Burdoy plc has a dedicated set of production facilities for component X. A just-in-time system is in

Question:

Burdoy plc has a dedicated set of production facilities for component X. A just-in-time system is in place such that no stock of materials; work-in-progress or finished goods are held.

At the beginning of period 1, the planned information relating to the production of component X through the dedicated facilities is as follows:

(i) Each unit of component X has input materials: 3 units of material A at £18 per unit and 2 units of material B at £9 per unit.

(ii) Variable cost per unit of component X (excluding materials) is £15 per unit worked on.

(iii) Fixed costs of the dedicated facilities for the period: £162 000.

(iv) It is anticipated that 10 per cent of the units of X worked on in the process will be defective and will be scrapped.

It is estimated that customers will require replacement (free of charge) of faulty units of component X at the rate of 2 per cent of the quantity invoiced to them in fulfilment of orders.

Burdoy plc is pursuing a total quality management philosophy.

Consequently all losses will be treated as abnormal in recognition of a zero-defect policy and will be valued at variable cost of production.

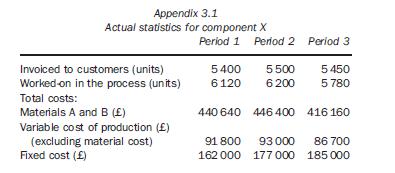

Actual statistics for each periods 1 to 3 for component X are shown in Appendix 3.1. No changes have occurred from the planned price levels for materials, variable overhead or fixed overhead costs.

Required:

(a) Prepare an analysis of the relevant figures provided in Appendix 3.1 to show that the period 1 actual results were achieved at the planned level in respect of (i) quantities and losses and (ii) unit cost levels for materials and variable costs.

(b) Use your analysis from (a) in order to calculate the value of the planned level of each of internal and external failure costs for period 1.

(c) Actual free replacements of component X to customers were 170 units and 40 units in periods 2 and 3 respectively.

Other data relating to periods 2 and 3 is shown in Appendix 3.1.

Burdoy plc authorized additional expenditure during periods 2 and 3 as follows:

Period 2: Equipment accuracy checks of £10 000 and staff training of £5000.

Period 3: Equipment accuracy checks of £10 000 plus £5000 of inspection costs; also staff training costs of £5000 plus £3000 on extra planned maintenance of equipment.

Required:

(i) Prepare an analysis for EACH of periods 2 and 3 which reconciles the number of components invoiced to customers with those worked-on in the production process.

The analysis should show the changes from the planned quantity of process losses and changes from the planned quantity of replacement of faulty components in customer hands; (All relevant working notes should be shown) (8 marks)

(ii) Prepare a cost analysis for EACH of periods 2 and 3 which shows actual internal failure costs, external failure costs, appraisal costs and prevention costs;

(iii) Prepare a report which explains the meaning and inter-relationship of the figures in Appendix 3.1 and in the analysis in (a), (b) and (c) (i)/(ii). The report should also give examples of each cost type and comment on their use in the monitoring and progressing of the TQM policy being pursued by Burdoy plc.

Step by Step Answer: