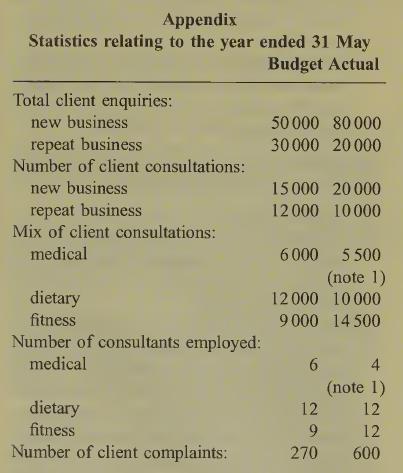

Advanced: Financial and non-financial performance measures Scotia Health Consultants Ltd provides advice to clients in medical, dietary

Question:

Advanced: Financial and non-financial performance measures Scotia Health Consultants Ltd provides advice to clients in medical, dietary and fitness matters by offering consultation with specialist staff.

The budget information for the year ended 31 May is as follows:

(i) Quantitative data as per Appendix.

(ii) Clients are charged a fee per consultation at the rate of: medical £75; dietary £50 and fitness £50.

(iii) Health foods are recommended and provided only to dietary clients at an average cost to the company of £10 per consultation. Clients are charged for such health foods at cost plus 100% mark-up.

(iv) Each customer enquiry incurs a variable cost of £3, whether or not it is converted into a consultation.

(v) Consultants are each paid a fixed annual salary as follows: medical £40000; dietary £28 000; fitness £25 000.

(vi) Sundry other fixed cost: £300000.

Actual results for the year to 31 May incorporate the following additional information:

(i) Quantitative data as per Appendix.

(ii) A reduction of 10% in health food costs to the company per consultation was achieved through a rationalisation of the range of foods made available.

(iii) Medical salary costs were altered through dispensing with the services of two full-time consultants and sub-contracting outside specialists as required. A total of 1900 consul¬ tations were sub-contracted to outside spe¬ cialists who were paid £50 per consultation.

(iv) Fitness costs were increased by £80000 through the hire of equipment to allow sophis¬ ticated cardio-vascular testing of clients.

(v) New computer software has been installed to provide detailed records and scheduling of all client enquiries and consultations. This soft¬ ware has an annual operating cost (including depreciation) of £50000.

Required:

(a) Prepare a statement showing the financial results for the year to 31 May in tabular format. This should show:

(i) the budget and actual gross margin for each type of consultation and for the company (ii) the actual net profit for the company (iii) the budget and actual margin (£) per consultation for each type of consulta¬ tion.

(Expenditure for each expense heading should be shown in (i) and (ii) as rel¬ evant.) (15 marks)

(b) Suggest ways in which each of the undemoted performance measures (1 to 5) could be used to supplement the financial results calculated in (a). You should include relevant quantita¬ tive analysis from the Appendix below for each performance measure:

1. Competitiveness; 2 Flexibility; 3. Resource utilisation; 4. Quality; 5. Innovation.

Step by Step Answer: