Outdoor Products Inc. produces extreme-weather sleeping bags. The company applies variable manufacturing overhead at a standard rate

Question:

Outdoor Products Inc. produces extreme-weather sleeping bags. The company applies variable manufacturing overhead at a standard rate of \($2\) per direct labor hour. The standard quantity of direct labor is 3 hours per unit. Variable overhead costs totaled \($32,000\) for the month of September. A total of 14,700 direct labor hours were worked during September to produce 5,100 sleeping bags.

Required

Calculate the variable overhead spending variance and variable overhead efficiency variance using the format shown in Exhibit 10.5. Clearly label each variance as favorable or unfavorable.

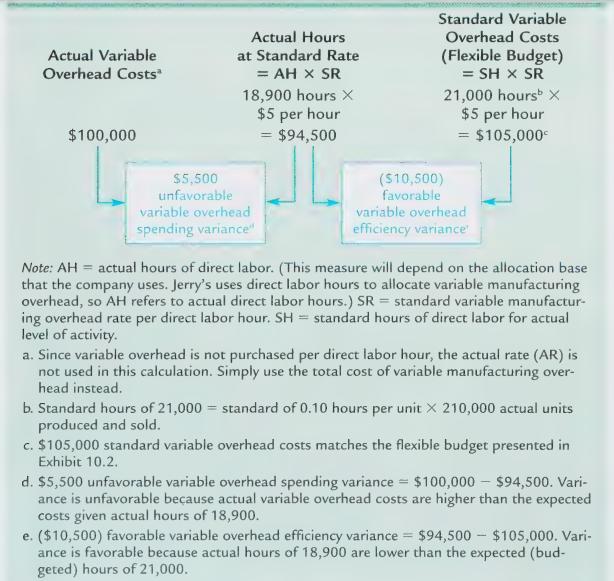

Exhibit 10.5

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Joseph Njoroge

I am a professional tutor with more than six years of experience. I have helped thousands of students to achieve their academic goals. My primary objectives as a tutor is to ensure that students do not have problems while tackling their academic problems.

10+ Reviews

27+ Question Solved

Related Book For

Question Posted: