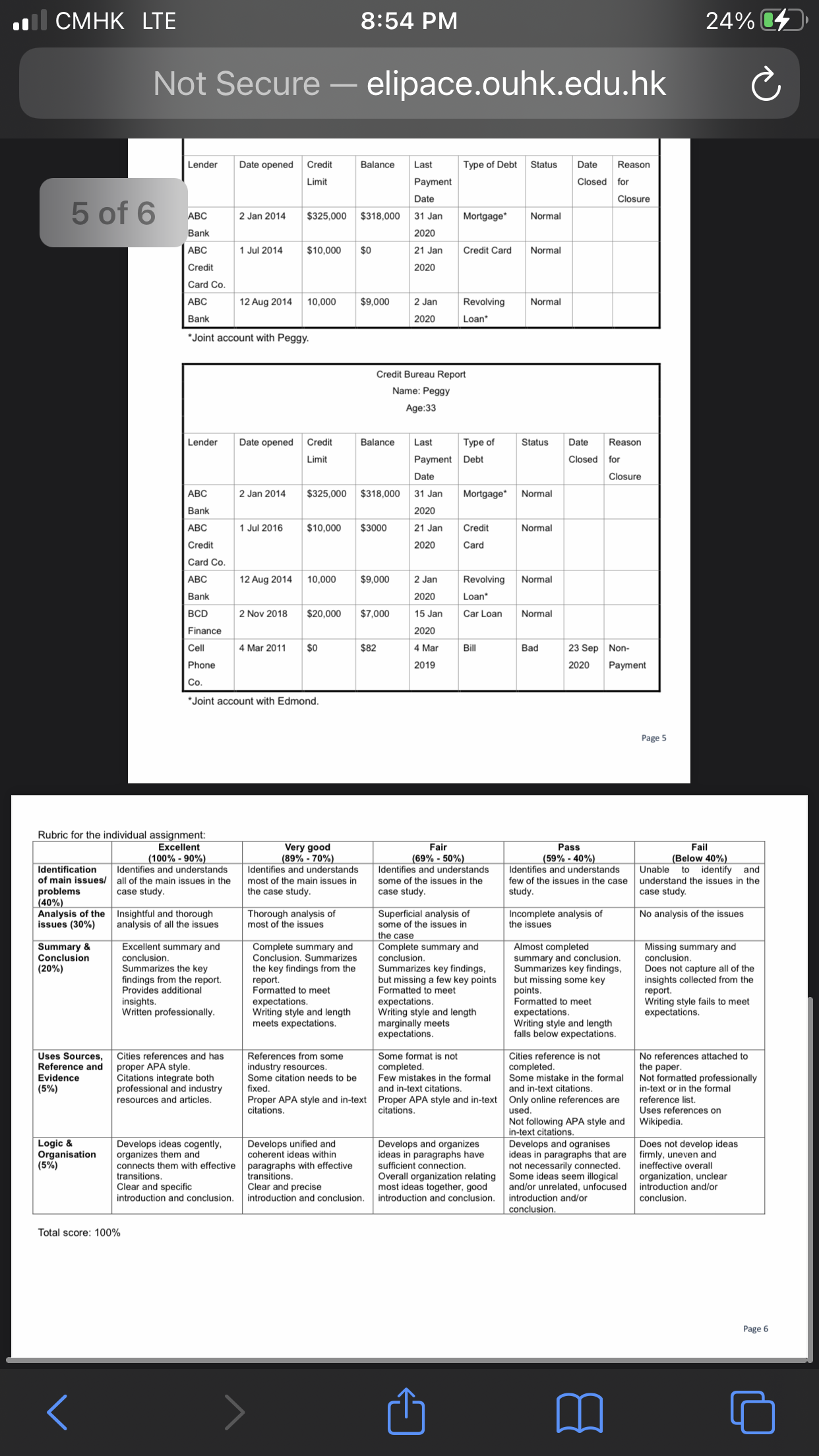

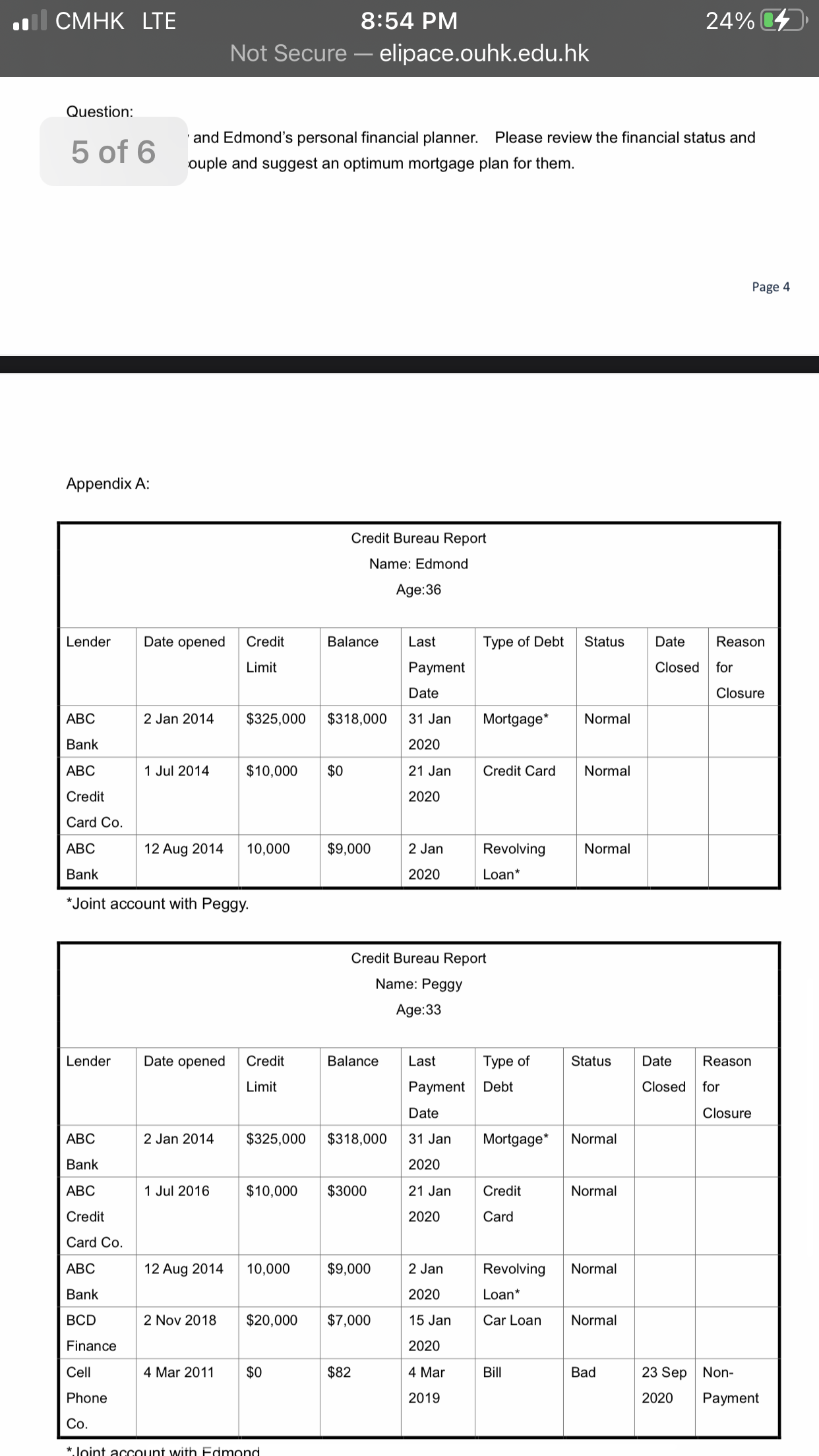

CMHK LTE 854 PM elipace.ouhk.edu.hk 4of6 The couple is proud of the fact that they are able to save $400 per month in theirjoint savings. Peggy has been focused on saving for emergencies, so she prefers that the $31,000 in her savings account be held in cash, while Edmond has invested $40,000 in a balanced mutual fund portfolio. Peggy contributes $300 per month to an employer sponsored dened contribution pension plan, estimated at $18,000, and recently contributed $5,000 to a voluntary contribution pension plan. Edmond has no employer pension and saves $400 per month toward his voluntary contribution pension plan in a growth-oriented mutual fund portfolio. The account has grown to $61,000. His goal is to maximize his voluntary contribution pension plan contributions once he repays $25,000 in student loans. The couple also contributes $400 per month to a scholarship trust for their children's education. Peggy earns $6,500 per month as a teacher, keeping $5,050 after taxes. The school board's top-up will ensure she maintains her full salary through her maternity leave. Edmond, as a sales manager, keeps $6,250 per month after taxes from his annual gross salary of $102,000. The couple's combined debt payment totals $2,850 per month. This includes $1 ,750 for their mortgage, $250 toward Edmond's student loan and $105 to Peggy's $3,000 balance on her credit card. In addition, the couple spends $450 per month on transportation costs, including $300 for Edmond's transit pass and $150 toward gas for the cars. Each July, they pay their car insurance premiums in full, at a combined cost of $2,700. Their gas spending has increased on higher fuel cost, and because they now drive their children to a daycare that is farther from the train station than their former daycare provider. The new daycare charges them $2,000 per month for their two children. Their two children will continue to attend daycare while Peggy is on maternity leave taking care of their newborn baby. Daycare costs are expected to remain constant at $2,000 per month, given that their eldest child's need for daycare will be replaced by their youngest child's need when Peggy returns to work. Peggy and Edmond's property taxes and home insurance are $4,200 and $960, respectively. Their gas, water and hydro bills total $100, $125 and $125 respectively every month. Food and house supplies average $1,000 per month, while lifestyle expenses, including eating out and vacations, total $18,000 per year. The couple has budgeted for an increase in monthly expenses on the new larger home in the amount of $700 per month for property taxes, and $200 each for gas and hydro expenses. The couple does not expect to have significant excess cash flow to make additional payments on their mortgage beyond the normal prepayment options provided. Question: As you are Peggy and Edmond's personal nancial planner. Please review the nancial status and situations of the couple and suggest an optimum mortgage plan for them. Page 4 .I CMHK LTE 854 PM elipace.ouhk.edu.hk 3of6 Case Study: Peggy and Edmond purchased their home for $350,000 six years ago, but the value of the property has grown to $500,000 since then. The outstanding mortgage balance is $318,000, with mortgage annual interest rate of 4.29 percent. Now that Peggy and Edmond are expecting their third child, they need more space. The couple has you, as a personal nancial planner, to help them understand the nancing options for purchasing a new $800,000 property. Real estate fees on the sale of their current property are expected to equal four percent of the sale price. However, they don't expect to sell their current home before November. The qualifying rate for mortgage applications is ve percent. Bridge loans are available at a variable rate of five percent and prevailing mortgage rates are as follows: One-year fixed rate 6.3% p.a. 6.3% p.a. 6.3% p.a. Four-year xed rate nla 3.75% p.a. nla p.a. Five-year xed rate 3.99% pa nla nla p.a. Variable rate Prime Rate minus Prime Rate minus Prime Rate minus 2.25% p.a.* 2.25% p.a.* 2.25% p.a.* *Prime rate = 5.25% p.a. If Peggy and Edmond pay out their current mortgage on the sale of their home, and take a new mortgage with a lower interest rate, they will be required to pay a penalty of $4,128. Edmond and Peggy expect to raise their children in the new house and have no plans to sell in the short term. They understand that, while monthly payments will be fixed, the amortization period may extend beyond the original date set if interest rates increase over time. This does not present a concern for the couple. Edmond and Peggy's primary goal is to pay off their mortgage as quickly as possible. The couple plans on doing a large renovation within a few years. To help in adjudicating Edmond and Peggy's mortgage application, you requested their credit bureau reports (as seen in Appendix A). The couple pays $305 per month toward theirjoint line of credit and Peggy pays $460 per month toward a car loan. The value of her car is estimated at $15,000, while Edmond's car is worth $7,000. Their current account (Edmond and Peggy's joint account) has a balance of $9,000. Page 3 The couple is proud of the fact that they are able to save $400 per month in theirjoint savings. Peggy has been focused on saving for emergencies, so she prefers that the $31,000 in her savings CMHK LTE 8:54 PM 24% Not Secure - elipace.ouhk.edu.hk C Lender Date opened Credit Balance Last Type of Debt Status Date Reason Limit Payment Closed for 5 of 6 Date Closure ABC 2 Jan 2014 $325,000 $318,000 31 Jan Mortgage Normal Bank 2020 ABC 1 Jul 2014 $10,000 SO 21 Jan Credit Card Normal Credit 2020 Card Co. ABC 12 Aug 2014 10,000 $9,000 2 Jan Revolving Normal Bank 2020 Loan* *Joint account with Peggy Credit Bureau Report Name: Peggy Age:33 Lender Date opened Credit Balance Last Type of Status Date Reason Limit Payment Debt Closed for Date Closure ABC 2 Jan 2014 $325,000 $318,000 31 Jan Mortgage" Normal Bank 2020 ABC 1 Jul 2016 $10,000 $3000 21 Jan Credit Normal Credit 2020 Card Card Co. ABC 12 Aug 2014 10,000 $9,000 2 Jan Revolving Normal Bank 2020 Loan BCD 2 Nov 2018 $20,000 $7,000 15 Jan Car Loan Normal Finance 2020 Cell 4 Mar 2011 SO $82 4 Ma Bill Bad 23 Sep Non- Phone 2019 2020 Payment Co. *Joint account with Edmond Page 5 Rubric for the individual assignment: Excellent Very good Fair Pass Fail (100% - 90%) (89% - 70%) (69% - 50%) (59% - 40%) (Below 40%) Identification Identifies and understands Identifies and understands Identifies and understands Identifies and understands Unable t identify and of main issues/ | all of the main issues in the most of the main issues in some of the issues in the few of the issues in the case | understand the issues in the problems case study. the case study. case study study. case study. (40%) Analysis of the Insightful and thorough Thorough analysis of Superficial analysis of Incomplete analysis of No analysis of the issues ssues (30%) analysis of all the issues most of the issues some of the issues in the issues the case Summary & Excellent summary and Complete summary and Complete summary and Almost completed Missing summary and Conclusion conclusion. Conclusion. Summarizes conclusion. summary and conclusion. conclusion. (20%) Summarizes the key the key findings from the Summarizes key findings, Summarizes key findings, Does not capture all of the findings from the report. report. but missing a few key points but missing some key insights collected from the Provides additional Formatted to meet Formatted to meet points. report. insights. expectations. expectations. Formatted to meet Writing style fails to meet Written professionally. Writing style and length Writing style and length expectations. expectations. meets expectations. marginally meets Writing style and length expectations. falls below expectations Uses Sources, Cities references and has References from some Some format is not Cities reference is not No references attached to Reference and proper APA style. ndustry resources. completed. completed. the paper. Evidence Citations integrate both Some citation needs to be Few mistakes in the formal Some mistake in the formal Not formatted professionally (5%) professional and industry fixed. and in-text citations. and in-text citations. n-text or in the formal resources and articles. Proper APA style and in-text Proper APA style and in-text Only online references are reference list. citations. citations. used. Uses references on Not following APA style and Wikipedia. in-text citations. Logic & Does not develop ideas Organisation Develops ideas cogently, Develops unified and Develops and organizes Develops and ogranises organizes them and coherent ideas within ideas in paragraphs have ideas in paragraphs that are firmly, uneven and (5%) connects them with effective paragraphs with effective sufficient connection. not necessarily connected. ineffective overall transitions. transitions. Overall organization relating Some ideas seem illogical organization, unclear Clear and specific Clear and precise most ideas together, good and/or unrelated, unfocused introduction and/or introduction and conclusion. introduction and conclusion. introduction and conclusion. introduction and/or conclusion. conclusion. Total score: 100% Page 6 mCMHK LTE 8:54 PM 24% Not Secure - elipace.ouhk.edu.hk Question: 5 of 6 and Edmond's personal financial planner. Please review the financial status and ouple and suggest an optimum mortgage plan for them. Page 4 Appendix A: Credit Bureau Report Name: Edmond Age:36 Lender Date opened Credit Balance Last Type of Debt Status Date Reason Limit Payment Closed for Date Closure ABC 2 Jan 2014 $325,000 $318,000 31 Jan Mortgage* Normal Bank 2020 ABC 1 Jul 2014 $10,000 $0 21 Jan Credit Card Normal Credit 2020 Card Co. ABC 12 Aug 2014 10,000 $9,000 2 Jan Revolving Normal Bank 2020 Loan* Joint account with Peggy. Credit Bureau Report Name: Peggy Age:33 Lender Date opened Credit Balance Last Type of Status Date Reason Limit Payment Deb Closed for Date Closure ABC 2 Jan 2014 $325,000 $318,000 31 Jan Mortgage* Normal Bank 2020 ABC 1 Jul 2016 $10,000 $3000 21 Jan Credit Normal Credit 2020 Card Card Co. ABC 12 Aug 2014 10,000 $9,000 2 Jan Revolving Normal Bank 2020 Loan* BCD 2 Nov 2018 $20,000 $7,000 15 Jan Car Loan Normal Finance 2020 Cell 4 Mar 2011 $0 $82 4 Mar Bill Bad 23 Sep Non- Phone 2019 2020 Payment CoCMHK LTE 8:54 PM 23% 4 Not Secure - elipace.ouhk.edu.hk 1 of 6 097EF Fundamentals of Financial Planning I Assignment: Case Study Marks for this assessment: 100% (20% of the total score of this course) Assignment Due Date: 30" December 2020 Assignment Information and Specification This case study is to provide hand on experience to synthesise the course topics that you have learnt throughout the semester by apply them to authentic scenarios. What you need to do: 1. Your assignment should be submitted with report format. 2. The assignment is in English. 3. Submit your written report on 30" December 2020 (Wed). 4. Use A4 size paper in this assignment. 5. Prepare a written report with single-spaced, double between paragraphs about your finds and analysis. 6. Not more than 600 words. 7. Use the American Psychological Association (APA) style of referencing to acknowledge sources used in your assignment. 8. You should submit your assignment to OLE. Report format: 1. Title Section/Report Cover Page: This includes student name, student ID and the report due date. 2. Summary: It needs to be short as it is a general overview of the report. Some people will read the summary and only skim the report, so make sure you include all the relevant information. It would be best to write this last so you will include everything, even the points that might be added at the last minute. (This part should be half page.) 3. Findings: You should include the result of calculations and financial status/situations. (This part should be 2 to 6 pages, depending on the number of graphs, chart, information, etc. that were reasonable.) 4. Conclusion and recommendation: It provides a summary of your findings and investigations and suggests appropriate actions. (This part should be 1-3 pages.) 5. Appendices. Page 1 Guideline for the assignment When your assignment is turned in, it should be done on a word processor in correct format. will be graded on the origin