Question: We know from the Normal tables that for a standard Normal density, prob (z > 1.96) = 0.025. Because the Normal density is symmetric, we

We know from the Normal tables that for a standard Normal density, prob (z >

1.96) = 0.025. Because the Normal density is symmetric, we can also say that prob (z

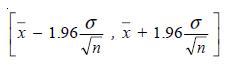

Assume that the distribution of a sample mean x is Normal with mean m and variance s2. Use the standard Normal limits above to claim:

Suppose you could repeatedly draw samples of size n and compute the mean of each such sample. Then 95% of the time, the interval will contain the true mean m. The above interval is said to be a 95% confidence interval for m.

Loosely speaking, once we have computed the sample mean 0 we can be 95%

confident that the true mean will lie between the two limits.

Getting back to our debate with Thomas, let’s look at this another way. We draw a sample of size four, and find a sample mean of 1.1%. We know the population standard deviation is s = 2%.

(i) Find a 95 % confidence limits for the population mean of stock returns.

(ii) Now change the sample size to n = 100. What happens to the confidence limits?

x 1.96- -1.96 x+1.96- n

Step by Step Solution

3.52 Rating (145 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts