Assume that the tracking error of portfolio X in Problem 3 is 9.2 percent. What is the

Question:

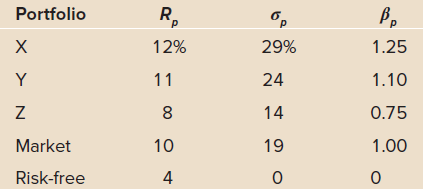

Data From Problem 3

You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: What are the Sharpe ratio, Treynor ratio, and Jensen€™s alpha for each portfolio?

What are the Sharpe ratio, Treynor ratio, and Jensen€™s alpha for each portfolio?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

IR ...View the full answer

Answered By

Zablon Gicharu

I am an educator who possesses the requisite skills and knowledge due to interacting with students for an extended period. I provide solutions to various problems in step-by-step explanations, a well-thought approach and an understandable breakdown. My goal is to impart more straightforward methodologies and understanding to students for more remarkable achievements.

4+ Reviews

10+ Question Solved

Related Book For

Fundamentals of Investments, Valuation and Management

ISBN: 978-1259720697

8th edition

Authors: Bradford Jordan, Thomas Miller, Steve Dolvin

Question Posted: