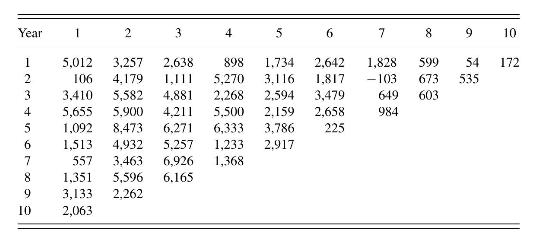

The data in Table 19.5 originate from the 1991 edition of the Historical Loss Development Study, published

Question:

The data in Table 19.5 originate from the 1991 edition of the Historical Loss Development Study, published by the Reinsurance Association of American. These data have been widely used to illustrate triangle methods, beginning with Mack (1994) and later by England and Verrall (2002). These data are from automatic facultative reinsurance business in general liability (excluding asbestos and environmental) coverages. (Under a facultative basis, each risk is underwritten by the reinsurer on its own merits.) Table 19.5 reports incremental incurred losses from 1981-90, in thousands of U.S. dollars.

a. Begin by calculating the deterministic chain-ladder factors. Note the element in the second origin and seventh development year is negative. You may want to first convert the incremental to cumulative payments. Use these factors to complete the triangle.

b. Use your work in part (a) to calculate the reserve estimate.

c. Remove the observation in the second origin and seventh development year. Fit a lognormal model to the remaining data. Comment on the statistical significance of each factor and the goodness of fit.

d. Fit the Hoerl model to the data in part (c). Produce a graph of fitted values.

e. Fit the overdisperse Poisson model to the data in part (c). Check the proximity of the fitted values to the chain-ladder values produced in part (a).

Step by Step Answer:

This question has not been answered yet.

You can Ask your question!

Regression Modeling With Actuarial And Financial Applications

ISBN: 9780521135962

1st Edition

Authors: Edward W. Frees