Crescent Chemical and Pharmaceuticals Ltd is one of the oldest and pioneering drug manufacturing companies in Calcutta.

Question:

Crescent Chemical and Pharmaceuticals Ltd is one of the oldest and pioneering drug manufacturing companies in Calcutta. It has gained a high reputation because many of its patented drugs and pharmaceutical products are distributed through a wide network of sales outlets across the country. It was obliged to make a serious effort to reduce total product cost due to the increase in competition, both from small and large-scale manufacturers. However, this seemed impossible immediately due to the steep and steady rise in the prices of heavy and basic chemicals and other raw materials. The company management then decided to analyse the requirements of the second-largest group of items in the purchase budget, i.e. packing materials.

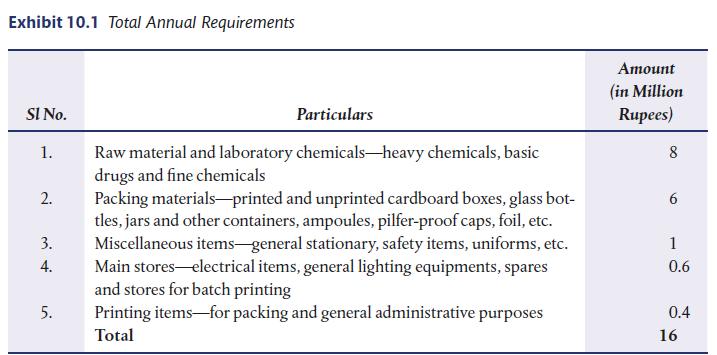

The group-wise annual purchase requirements of the company is given in Exhibit 10.1.

It was seen that out of the total annual requirements of stores of Rs 16 million, the packing material accounted for two-thirds of the money value of raw materials and laboratory chemicals. Therefore, even a slight reduction in the cost of these items was seen to be able to yield a large sum of savings, which would be available for deployment in other spheres of activities of the company. However, the preservative and protective characteristics of packing materials could not be sacrificed.

Several senior officials were grouped to form a value analysis team in order to explore the possibilities of cost reductions and make recommendations to control costs. The chief chemist, designer, chiefs of purchases, stores and packing departments as well as costs and works accountants, works manager and marketing manager were clubbed together to present their respective view points.

A broad analysis revealed that the packing costs had soared in recent years due to the heavy breakage of glass bottles, jars and other containers. This was attributed to a large extent to improper handling and the brittleness of glass. In an effort to substitute, the chief chemist isolated at least 15 items on the product line for which glass bottles and container neither enhanced any functional utility, nor acted as preservatives.

A detailed probe revealed that in many cases, container design and shape could be conveniently changed to standard sizes and shapes. A switchover scheme for these container items from glass to moulded plastics with caps (with polythene packs inside for pilfer proofing)

was considered. It was worked out that about three per cent of net savings of the total packing costs could be affected as this would reduce breakages substantially.

A report from the packing department showed that it required extra hands for this item wise conversion for filling.

The marketing manager, however, objected to the plan on the ground that such a sudden switchover would create some marketing problems. This had to be heavily advertised and brought to the notice of the ultimate consumers, who had been accustomed to the company’s product being available in traditional packs. Since the company name was etched on each

glass bottle, container, etc. he apprehended a shift of custom to other companies’ products with unscrupulous traders taking advantage of these situations.

Mr Sarkar, the purchase manager, however, did not agree and argued that the company’s name could be printed and moulded on plastic packs. The marketing manager was then approached with drawings of attractive designs and colours for various container shapes.

After going through the drawings, he withdrew his initial objections satisfied that the proposal of substitution was both technically sound and economically feasible.

All that was done was a cost comparison of various cost components from functional utilities as well as the cost of acquisition, carrying and handling before and after substitution.

The overall sales turnover at the end of financial year actually increased in spite of the gloomy projections of sales by the marketing manager. This increased sales turnover fully justified the additional expenditure on sales promotion activities.

Question For Discussion

1. Was the initial objection of the marketing manager valid? Do you agree with his views?

2. At the end of the year, the marketing manager contended that target sales were achieved through vigorous sales promotion activities and he had been requesting for an increase in the budget for sales promotion all along. Do you agree with the same?

3. Prepare a report on value analysis based on the data given in the case study.

Step by Step Answer:

The image provided lists the total annual requirements of Crescent Chemical and Pharmaceuticals Ltd in terms of the amount spent on different categories of items The figures are as follows 1 Raw mater...View the full answer