Question

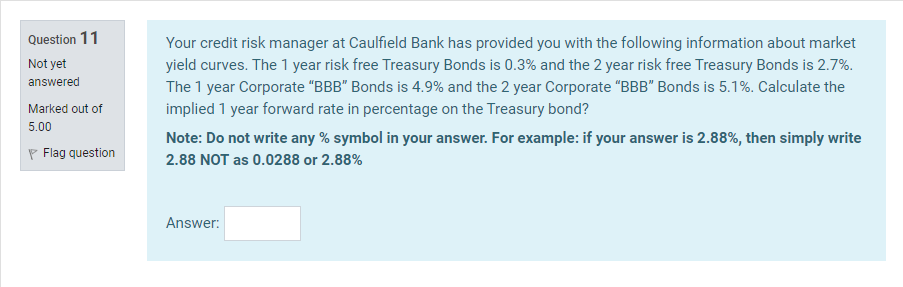

Your credit risk manager at Caulfield Bank has provided you with the following information about market yield curves. The 1 year risk free Treasury Bonds

Your credit risk manager at Caulfield Bank has provided you with the following information about market yield curves. The 1 year risk free Treasury Bonds is 0.3% and the 2 year risk free Treasury Bonds is 2.7%. The 1 year Corporate BBB Bonds is 4.9% and the 2 year Corporate BBB Bonds is 5.1%. Calculate the implied 1 year forward rate in percentage on the Treasury bond?

Note: Do not write any % symbol in your answer. For example: if your answer is 2.88%, then simply write 2.88 NOT as 0.0288 or 2.88%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of The Political Economy Of Financial Crises

Authors: Martin H. Wolfson, Gerald A. Epstein

1st Edition

0199757232, 978-0199757237