Stewart Manufacturing buys on terms of 2/10, net 30, but it has not been paying on timeit

Question:

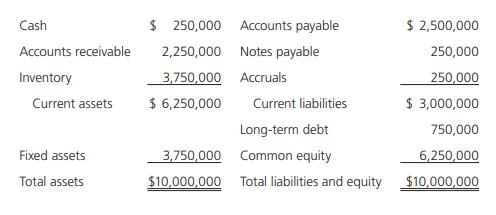

Stewart Manufacturing buys on terms of 2/10, net 30, but it has not been paying on time—it is a “slower payer” and its suppliers are getting upset. Stewart does not take discounts, and it has been paying in 50 rather than the required 30 days. Assume that the accounts payable are recorded at full cost, not net of discounts. Stewart’s suppliers are fed up and will not continue selling to Stewart unless Stewart begins making prompt payments (that is, paying in 30 days or less). The firm is going to have to reduce its level of accounts payable, either to an amount that is equal to 30 days purchases (if it does not take discounts) or to 10 days purchases (if it decides to take discounts). Management has decided to obtain the needed funds by borrowing on an additional 1-year note payable (call this a current liability) from its bank at a rate of 16%, discount interest, with a 15% compensating balance required. The cash currently held by Stewart is needed for transactions, so it cannot be used as part of the compensating balance. So, the issue now facing the company is this: How much trade credit should it use, and how large a loan should it obtain from its bank? Stewart’s balance sheet follows:

Answer the following questions:

a. How large would the accounts payable balance be if Stewart takes discounts? If it does not take discounts and pays in 30 days?

b. How large must the bank loan be if Stewart takes discounts? If Stewart doesn’t take discounts?

c. What are the nominal and effective costs of non free trade credit? What is the effective cost of the bank loan? Based on these costs, what should Stewart do?

d. Assume that Stewart foregoes the discount and borrows the amount needed to become current on its payables. Construct a pro forma balance sheet based on this decision.

e. Using interest rates in the range of 5% to 25% and compensating balances in the range of 0% to 30%, perform a sensitivity analysis that shows how the size of the bank loan would vary with changes in the interest rate and the compensating balance percentage.

Step by Step Answer:

a If Stewart takes discounts the accounts payable balance would be 2500000 12 2450000 If it does not take discounts and pays in 30 days the accounts p...View the full answer

Intermediate Financial Management

ISBN: 9780357516669

14th Edition

Authors: Eugene F Brigham, Phillip R Daves