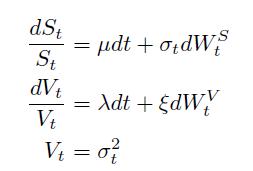

Consider the HullWhite volatility process: In the chapter, we worked under the simplifying assumption (as per Hull

Question:

Consider the Hull–White volatility process:

In the chapter, we worked under the simplifying assumption (as per Hull and White’s original paper), that the variance and stock processes were uncorrelated. Now consider the more general case

![]()

Derive an integral expression for the undiscounted price of a call by considering the distribution of the stock conditional on realised variance.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Antony Sang

I am a research and academic writer whose work is outstanding. I always have my customer's interests at heart. Time is an important factor in our day to day life so I am always time conscious. Plagiarism has never been my thing whatsoever. I give best Research Papers, Computer science and IT papers, Lab reports, Law, programming, Term papers, English and literature, History, Math, Accounting, Business Studies, Finance, Economics, Business Management, Chemistry, Biology, Physics, Anthropology, Sociology, Psychology, Nutrition, Creative Writing, Health Care, Nursing, and Articles.

2+ Reviews

10+ Question Solved

Related Book For

The Value Of Uncertainty Dealing With Risk In The Equity Derivatives Market

ISBN: 9781848167728,9781908979582

1st Edition

Authors: George Kaye

Question Posted: