Intermediate: Calculation of fixed and variable overhead rates, normal activity level and under/over recovery of overheads (a)

Question:

Intermediate: Calculation of fixed and variable overhead rates, normal activity level and under/over recovery of overheads

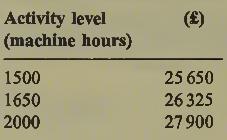

(a) C Ltd is a manufacturing company. In one of the production departments in its main factory a machine hour rate is used for absorbing production overhead. This is established as a predetermined rate, based on normal activity. The rate that will be used for the period which is just commencing is £15.00 per machine hour. Overhead expenditure anticipated, at a range of activity levels, is as follows:

Required:

Calculate:

(i) the variable overhead rate per machine hour;

(ii) the total budgeted fixed overhead;

(iii) the normal activity level of the depart¬ ment; and (iv) the extent of over/under absorption if actual machine hours are 1700 and expenditure is as budgeted.

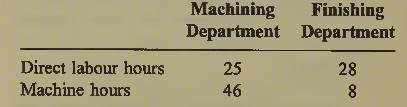

(b) In another of its factories, C Ltd carries out jobs to customers’ specifications. A particular job requires the following machine hours and direct labour hours in the two production departments:

Direct labour in both departments is paid at a basic rate of £4.00 per hour. 10% of the direct labour hours in the finishing department are overtime hours, paid at 125% of basic rate. Overtime premiums are charged to production overhead.

The job requires the manufacture of 189 com¬ ponents. Each component requires 1.1 kilos of prepared material. Loss on preparation is 10% of unprepared material, which costs £2.35 per kilo.

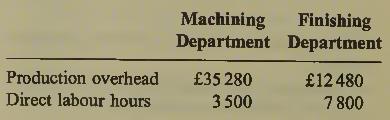

Overhead absorption' rates are to be established from the following data:

![]()

Required:

(i) Calculate the overhead absorption rate for each department and justify the absorption method used.

(ii) Calculate the cost of the job.

Step by Step Answer: