(Evaluating and interpreting the effects of a write-down, LO 4, 6) Meridian Ltd. (ML) is a public...

Question:

(Evaluating and interpreting the effects of a write-down, LO 4, 6) Meridian Ltd.

(ML) is a public company that manufactures machine parts. In its most recent financial statements ML wrote down $175,000,000 of its assets. The assets will continue to be used by ML, The new president and CEO of ML announced that the write-downs were the result of competitive pressures and poor performance of the company in the last year. The write-downs were reported separately in ML’s income statement as a “non-recurring” item. A non-recurring item is “an item that results from transactions or events that are not expected to occur frequently over several years, or do not typify normal business activities of the entity.” The write-off is not included in the calculation of operating income.

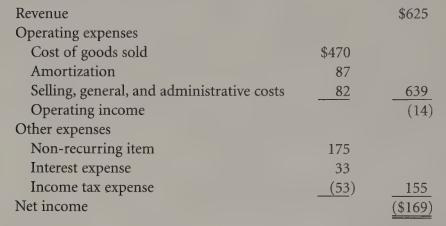

ML’s summarized income statement for the year ended December 31, 2004 is

(amounts in millions of dollars):

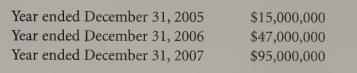

The write-downs will reduce the amortization expense by $22,000,000 per year for each of the next eight years. After the announcement and release of the income statement, analysts revised their forecasts of earnings for the next three years to:

Required:

a. What would net income be in each of 2004 through 2007 had ML not written off the assets and continued to amortize them? Assume that the operations of ML do not change regardless of the accounting method used.

b. Why do you think management might have undertaken the decision to write off the assets?

c. As an investor trying to evaluate the performance and predict future profitability, what problems do asset write-downs of this type create for you? Consider how the write-off is reflected in the income statement and use the ML case as a basis for your discussion.

Step by Step Answer: