Answered step by step

Verified Expert Solution

Question

1 Approved Answer

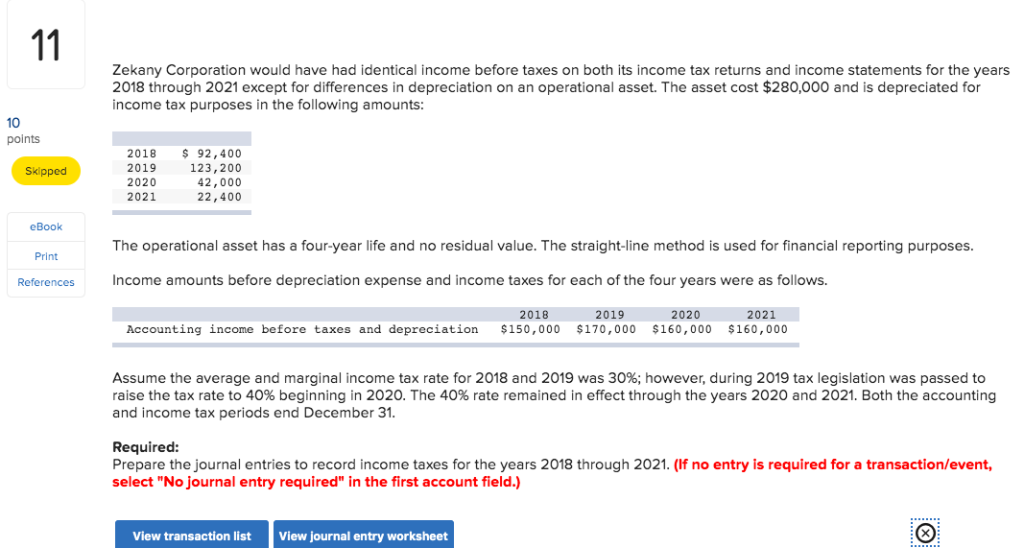

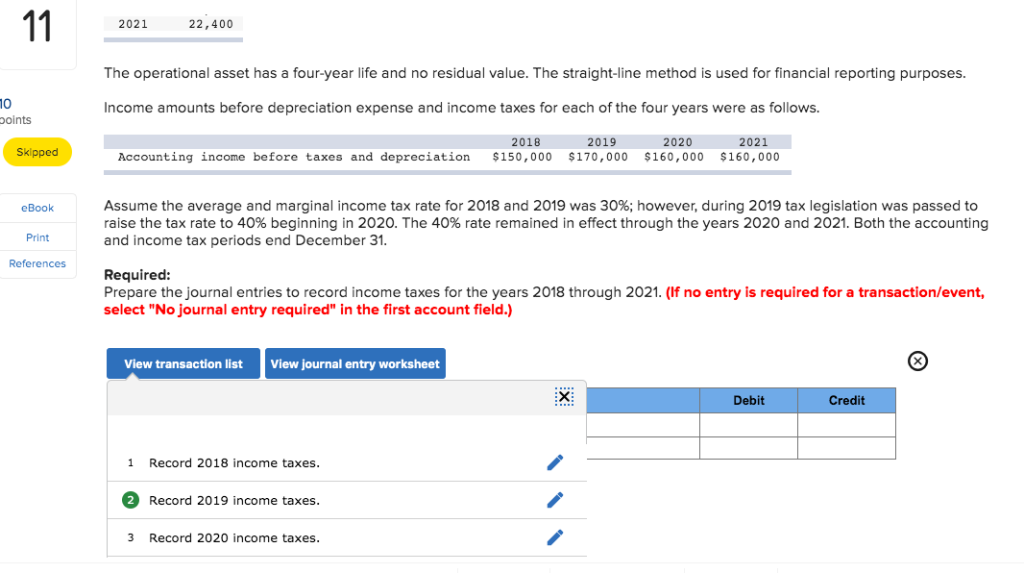

Zekany Corporation would have had identical income before taxes on both its income tax returns and income statements for the years 2018 through 2021 except

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting 101 An Investment In Knowledge Pays The Best Interest Benjamin Franklin

Authors: Daniel Arellano

1st Edition

979-8633540260