Answered step by step

Verified Expert Solution

Question

1 Approved Answer

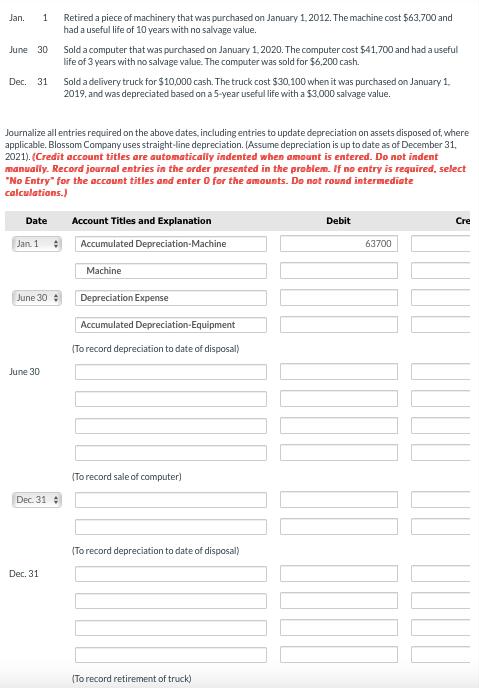

Jan. 1 June 30 Dec. 31 Date Jan 1 Journalize all entries required on the above dates, including entries to update depreciation on assets

Jan. 1 June 30 Dec. 31 Date Jan 1 Journalize all entries required on the above dates, including entries to update depreciation on assets disposed of, where applicable. Blossom Company uses straight-line depreciation. (Assume depreciation is up to date as of December 31, 2021). (Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Do not round intermediate calculations.) June 30 June 30 Dec. 31 Retired a piece of machinery that was purchased on January 1, 2012. The machine cost $63,700 and had a useful life of 10 years with no salvage value. Dec. 31 Sold a computer that was purchased on January 1, 2020. The computer cost $41,700 and had a useful life of 3 years with no salvage value. The computer was sold for $6.200 cash. Sold a delivery truck for $10,000 cash. The truck cost $30,100 when it was purchased on January 1, 2019, and was depreciated based on a 5-year useful life with a $3,000 salvage value. Account Titles and Explanation Accumulated Depreciation-Machine Machine Depreciation Expense Accumulated Depreciation-Equipment (To record depreciation to date of disposal) (To record sale of computer) (To record depreciation to date of disposal) (To record retirement of truck) Debit 63700 Cre

Step by Step Solution

★★★★★

3.32 Rating (146 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Accounting Reporting Analysis And Decision Making

Authors: Shirley Carlon, Rosina Mladenovic Mcalpine, Chrisann Palm, Lorena Mitrione, Ngaire Kirk, Lily Wong

5th Edition

0730313743, 978-0730313748