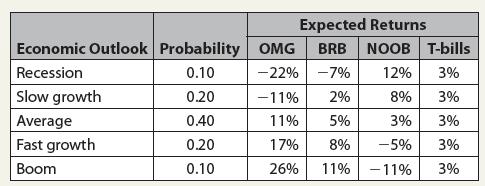

You are considering investing in the following securities and have developed the probability distributions for their returns

Question:

You are considering investing in the following securities and have developed the probability distributions for their returns over the next year.

a. Calculate the expected return and standard deviation of each security.

b. Create a variance/covariance matrix for the four securities. An example of how to create a formula that uses probabilities instead of historical (equally weighted) data.

c. Using the Solver, create a set of 11 portfolios that make up the capital market line. Create a chart of the CML from your results, and add a plot of the original securities.

d. Find the weights of each security in the market portfolio by maximizing the Sharpe ratio.

e. How does the risk/return trade-off of the original securities compare to that available on the CML?

Step by Step Answer:

ANSWER To calculate the expected return and standard deviation of each security well use the provided probability distributions Lets start with the ca...View the full answer