Question

Your manager was so impressed with your work analyzing the return and standard deviations of the 12 stocks from Chapter 10 that he would like

Your manager was so impressed with your work analyzing the return and standard deviations of the 12 stocks from Chapter 10 that he would like you to continue your analysis. Specifically, he wants you to update the stock portfolio by:

- Rebalancing the portfolio with the optimum weights that will provide the best risk and return combinations for the new 12-stock portfolio.

- Determining the improvement in the return and risk that would result from these optimum weights compared to the current method of equally weighting the stocks in the portfolio.

Steps:

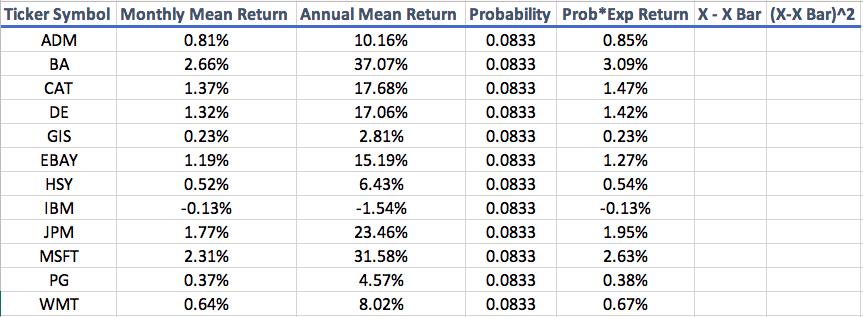

Use the Solver function in Excel to perform this analysis (the time-consuming alternative is to find the optimum weights by trial and error). 1. Begin with the equally weighted portfolio analyzed in Chapter 10. Establish the portfolio returns for the stocks in the portfolio using a formula that depends on the portfolio weights. Initially, these weights will all equal 1/12. You would like to allow the portfolio weights to vary, so you will need to list the weights for each stock in separate cells, and establish another cell that sums the weights of the stocks. The portfolio returns for each month must reference these weights for Excel Solver to be useful.

Compute the values for the monthly mean return and standard deviation of the portfolio. Convert these values to annual numbers (as you did in Chapter 10) for easier interpretation.

---I have the data in a workbook but I am unsure of how to use Solver in Excel.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Technical Analysis Of Stock Trends

Authors: Robert D. Edwards, John Magee

1st Edition

1607962233, 978-1607962236