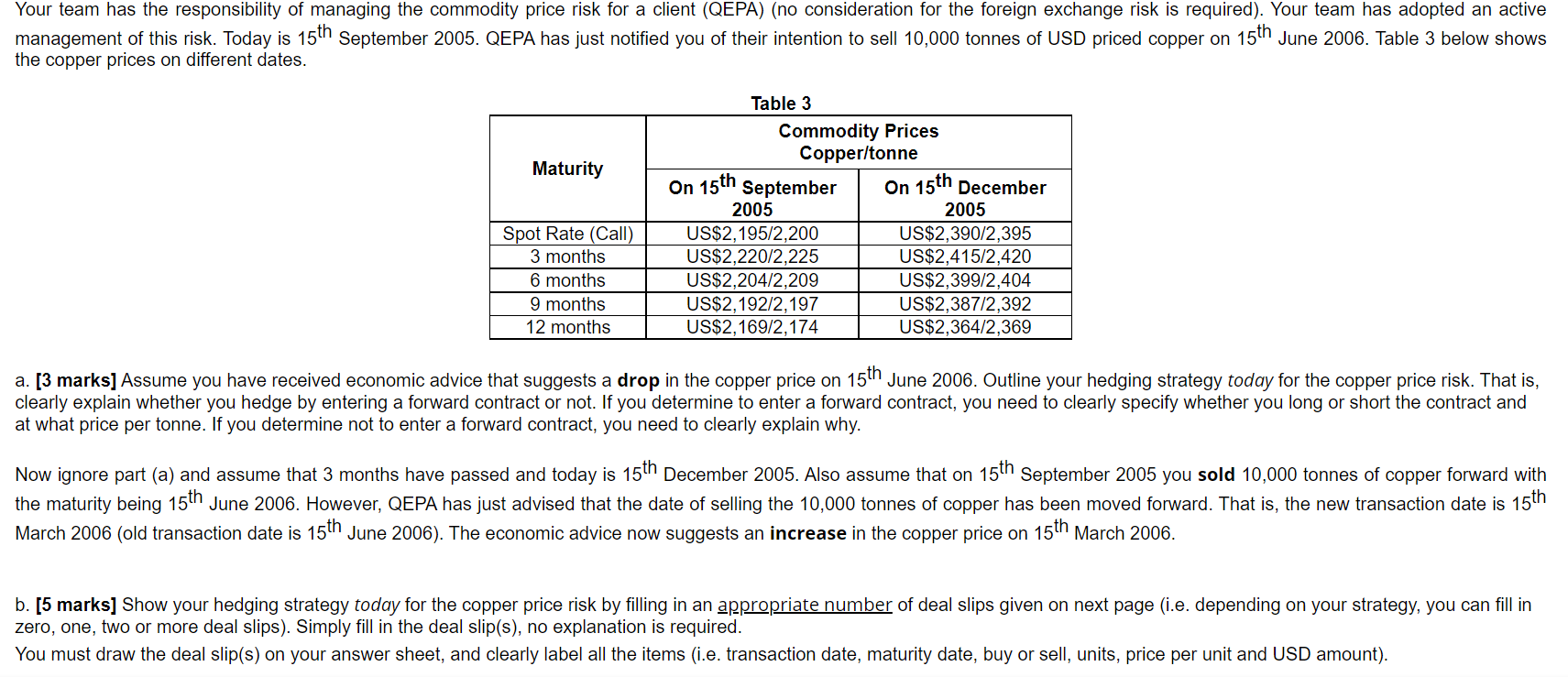

Your team has the responsibility of managing the commodity price risk for a client (QEPA) (no consideration for the foreign exchange risk is required). Your team has adopted an active management of this risk. Today is 15th September 2005. QEPA has just notified you of their intention to sell 10,000 tonnes of USD priced copper on 15th June 2006. Table 3 below shows the copper prices on different dates. Table 3 Maturity Spot Rate (Call) 3 months 6 months 9 months 12 months Commodity Prices Copper/tonne On 15th September On 15th December 2005 2005 US$2,195/2,200 US$2,390/2,395 US$2,220/2,225 US$2,415/2,420 US$2,204/2,209 US$2,399/2,404 US$2,192/2,197 US$2,387/2,392 US$2,169/2,174 US$2,364/2,369 a. [3 marks] Assume you have received economic advice that suggests a drop in the copper price on 15th June 2006. Outline your hedging strategy today for the copper price risk. That is, clearly explain whether you hedge by entering a forward contract or not. If you determine to enter a forward contract, you need to clearly specify whether you long or short the contract and at what price per tonne. If you determine not to enter a forward contract, you need to clearly explain why. Now ignore part (a) and assume that 3 months have passed and today is 15th December 2005. Also assume that on 15th September 2005 you sold 10,000 tonnes of copper forward with the maturity being 15th June 2006. However, QEPA has just advised that the date of selling the 10,000 tonnes of copper has been moved forward. That is, the new transaction date is 15th March 2006 (old transaction date is 15th June 2006). The economic advice now suggests an increase in the copper price on 15th March 2006. b. [5 marks] Show your hedging strategy today for the copper price risk by filling in an appropriate number of deal slips given on next page (i.e. depending on your strategy, you can fill in zero, one, two or more deal slips). Simply fill in the deal slip(s), no explanation is required. You must draw the deal slip(s) on your answer sheet, and clearly label all the items (i.e. transaction date, maturity date, buy or sell, units, price per unit and USD amount). Your team has the responsibility of managing the commodity price risk for a client (QEPA) (no consideration for the foreign exchange risk is required). Your team has adopted an active management of this risk. Today is 15th September 2005. QEPA has just notified you of their intention to sell 10,000 tonnes of USD priced copper on 15th June 2006. Table 3 below shows the copper prices on different dates. Table 3 Maturity Spot Rate (Call) 3 months 6 months 9 months 12 months Commodity Prices Copper/tonne On 15th September On 15th December 2005 2005 US$2,195/2,200 US$2,390/2,395 US$2,220/2,225 US$2,415/2,420 US$2,204/2,209 US$2,399/2,404 US$2,192/2,197 US$2,387/2,392 US$2,169/2,174 US$2,364/2,369 a. [3 marks] Assume you have received economic advice that suggests a drop in the copper price on 15th June 2006. Outline your hedging strategy today for the copper price risk. That is, clearly explain whether you hedge by entering a forward contract or not. If you determine to enter a forward contract, you need to clearly specify whether you long or short the contract and at what price per tonne. If you determine not to enter a forward contract, you need to clearly explain why. Now ignore part (a) and assume that 3 months have passed and today is 15th December 2005. Also assume that on 15th September 2005 you sold 10,000 tonnes of copper forward with the maturity being 15th June 2006. However, QEPA has just advised that the date of selling the 10,000 tonnes of copper has been moved forward. That is, the new transaction date is 15th March 2006 (old transaction date is 15th June 2006). The economic advice now suggests an increase in the copper price on 15th March 2006. b. [5 marks] Show your hedging strategy today for the copper price risk by filling in an appropriate number of deal slips given on next page (i.e. depending on your strategy, you can fill in zero, one, two or more deal slips). Simply fill in the deal slip(s), no explanation is required. You must draw the deal slip(s) on your answer sheet, and clearly label all the items (i.e. transaction date, maturity date, buy or sell, units, price per unit and USD amount)