Refer to P6.7 . Assume that the presentation currency of Y Co is the FC while the

Question:

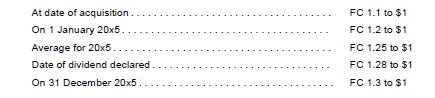

Refer to P6.7 . Assume that the presentation currency of Y Co is the FC while the functional currency is the dollar ($). P Co’s investment in Y Co is FC 1,980,000. The exchange rates are as follows:

Foreign currency translation reserve (FCTR) on 1 January 20x5 arising from the translation of net assets of Y Co (excluding the FCTR relating to goodwill and fair value adjustments) is FC 150,000 (credit balance).

Required

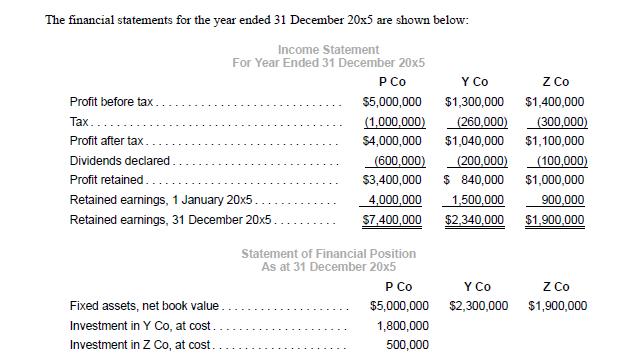

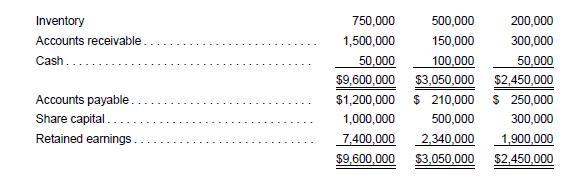

1. Translate the financial statements of subsidiary Y Co for the year ended 31 December 20x5 into the presentation currency. Perform a reconciliation check on the movement in FCTR.

2. Prepare the consolidation adjusting entries for the year ended 31 December 20x5 in FC to:

(a) Eliminate the investment in Y Co and allocate the cost of business combination;

(b) Recognize the FCTR on goodwill and intangible asset.

(c) Allocate FCTR to non-controlling interests.

Data from P6.7

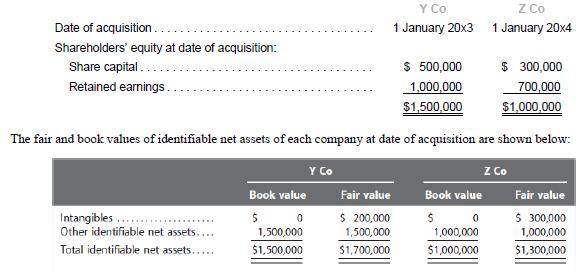

On 1 January 20x3, P Co acquired a 90% interest in Y Co. On that date, the fair value of non-controlling interests in Y Co was $180,000. A year later, on 1 January 20x4, P Co acquired a 30% interest in Z Co. Book values of equity and fair values of identifiable net assets of the acquired companies are shown below:

Additional information

(a) Unrecognized intangible asset of Z Co was impaired in 20x5 to the extent of 30% of its original fair value.

Unrecognized intangible asset of Y Co was unimpaired.

(b) On 1 January 20x5, Y Co sold equipment to P Co at an invoiced price of $150,000. At the date of the sale, the net book value of the equipment was $48,000. Its original cost was $120,000. The original useful life of the equipment was five years; it had no estimated residual value. On 1 January 20x5, the remaining useful life was estimated at three years; estimated residual value remains at nil value.

(c) P Co sold inventory to Y Co in December 20x4 at market price of $60,000. The original cost of the inventory was $70,000. The inventory was resold to third parties in 20x5.

(d) Assume a tax rate of 20%. Recognize tax on fair value adjustments.

Step by Step Answer:

To address the questions outlined we need to perform currency translations and reconciliation of the Foreign Currency Translation Reserve FCTR as well as prepare consolidation adjusting entries based ...View the full answer

Advanced Financial Accounting An IFRS Standards Approach

ISBN: 9781285428765

4th Edition

Authors: Pearl Tan, Chu Yeong Lim, Ee Wen Kuah