a. In Concept Check 11.1, you calculated the price and duration of a three-year maturity, 8% coupon

Question:

a. In Concept Check 11.1, you calculated the price and duration of a three-year maturity, 8% coupon bond for an interest rate of 9%. Now suppose the interest rate increases to 9.05%. What is the new value of the bond and the percentage change in the bond’s price?

b. Calculate the percentage change in the bond’s price predicted by the duration formula in Equation 11.2 or 11.3. Compare this value to your answer for (a).![P DX (1 + y] 1+ y (11.2)](https://dsd5zvtm8ll6.cloudfront.net/si.question.images/images/question_images/1697/4/5/7/058652d23a261ee11697457056049.jpg)

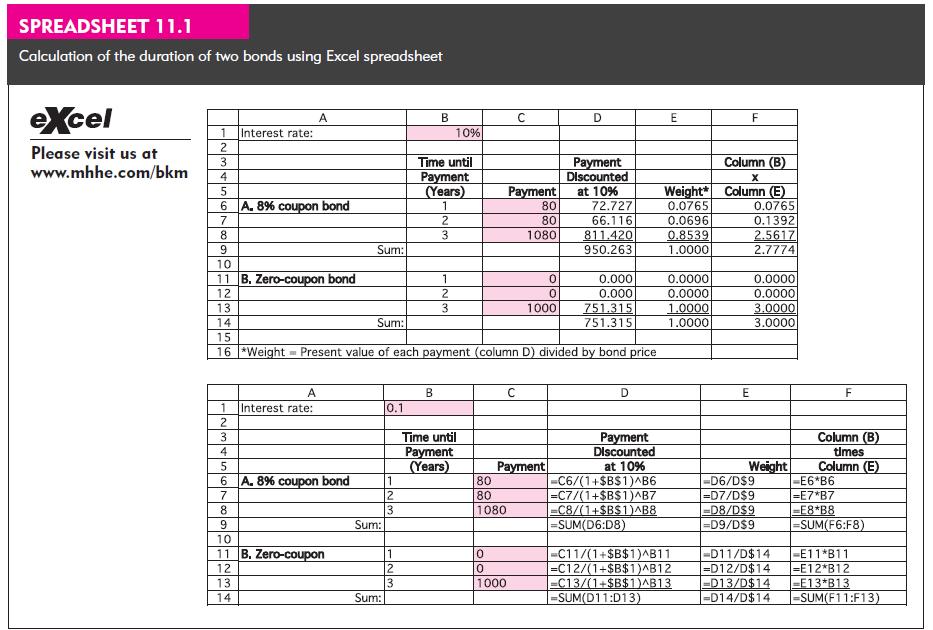

Data from Concept Check 11.1:

Suppose the interest rate decreases to 9%. What will happen to the price and duration of each bond in Spreadsheet 11.1?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a If the interest rate increases from 9 to 905 the bond p...View the full answer

Answered By

Susan Juma

I'm available and reachable 24/7. I have high experience in helping students with their assignments, proposals, and dissertations. Most importantly, I'm a professional accountant and I can handle all kinds of accounting and finance problems.

15+ Reviews

45+ Question Solved

Related Book For

Essentials Of Investments

ISBN: 9780073368719

7th Edition

Authors: Zvi Bodie, Alex Kane, Alan J. Marcus

Question Posted: