In practice, bond prices are never available at conveniently spaced intervals. Some interpolation scheme is called for.

Question:

In practice, bond prices are never available at conveniently spaced intervals. Some interpolation scheme is called for. However, by making an assumption of constant forward rates between non-standard maturities, we can develop a spot rate curve even for unequal time intervals. In this question, you will undertake a simple exercise of this type.

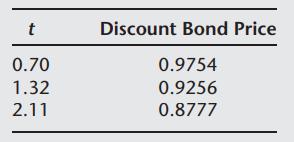

You are given the following discount bond prices at times t:

All compounding and discounting are continuous.

(a) Assuming that forward rates are constant between these dates, find these forward rates.

(b) Price a two-year $100 face value bond that pays 10% p.a. semiannually.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Let the constant forward rate between two dates t and to be denoted as ft t We ...View the full answer

Answered By

Gabriela Rosalía Castro

I have worked with very different types of students, from little kids to bussines men and women. I have thaught at universities, schools, but mostly in private sessions for specialized purpuses. Sometimes I tutored kids that needed help with their classes at school, some others were high school or college students that needed to prepare for an exam to study abroud. Currently I'm teaching bussiness English for people in bussiness positions that want to improve their skills, and preparing and ex-student to pass a standarized test to study in the UK.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: