In 1887, a young Dutchman, Albert Heijn, entered the business world by purchasing a small grocery store

Question:

In 1887, a young Dutchman, Albert Heijn, entered the business world by purchasing a small grocery store from his father.1 The store was located in Oostzaan, a village on the Dutch peninsula known as North Holland, which is also one of the Netherlands’ 12 provinces. Unlike his father who was content to own and operate a small business, Albert had dreams of becoming an entrepreneur on a much larger scale. Within 10 years, the frugal and hard-working Heijn owned two dozen grocery stores scattered throughout the small country. A key to the early success of Heijn’s retail grocery chain was that he designed each of his new stores to meet the specific interests and needs of the community in which it was located. For example, the merchandise stocked by Heijn stores in fishing villages was quite different from the merchandise carried by stores located in farming communities. In metropolitan areas such as Amsterdam and The Hague, Heijn established large stores that stocked a complete range of food products and household merchandise. In fact, Heijn’s company was credited with developing the supermarket concept in the Netherlands; in later years, his company popularized the convenience-store format in his home country.

In the early 1900s, Heijn launched his own brand of baked products including cookies and assorted pastries that he sold in his grocery stores. Over the years to come, the company would develop a wide range of its own products that it marketed under the Albert Heijn brand. In 1973, management changed the company’s name to Ahold. The following decade, Queen Beatrix awarded the title “Royal” to the company, a designation reserved for Dutch companies that have operated continuously—and honorably—for one hundred years.2 By the early 1990s, Royal Ahold ranked among the most prominent and respected corporations in the Netherlands. For several years during that time frame, Royal Ahold was named the most desirable employer in the Netherlands and the company with the best reputation in that nation.3 The company was also well known outside of its home country. In 1948, the Heijn family had taken the company public. By 2000, the company’s stock was registered on stock exchanges around the world, including the New York Stock Exchange.

A financial scandal shortly after the turn of the century besmirched Royal Ahold’s sterling reputation, prompted a consumer boycott of the company in the Netherlands, and resulted in many critics insisting that the Dutch royal family rescind the company’s “royal” designation. In March 2003, The Economist, one of Europe’s leading business publications, referred to the Royal Ahold scandal as “Europe’s Enron.”4 The Royal Ahold scandal, along with the accounting fraud at the giant Italian firm Parmalat, caused the European Union (EU) to impose more extensive regulation on the financial reporting system and independent audit function within its member nations. The Royal Ahold debacle also focused more attention on the question of whether uniform accounting and auditing standards should be adopted around the globe......

Questions

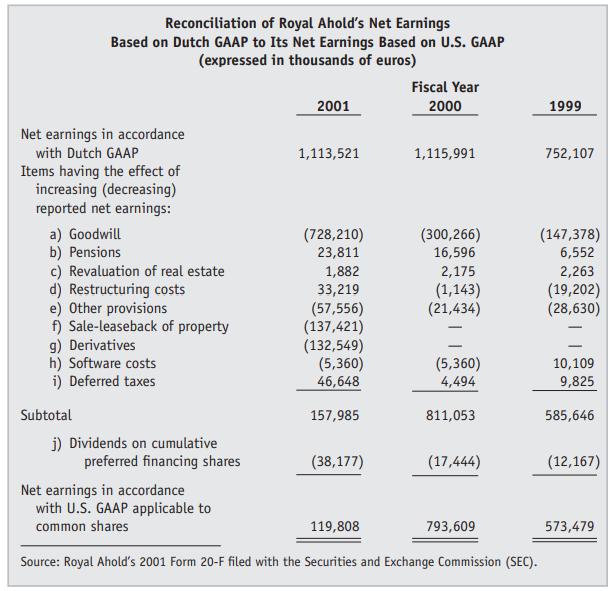

1. To arrive at the U.S. GAAP-based net income figures shown in Exhibit 3, Royal Ahold fully consolidated the operating results of the companies in which it held a 50 percent equity interest. For purposes of determining its U.S. GAAP-based net income figures, what accounting method should the company have applied to those investments? How would the application of this latter method have affected the U.S. GAAP-based net income amounts?

2. The application of Dutch GAAP and U.S. GAAP to Royal Ahold’s financial data produced significantly different net earnings figures for the company each year. Explain what is meant by “earnings quality.” Suppose that the application of IFRS to a company’s financial data produces a higher net income for that company than the application of U.S. GAAP. Does this mean that the U.S. GAAP-based net income figure is of “higher quality” than the net income figure yielded by IFRS? Explain.

3. Accounting for promotional allowances in the retailing and wholesaling industries has long been a controversial topic. In 2002, the Emerging Issues Task Force (EITF) of the Financial Accounting Standards Board began studying that issue. What changes, if any, did the EITF make in the recommended accounting for such promotional allowances?

4. Identify the factors that complicate an independent audit of a multinational company. Explain how these factors affected the audits of Royal Ahold that were performed by Deloitte Accountants, B.V., and its affiliated fi rms.

5. Briefly describe the three elements of the “fraud triangle.” Identify specific fraud risk factors that were present during the audits of Royal Ahold that were performed by Deloitte Accountants. How should those risk factors have affected Deloitte’s audits?

6. What audit procedures would likely have been the most effective for detecting the fraudulent accounting for U.S. Foodservice’s promotional allowances?

7. Royal Ahold’s two major business segments were food wholesaling and retail grocery chains. Identify and briefly explain three key differences in the overall design of an audit for those two types of business segments.

Exhibit 3

Step by Step Answer:

Contemporary Auditing Real Issues And Cases

ISBN: 9780538466790

8th Edition

Authors: Michael C. Knapp