Time-wise autocorrelated and cross-sectionally heteroskedastic disturbances. Using the Nickell, Nunziata and Ochel (2005) data set which is

Question:

Time-wise autocorrelated and cross-sectionally heteroskedastic disturbances. Using the Nickell, Nunziata and Ochel (2005) data set which is the basis for the empirical example in Sect. 5.3 explaining dynamic unemployment using a panel of 20 OECD countries over the period 1961-95,

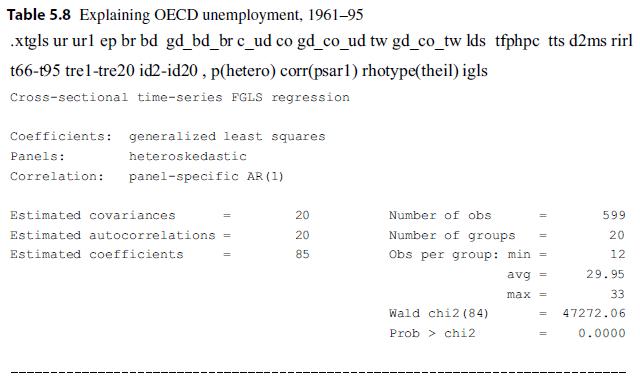

(a) Replicate Table 5.8 using iterative generalized least squares allowing for heteroskedastic errors and country- specific first-order serial correlation.

(b) Replicate the rest of Table 5 in Nickell, Nunziata and Ochel (2005, p. 14).

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Madhvendra Pandey

Hi! I am Madhvendra, and I am your new friend ready to help you in the field of business, accounting, and finance. I am a College graduate in B.Com, and currently pursuing a Chartered Accountancy course (i.e equivalent to CPA in the USA). I have around 3 years of experience in the field of Financial Accounts, finance and, business studies, thereby looking forward to sharing those experiences in such a way that finds suitable solutions to your query.

Thus, please feel free to contact me regarding the same.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: