(Comprehensive: CMA adopted) The financial results for the Continuing Education Department of BusEd Corporation for November 19x8...

Question:

(Comprehensive: CMA adopted) The financial results for the Continuing Education Department of BusEd Corporation for November 19x8 are presented at the top of the next page Mary Ross, president of BusEd, is pleased with the final results but has observed that the revenue and most of the costs and expenses of this department exceeded the budgeted amounts. Barry Stein, vice president of the Continuing Education Department, has been requested to provide an explanation of any amount that exceeded the budget by 5 percent or more. , ^ k, i.

Stein has accumulated the following facts to assist in his analysis of the November results.

1 The budget for calendar year 1 9x8 was finalized in December 1 9x7, and at that time, a full program of continuing education courses was scheduled to be held in Chicago during the first weeic of November 19x8. The courses were scheduled so that eight courses would be run on each of the five days during the week. The budget assumed that there would be 425 participants in the program and 1 ,000 participant days for the week.

2 BusEd charges a flat fee of $150 per day of course instruction, i.e., the fee for a three-day course would be $450. BusEd grants a 10 percent discount to persons who subscribe to its publications. The 10 percent discount is also granted to second and subsequent registrants for the same course from the same organization. However, only one discount per registration is allowed. Historically, 70 percent of the participant day registrations are at the full fee of $150 per day and 30 percent of the participant day registrations receive the discounted fee of $135 per day. These percentages were used in developing the November 19x8 budgeted revenue.

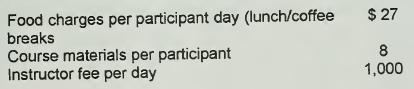

3. The following estimates were used to develop the budgeted figures for course related expenses.

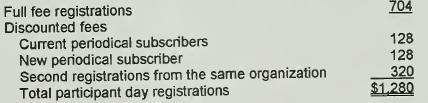

4 A total of 530 individuals participated in the Chicago courses in November 19x8, accounting for 1,280 participant days. This included 20 persons who took a new, twoday course on pension accounting that was not on the original schedule; thus, on two of the days, nine courses were offered, and an additional instructor was hired to cover the new course. The breakdown of the course registrations was as follows.

5. A combined promotional mailing was used to advertise the Chicago program and a program in Cincinnati that was scheduled for December 1988. The incremental costs of the combined promotional piece was $5,000, but none of the promotional expenses ($20,000) budgeted for the Cincinnati program in December will have to be incurred. This earlier than nomrial promotion for the Cincinnati program has resulted in early registration fees collected in November as follows (in terms of participant days).

6. BusEd continually updates and adds new courses, and includes $2,000 in each monthly budget for this purpose. The additional amount spent on course development during November was for an unscheduled course that will be offered in February for the first time.

Barry Stein has prepared the quantitative analysis of the November 19x8 variances shown at the bottom of the next page.

REQUIRED:

After reviewing Barry Stein's quantitative analysis of the November variances, prepare a memorandum addressed to Mary Ross explaining the following.

1 .

The cause of the revenue mix variance.

2. The implication of the revenue mix variance.

3. The cause of the revenue timing difference.

4. The significance of the revenue timing difference.

5. The primary cause of the unfavorable total expense variance.

6. How the favorable food price variance was determined.

7. The impact of the promotion timing difference on future revenues and expenses.

8. Whether or not the course development variance has an unfavorable impact on the company.

Step by Step Answer:

Cost Management A Strategic Emphasis

ISBN: 9780070059160

1st Edition

Authors: Edward Blocher, Kung Chen, Thomas Lin