New West Company recently hired a new accountant whose first task was to prepare the financial statements

Question:

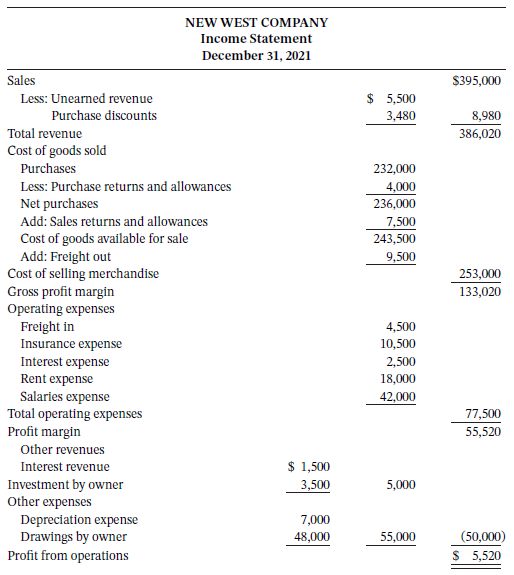

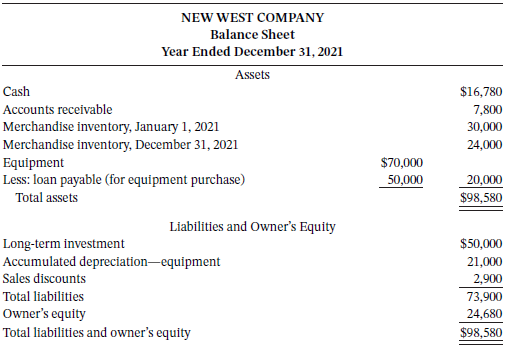

New West Company recently hired a new accountant whose first task was to prepare the financial statements for the year ended December 31, 2021. The following is what he produced:

The owner of the company, Lily Oliver, is confused by the statements and has asked you for your help. She doesn?t understand how, if her Owner?s Capital account was $75,000 at December 31, 2020, owner?s equity is now only $24,680. The accountant tells you that $24,680 must be correct because the balance sheet is balanced. The accountant also tells you that he didn?t prepare a statement of owner?s equity because it is an optional statement. You are relieved to find out that, even though there are errors in the statements, the amounts used from the accounts in the general ledger are the correct amounts.

InstructionsPrepare the correct multiple-step income statement, statement of owner?s equity, and classified balance sheet. You determine that $5,000 of the loan payable on the equipment must be paid during 2022.?

If a company uses a periodic inventory system, does it have to show on its income statement all of the details as to how cost of goods sold was calculated? Why or why not?

Financial StatementsFinancial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial...

Step by Step Answer:

NEW WEST COMPANY Statement of Owners Equity Year Ended December 31 2021 L Oliver capital January 1 2...View the full answer

Accounting Principles Volume 1

ISBN: 978-1119502425

8th Canadian Edition

Authors: Jerry J. Weygandt, Donald E. Kieso, Paul D. Kimmel, Barbara Trenholm, Valerie Warren, Lori Novak