Hals Heating produces furnaces for commercial buildings. The company applies variable manufacturing overhead at a standard rate

Question:

Hal’s Heating produces furnaces for commercial buildings. The company applies variable manufacturing overhead at a standard rate of \($15\) per direct labor hour. The standard quantity of direct labor is 35 hours per unit. Variable overhead costs totaled \($190,000\) for the month of January. A total of 10,000 direct labor hours were worked during January to produce 320 furnaces.

Required

Calculate the variable overhead spending variance and variable overhead efficiency variance using the format shown in Exhibit 10.5. Clearly label each variance as favorable or unfavorable.

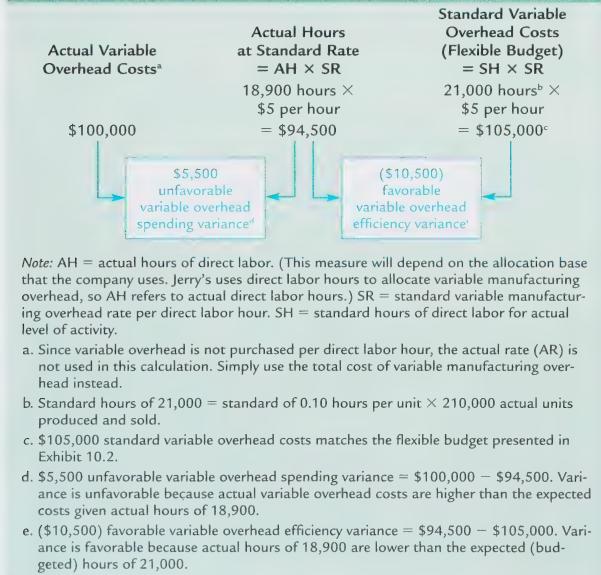

Exhibit 10.5

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Pushpinder Singh

Currently, I am PhD scholar with Indian Statistical problem, working in applied statistics and real life data problems. I have done several projects in Statistics especially Time Series data analysis, Regression Techniques.

I am Master in Statistics from Indian Institute of Technology, Kanpur.

I have been teaching students for various University entrance exams and passing grades in Graduation and Post-Graduation.I have expertise in solving problems in Statistics for more than 2 years now.I am a subject expert in Statistics with Assignmentpedia.com.

3+ Reviews

10+ Question Solved

Related Book For

Question Posted: