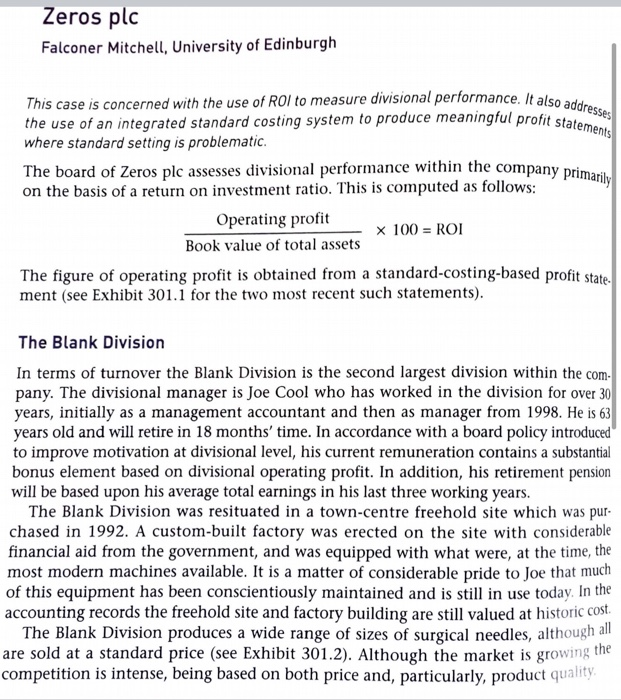

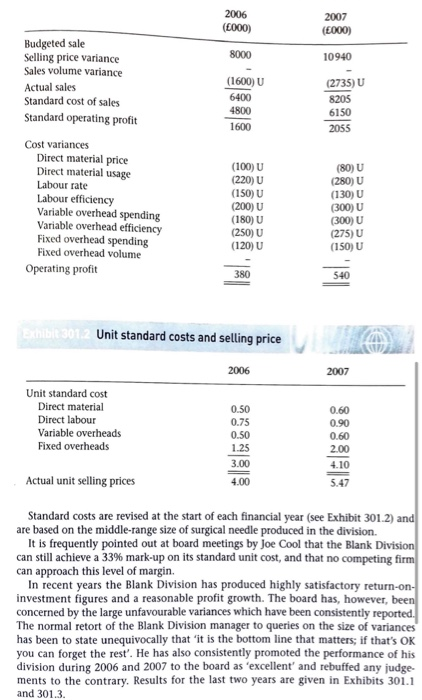

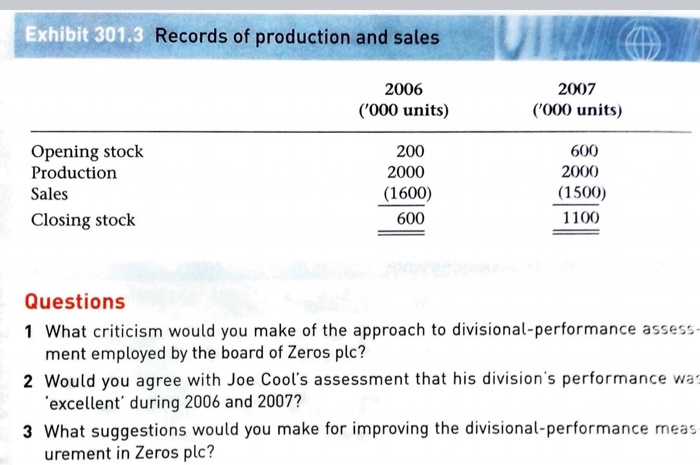

Zeros plc Falconer Mitchell, University of Edinburgh e It also addresses This case is concerned with the use of ROI to measure divisional performance. It also add the use of an integrated standard costing system to produce meaningful profit stars where standard setting is problematic. The board of Zeros plc assesses divisional performance within the company on the basis of a return on investment ratio. This is computed as follows: Operating profit - 1 100 = ROI Book value of total assets The figure of operating profit is obtained from a standard-costing-based profit state. ment (see Exhibit 301.1 for the two most recent such statements). The Blank Division In terms of turnover the Blank Division is the second largest division within the com. pany. The divisional manager is Joe Cool who has worked in the division for over 30 years, initially as a management accountant and then as manager from 1998. He is 63 years old and will retire in 18 months' time. In accordance with a board policy introduced to improve motivation at divisional level, his current remuneration contains a substantial bonus element based on divisional operating profit. In addition, his retirement pension will be based upon his average total earnings in his last three working years. The Blank Division was resituated in a town-centre freehold site which was pur- chased in 1992. A custom-built factory was erected on the site with considerable financial aid from the government, and was equipped with what were, at the time, the most modern machines available. It is a matter of considerable pride to Joe that much of this equipment has been conscientiously maintained and is still in use today. In the accounting records the freehold site and factory building are still valued at historic cost. The Blank Division produces a wide range of sizes of surgical needles, although all are sold at a standard price (see Exhibit 301.2). Although the market is growing competition is intense, being based on both price and, particularly, product quality 2006 (5000) 2007 (2000) 8000 10940 Budgeted sale Selling price variance Sales volume variance Actual sales Standard cost of sales Standard operating profit (1600) U 6400 4800 (2735) U 8205 6150 2055 1600 Cost variances Direct material price Direct material usage Labour rate Labour efficiency Variable overhead spending Variable overhead efficiency Fixed overhead spending Fixed overhead volume Operating profit (100) U (220) U (150) U (200) U (180) U (250) U (120) U (80) U (280) U (130) U (300) U (300) U (275) U (150) U 380 540 ER 301 Unit standard costs and selling price 2006 2007 0.50 Unit standard cost Direct material Direct labour Variable overheads Fixed overheads 0.60 0.90 0.60 2.00 0.50 1.25 3.00 4.00 Actual unit selling prices Standard costs are revised at the start of each financial year (see Exhibit 301.2) and are based on the middle-range size of surgical needle produced in the division. It is frequently pointed out at board meetings by Joe Cool that the Blank Division can still achieve a 33% mark-up on its standard unit cost, and that no competing firm can approach this level of margin. In recent years the Blank Division has produced highly satisfactory return-on- investment figures and a reasonable profit growth. The board has, however, been concerned by the large unfavourable variances which have been consistently reported. The normal retort of the Blank Division manager to queries on the size of variances has been to state unequivocally that it is the bottom line that matters: if that's OK you can forget the rest'. He has also consistently promoted the performance of his division during 2006 and 2007 to the board as 'excellent and rebuffed any judge- ments to the contrary. Results for the last two years are given in Exhibits 301.1 and 301.3. Exhibit 301.3 Records of production and sales 2006 ('000 units) 2007 ('000 units) Opening stock Production Sales Closing stock 200 2000 (1600) 600 2000 (1500) 600 1100 Questions 1 What criticism would you make of the approach to divisional-performance assess- ment employed by the board of Zeros plc? 2 Would you agree with Joe Cool's assessment that his division's performance was 'excellent' during 2006 and 2007? 3 What suggestions would you make for improving the divisional performance meas urement in Zeros plc