Automotive Products (AP) designs and produces automotive parts. In 2014, actual variable manufacturing overhead is $308,600. APs

Question:

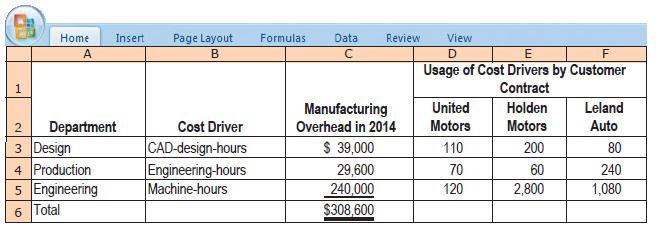

Automotive Products (AP) designs and produces automotive parts. In 2014, actual variable manufacturing overhead is $308,600. AP’s simple costing system allocates variable manufacturing overhead to its three customers based on machine-hours and prices its contracts based on full costs. One of its customers has regularly complained of being charged noncompetitive prices, so AP’s controller Devon Smith realizes that it is time to examine the consumption of overhead resources more closely. He knows that there are three main departments that consume overhead resources: design, production, and engineering. Interviews with the department personnel and examination of time records yield the following detailed information.

Required:

1. Compute the manufacturing overhead allocated to each customer in 2014 using the simple costing system that uses machine-hours as the allocation base.

2. Compute the manufacturing overhead allocated to each customer in 2014 using department-based manufacturing overhead rates.

3. Comment on your answers in requirements 1 and 2. Which customer do you think was complaining about being overcharged in the simple system? If the new department-based rates are used to price contracts, which customer(s) will be unhappy? How would you respond to these concerns?

4. How else might AP use the information available from its department-by-department analysis of manufacturing overhead costs?

5. AP’s managers are wondering if they should further refine the department-by-department costing system into an ABC system by identifying different activities within each department. Under what conditions would it not be worthwhile to further refine the department costing system into an ABC system?

Step by Step Answer:

In order to address the requirements well need to perform calculations using the provided table Lets work through each requirement one by one 1 Compute the manufacturing overhead allocated to each cus...View the full answer

Cost Accounting A Managerial Emphasis

ISBN: 978-0133428704

15th edition

Authors: Charles T. Horngren, Srikant M. Datar, Madhav V. Rajan