Answered step by step

Verified Expert Solution

Question

1 Approved Answer

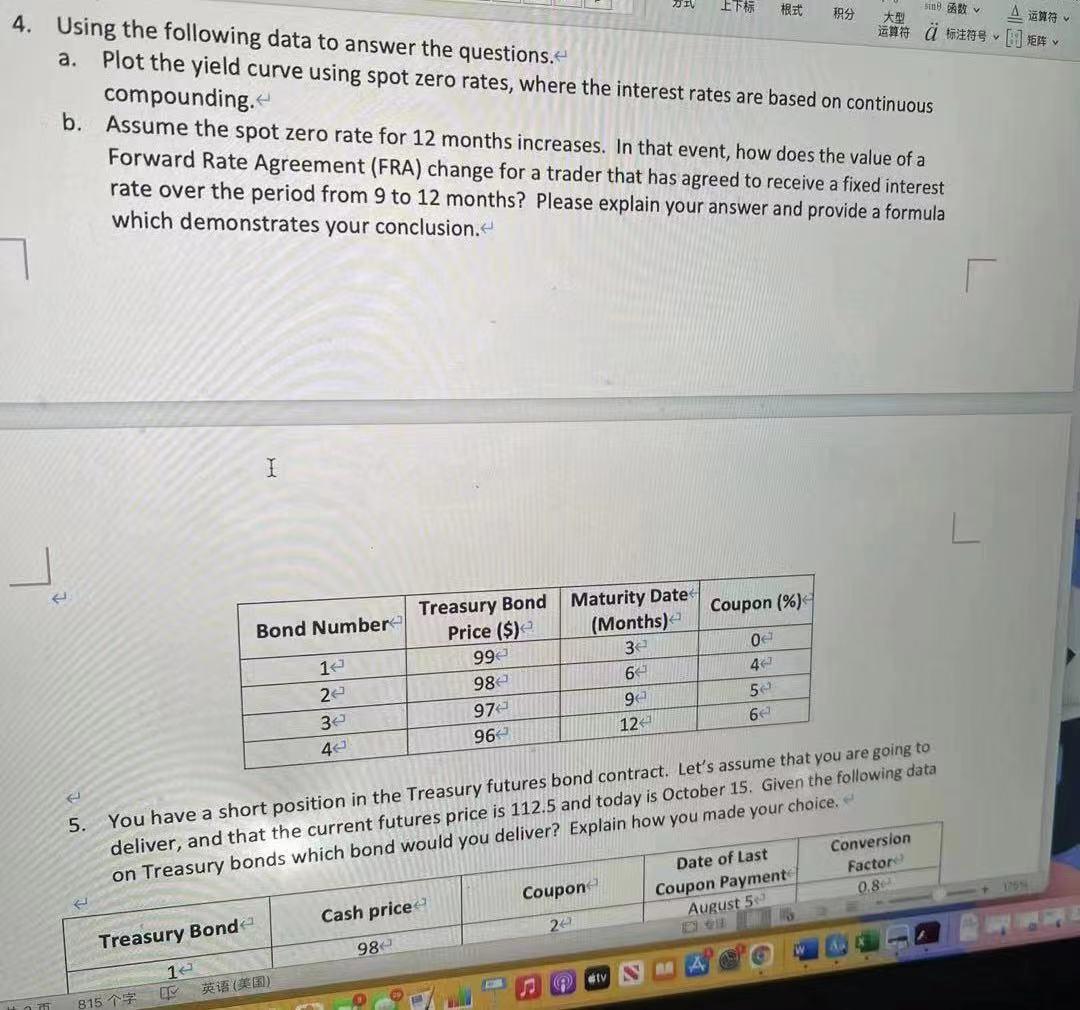

ZIV ETI 199 3129 1. y d y 4. Using the following data to answer the questions. a. Plot the yield curve using spot zero

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Information Technology And Insights Audit Controls Bringing A Vision And Understanding To Effective Practices

Authors: R. Allen Conner

1st Edition

1720081883, 978-1720081883