Question:

Every publicly traded company is required to have an annual audit of its financial statements. Independent auditors-accountants from outside the company-examine how a company records transactions and prepares its financial statements. Auditors examine the records that support the financial records of a business to ensure that generally accepted accounting principles are followed. Based on their audit, the auditors issue an opinion that states whether the financial statements "present fairly, in all material respects, the consolidated financial position" of the company. The auditors' opinion gives external users confidence in the financial statement information. With this confidence, individuals and other companies are more likely to enter into business transactions.

Instructions:

Using Appendix B in this textbook, refer to Costco's Report of Registered Public Accounting Firm on page B-5 to answer the following questions.

1. List the four financial statements that were audited by the independent public accounting firm.

2. Identify the fiscal periods examined by the independent public accounting firm.

3. State whether auditing standards require the independent public accounting firm to obtain "total and absolute" assurance that the financial statements are free of material misstatement.

4. State whether the independent public accounting firm examines every business transaction conducted by Costco.

5. Name the independent public accounting firm and which office is responsible for the audit of Costco's financial statements.

Data from page B-5 Appendix B

Transcribed Image Text:

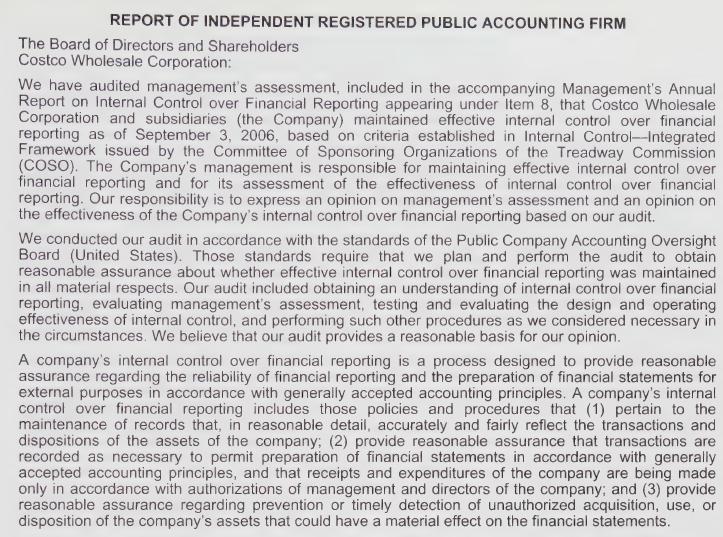

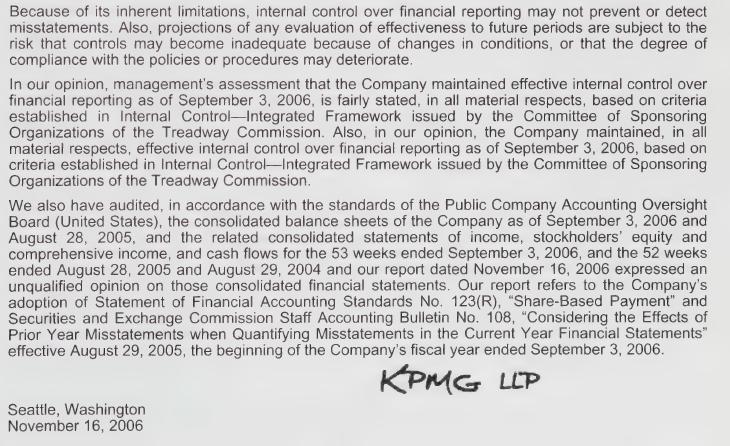

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM The Board of Directors and Shareholders Costco Wholesale Corporation: We have audited management's assessment, included in the accompanying Management's Annual Report on Internal Control over Financial Reporting appearing under Item 8, that Costco Wholesale Corporation and subsidiaries (the Company) maintained effective internal control over financial reporting as of September 3, 2006, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). The Company's management is responsible for maintaining effective internal control over financial reporting and for its assessment of the effectiveness of internal control over financial reporting. Our responsibility is to express an opinion on management's assessment and an opinion on the effectiveness of the Company's internal control over financial reporting based on our audit. We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether effective internal control over financial reporting was maintained in all material respects. Our audit included obtaining an understanding of internal control over financial reporting, evaluating management's assessment, testing and evaluating the design and operating effectiveness of internal control, and performing such other procedures as we considered necessary in the circumstances. We believe that our audit provides a reasonable basis for our opinion. A company's internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. A company's internal control over financial reporting includes those policies and procedures that (1) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the company; (2) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the company are being made only in accordance with authorizations of management and directors of the company; and (3) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company's assets that could have a material effect on the financial statements.