In 2015, Gail changed from the lower of cost or market FIFO method to the LIFO inventory

Question:

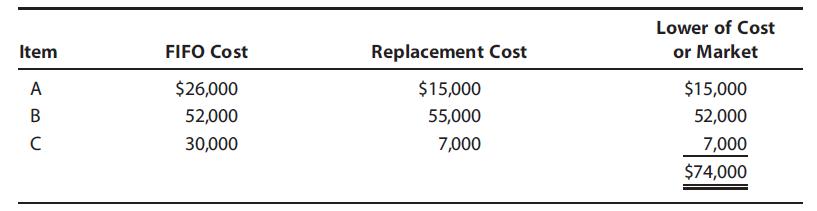

In 2015, Gail changed from the lower of cost or market FIFO method to the LIFO inventory method. The ending inventory for 2014 was computed as follows:

Item C was damaged goods, and the replacement cost used was actually the estimated selling price of the goods. The actual cost to replace item C was $32,000.

a. What is the correct beginning inventory for 2015 under the LIFO method?

b. What immediate tax consequences (if any) will result from the switch to LIFO?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a The correct beginning ...View the full answer

Answered By

Chandrasekhar Karri

I have tutored students in accounting at the high school and college levels. I have developed strong teaching methods, which allow me to effectively explain complex accounting concepts to students. Additionally, I am committed to helping students reach their academic goals and providing them with the necessary tools to succeed.

0 Reviews

10+ Question Solved

Related Book For

South Western Federal Taxation 2016 Individual Income Taxes

ISBN: 9781305393301

39th Edition

Authors: James H. Boyd, William H. Jr. Hoffman, David M. Maloney, William A. Raabe, James C. Young

Question Posted: